The AI trade became overcrowded, and many are now panicking about the prospects of stocks that had run too high and are now facing uncertainty in a rapidly changing environment. This was confirmed by Charles Schwab Corporation last week when it published its Q1 2026 Trader Sentiment Survey. According to the survey results, only 52% of the traders were bullish on AI stocks compared to 64% in the previous quarter.

This shift in retail sentiment is generating a debate around whether AI stocks are risky right now. Contrarian investors believe the dip provides an opportunity, and they’ve been given a pat on the back by none other than Morgan Stanley. Analysts at the financial services firm believe high-quality companies that are growing strongly are worth buying at an attractive valuation. The tailwind of AI adoption is currently dominating the disruption fears as far as business performance is concerned. Morgan Stanley analysts believe investors should utilize the sell-off to take positions in software stocks that will find a way to deal with the potential disruption that newer AI models have caused.

Software Stock #1: Microsoft (MSFT)

Microsoft (MSFT) is a software company known mainly for its Windows operating system and enterprise software. The company also offers laptops and cloud services, among other things. It is led by Satya Nadella and is headquartered in Washington State.

MSFT stock has given back all its gains from the last 12 months since the launch of competitor Anthropic's Claude Opus 4.6 AI model. This is still a better performance than the iShares Expanded Tech-Software Sector ETF (IGV), which not only gave back all its gains but is now down nearly 12% in the same period.

As a result of the selloff in software stocks, Microsoft is now trading at a forward P/E of 23.49x. This is 25% below the stock’s five-year average P/E multiple and just above the S&P 500’s ($SPX) forward P/E multiple of 21.92x. A similar picture is depicted across most of the valuation multiples. What’s more, even the dividend yield of 0.86% is now above the five-year average, which is attractive considering the stock is up 75% in the last five years.

Before the selloff started in early February, Microsoft had already announced a stellar earnings report, registering 17% year-over-year (YoY) growth in revenue. Revenue from Microsoft Cloud touched $50 billion for the first time, rising 26% YoY. This segment is likely to stay strong even if the software industry is severely disrupted. AI doing the software tasks will still require computational power and cloud access, which Microsoft provides. It is therefore a stock worth buying on the dip.

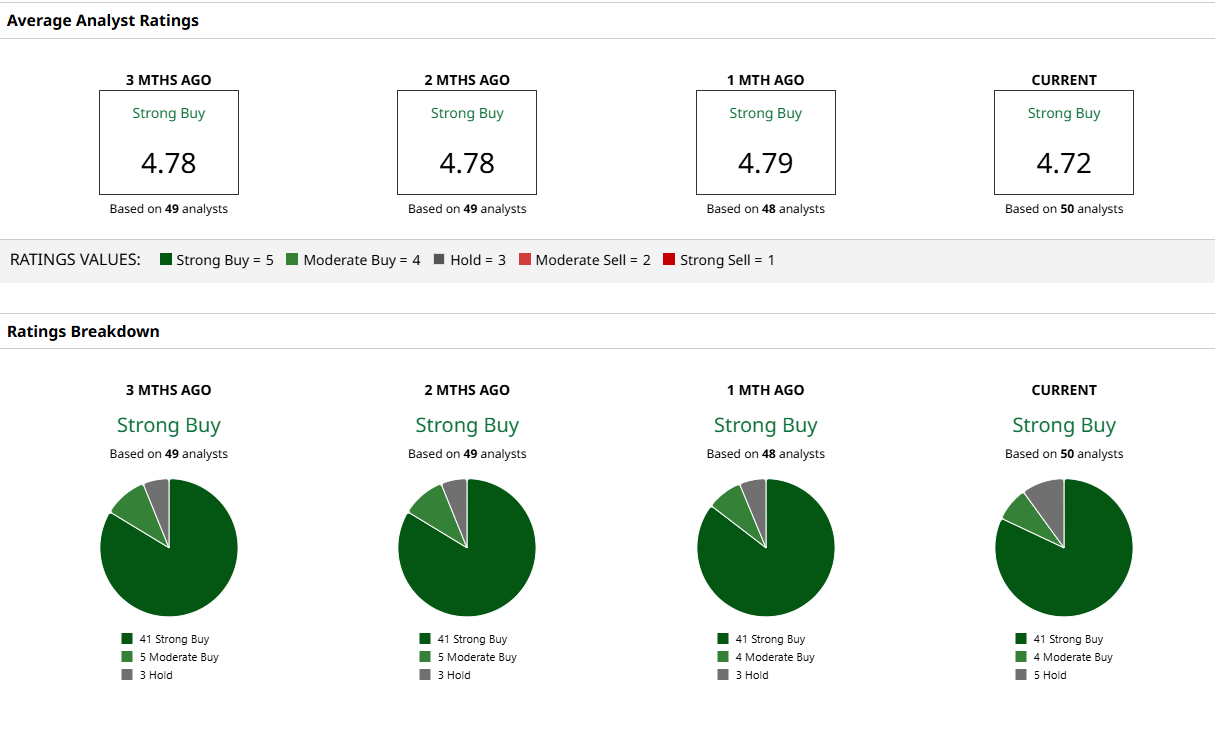

Analysts are still bullish on the stock despite disruption fears, with 41 out of 50 Wall Street analysts rating it a “Strong Buy.” The mean target price of $595.6 offers 45% upside from here on, while the most bullish analyst price target of $678 offers more than 65% upside.

Software Stock #2: Atlassian (TEAM)

Atlassian (TEAM) provides productivity and collaboration tools, including Jira, Jira Service Management, Confluence, and Loom. The company is headquartered in San Francisco, California, and has been operating since 2002.

TEAM stock is down a staggering 71% in the last 12 months. It has lost a quarter of its value in the last one month, despite the iShares Expanded Tech-Software Sector ETF trading positive during the same period. This reflects how bad the sentiment is around collaboration tools, but that is undoubtedly what makes it an exciting opportunity.

TEAM is currently as cheap as a stock can get. It is trading at a staggering 82% discount to its five-year forward price-to-cash flow average. A similar discount is on offer on the forward price-to-book and price-to-sales ratio as well. As far as multiples are concerned, the stock is cheap.

The question for investors is whether the future holds more promise than what the market is expecting. The company is expected to grow its earnings by 15.74% in 2027, 18.55% in 2028, and 15% by 2029. These would be great numbers if the growth were guaranteed. However, amid disruption fears, one needs to look closely at how the management is approaching this.

On the earnings call on Feb. 5, management reiterated that there was no change in the revenue growth outlook for FY 2027. The FY 2026 guidance was not extraordinary, but management’s cautious approach was expected with what’s happening in the industry. In short, there weren't any red flags in the earnings call, and buying the stock now while keeping an eye on the next earnings report might be the right way to go ahead with this stock.

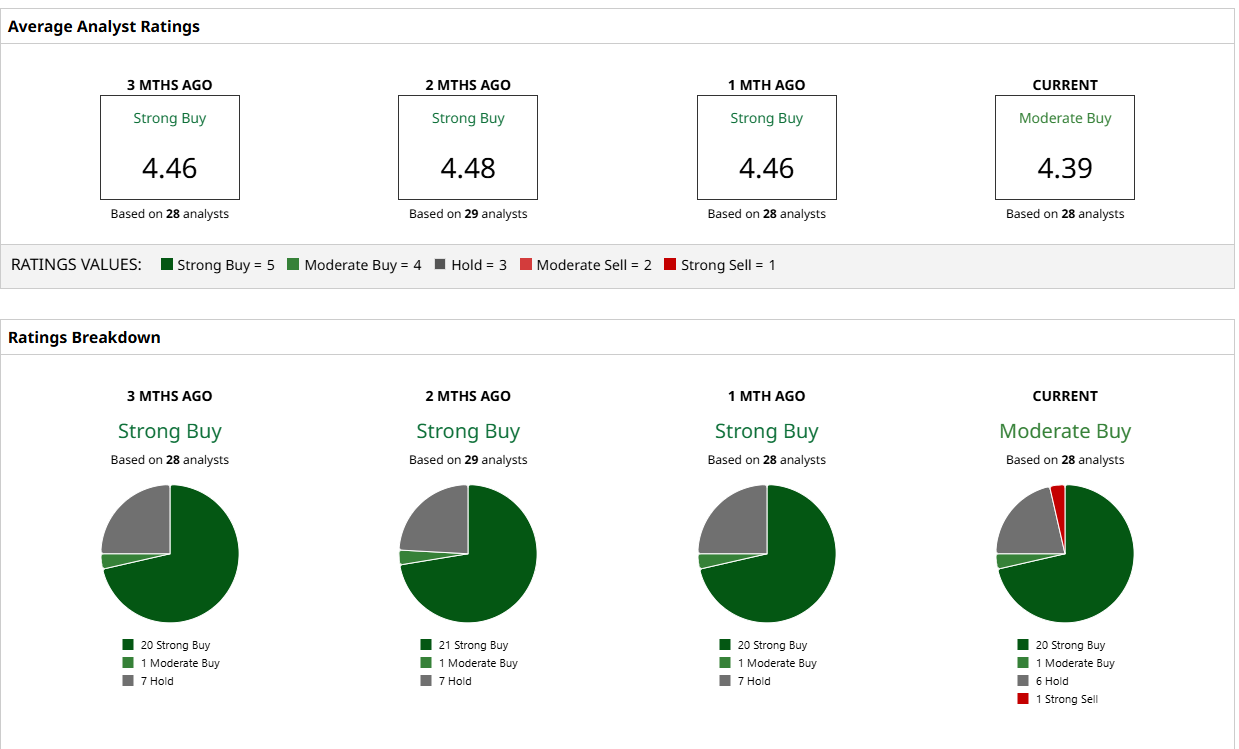

Analysts have a consensus “Moderate Buy” stance on the TEAM stock. After the Q2 2026 earnings report, Citi lowered its price target to $160 from the previous $210. This is quite close to the mean price target of $163.32, according to 28 different analysts’ ratings. Despite the downgrade, Citi’s price target still sees the stock more than doubling from here on.

Software Stock #3: Intuit (INTU)

Intuit (INTU) is a software company that specializes in servicing the financial industry through its cloud-based platform. The firm offers tax preparation and filing, enterprise solutions, accounting tools, invoicing, and payments, among other things. It is headquartered in Mountain View, California.

INTU stock has fared slightly better than the other two software stocks, down only 29% in the last 12 months. It has also recovered all the losses post-Claude Opus 4.6 launch. However, it must be added that most of that recovery has come on the back of an impressive Q2 earnings report on Feb. 26.

The earnings report that propelled the stock higher indicates the company has done a good job satisfying investors that it won’t be so easily disrupted. It has also meant that previous discounts on valuation are not available anymore, though the stock is still trading 50% below its five-year average on various metrics like forward P/E and forward price-to-cash-flow ratio.

The company reaffirmed guidance on the earnings call, expecting total revenue in the range of $20.997 billion and $21.186 billion for fiscal 2026. This translates to a growth rate of 12% to 13%. This may not be that impressive, but what stood out on the call was CEO Goodarzi’s mention of a multiyear deal with Anthropic to leverage the company’s proprietary data. The CEO called it a game-changer, and it would certainly be one if the company were able to pull it off. This suggests that if the disruption happens, Intuit might be able to benefit from the resulting changing dynamics.

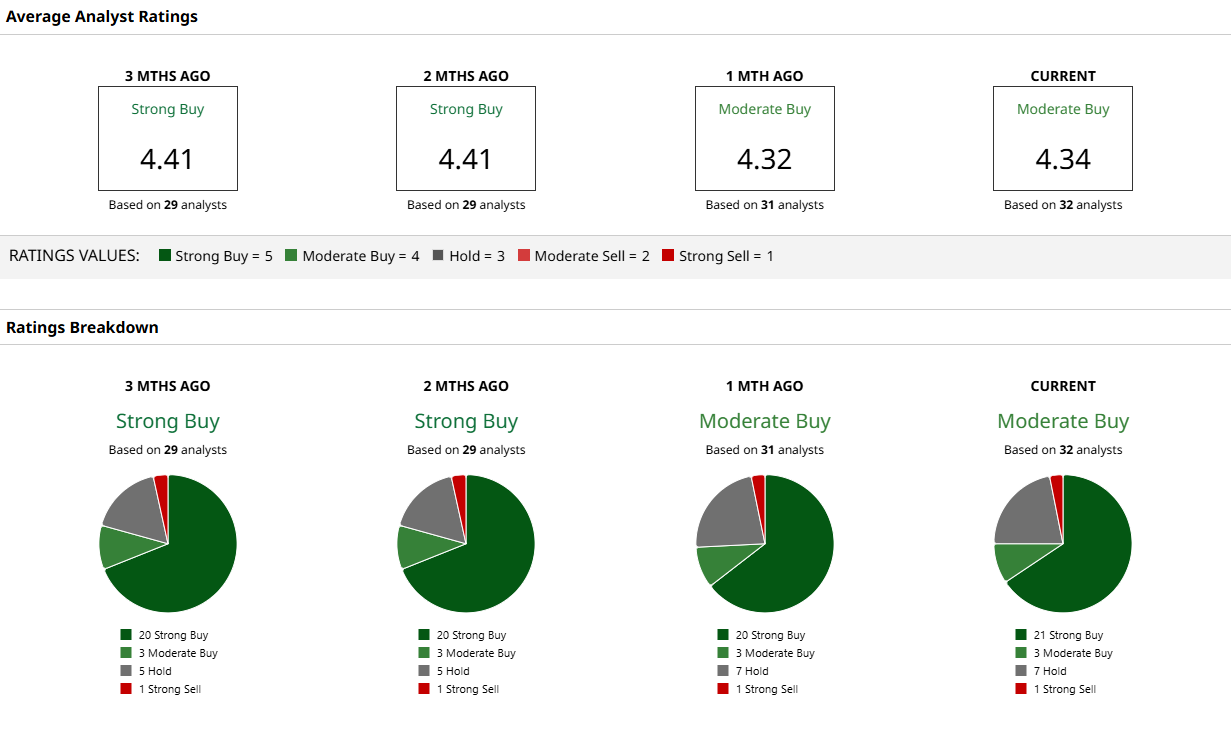

Analysts have shown caution in the last few days, lowering their price targets on the stock. So far this week, Mizuho lowered its price target from $675 to $600, Goldman Sachs from $720 to $519, and Citi from $803 to $649. Only time will tell if analysts were right, but even if they are, the mean target price of $629.48, as per 32 analysts covering INTU stock, still offers 43% upside from here on.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- South Korea’s Stock Market Just Fell 12% in 1 Day. Here's What It Means for Investors.

- As CoreWeave Signs a Deal with Perplexity, Should You Buy, Sell, or Hold CRWV Stock?

- What Does the Middle East Conflict Mean for Valero Energy Stock?

- This Chart Indicator Clears the Noise to Show a Stock’s Real Trend