In today’s digital world, cybersecurity has become one of the most critical pillars of modern business. In that space, CrowdStrike Holdings (CRWD) has steadily risen to prominence with its artificial intelligence (AI)-powered Falcon platform, offering broad protection across endpoints, cloud, and identity. Lately, CRWD stock has been flashing green even as parts of the broader tech sector wrestle.

Part of that renewed confidence stems from the company’s latest quarterly results, which reassured investors about its growth trajectory. Meanwhile, analysts have begun pushing back against the wave of skepticism that surrounded the stock last month.

Morgan Stanley recently upgraded CRWD to “Overweight” and named it a “Top Pick.” Led by analyst Meta Marshall, it believes the company is a durable platform winner thanks to its strong AI positioning, rising adoption of new modules, improving endpoint trends, and potential for double-digit revenue growth with expanding margins and cash flow.

About CrowdStrike Stock

Based in Austin, Texas, CrowdStrike Holdings is a leading global cybersecurity firm armed with its cutting-edge Falcon platform. Merging AI with the CrowdStrike Security Cloud, it excels in real-time attack detection and automated protection, delivering seamless solutions.

As data breaches rise, the demand for robust cybersecurity is surging, and CrowdStrike is right in the mix, innovating with new products and strategic partnerships. With profitable quarters and boasting a market cap of $111 billion, this cybersecurity trailblazer is redefining standards and protecting organizations against ever-evolving cyber threats.

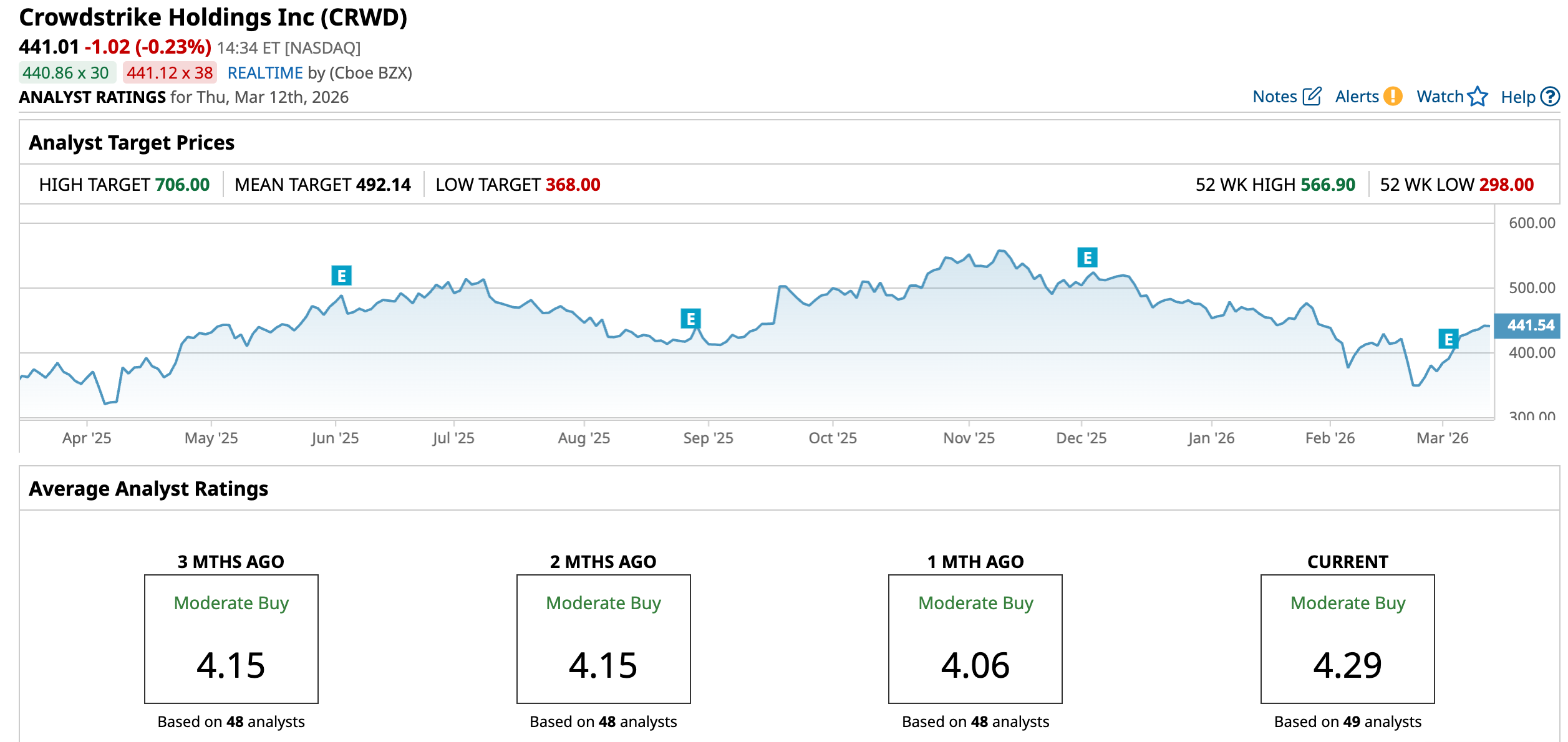

CrowdStrike has been on quite a run over the past few years, rewarding investors with 127% gains over five years and an even sharper 232% jump in the past three years. Even after pulling back about 22% from its November high of $566.90, the stock is still up 27% over the past 52 weeks, showing the strength of the broader trend.

Some investors began worrying about valuation, a common concern for high-growth tech names. More recently, another debate has emerged as agentic AI evolves. Some analysts wonder whether AI automation could eventually pressure pricing for software platforms that rely upon layered subscriptions, a model central to CrowdStrike’s expanding Falcon ecosystem.

Still, sentiment has recently turned positive again. Since early March, the stock has pushed higher, helped by its solid Q4 earnings report and a broader rally in cybersecurity stocks. Rising geopolitical tensions have also put cyber defense back in focus, reminding investors that as digital threats grow, companies like CrowdStrike remain central to protecting modern infrastructure.

Technically, momentum is quietly turning positive for CRWD stock. The 14-day RSI has climbed to 59, recovering sharply from the oversold levels seen in February. At the same time, the MACD oscillator is flashing early bullish signals. While still in negative territory, the MACD line has crossed above the signal line and the histogram has flipped positive, often a sign that buying pressure is starting to build again.

Valuation-wise, CrowdStrike commands a premium. The stock trades around 22.6 times forward adjusted earnings and roughly 12.3 times sales, noticeably higher than many of its cybersecurity peers. Yet there’s an interesting twist.

Even after more than doubling over the past five years, CRWD is currently valued below its own five-year average multiples. That suggests the premium may not be as stretched as it looks at first glance. With analysts expecting continued growth in top and bottom lines, those lofty multiples could gradually ease over time, making today’s valuation appear more reasonable for long-term investors.

CrowdStrike Beats Q4 Numbers

CrowdStrike delivered a solid Q4 earnings report for fiscal 2026 after the market closed on March 3. While the results were not too impressive, the company still managed to edge past Wall Street’s expectations on both revenue and profit. CrowdStrike reported $1.31 billion in revenue, marking a 23% increase year-over-year (YOY), while adjusted EPS climbed 38.3% annually to $1.12.

A large portion of that growth came from the company’s core subscription business. Subscription revenue rose 23.2% annually to $1.24 billion, making up about 95.2% of total revenue. The rise was partly fueled by the growing adoption of Falcon Flex, a subscription model that allows customers to commit to spending upfront and then choose different security modules later, making the purchasing process simpler. Meanwhile, professional services revenue, which represents the remaining 4.8% of sales, increased 25.7% YOY to $63.1 million.

Customer adoption of CrowdStrike’s platform also continues to deepen. As of Jan. 31, 2026, about 50% of subscription customers were using six or more cloud modules, while 34% had adopted seven or more, and 24% were running eight or more modules. This indicates a sign that clients are increasingly consolidating security tools on the Falcon platform.

Also, the quarter brought record levels of net new annual recurring revenue (ARR), operating income, and free cash flow, key metrics for a subscription-driven business. Ending ARR reached $5.25 billion, up 24% YOY, while net new ARR surged 47% to $330.7 million.

Non-GAAP operating income rose 44.9% YOY to $325.8 million in Q4, and the company ended the fiscal year with $5.23 billion in cash and cash equivalents as of Jan. 31, against $745.5 million in long-term debt. CrowdStrike also generated $497.9 million in operating cash flow and $376.4 million in FCF during the quarter.

Much of the company’s momentum is tied to the growing demand for AI-powered cybersecurity. As businesses increasingly adopt AI, CrowdStrike’s platform is positioning itself as critical infrastructure to help secure AI systems across everything from GPUs and cloud environments to user interactions and prompts.

Looking ahead, CrowdStrike expects a steady start to fiscal 2027. For Q1, management forecasts revenue between $1.36 billion and $1.364 billion, with adjusted EPS between $1.06 and $1.07. ARR is projected to land between $5.502 billion and $5.504 billion.

For the full fiscal year 2027, management expects CrowdStrike to generate revenue between $5.87 billion and $5.93 billion, alongside adjusted EPS of $4.78 to $4.90. ARR for the year is anticipated to climb further, landing between $6.47 billion and $6.52 billion.

Overall, the outlook largely matched analysts’ expectations. While the guidance reassured investors about continued growth, it was not bold enough to fully quiet some lingering questions on Wall Street around long-term AI competition and pricing dynamics.

Analysts tracking CrowdStrike expect revenue for the first quarter of fiscal 2027 to be around $1.36 billion, with EPS estimated to rise by 147.8% YOY to $0.11. Looking ahead to fiscal 2027, EPS is projected to grow impressively to $0.88, before rising by another 96.6% annually to $1.73 in fiscal 2028.

What Do Analysts Expect for CrowdStrike Stock?

Optimism around CrowdStrike is picking up on Wall Street. Analysts at Morgan Stanley upgraded the cybersecurity firm to “Overweight” from “Equal-weight,” adding it to its Top Pick. The bank also lifted its price target to $510 from $487, signaling growing confidence in the company’s long-term growth story.

Analysts led by Meta Marshall believe CrowdStrike is emerging as a durable platform winner, thanks largely to its strong positioning in AI and expanding adoption of its newer security modules. While they acknowledge the stock’s expensive valuation, they argue the fundamentals justify it and point to potential revenue growth, improving margins, and stronger FCF in the years ahead.

Another key reason for the bullish call is CrowdStrike’s growing strength across multiple security categories. Its leadership in Endpoint Detection and Response (EDR), along with its expanding platform across cloud, identity, AI, and next-generation SIEM, is helping the company steadily gain market share.

Marshall’s team also noted improving win rates in core endpoint security and stronger adoption of the broader Falcon platform. A newer offering, Falcon Flex, is quickly becoming a catalyst, helping CrowdStrike land larger, longer-term deals and consolidate multiple security tools into one platform.

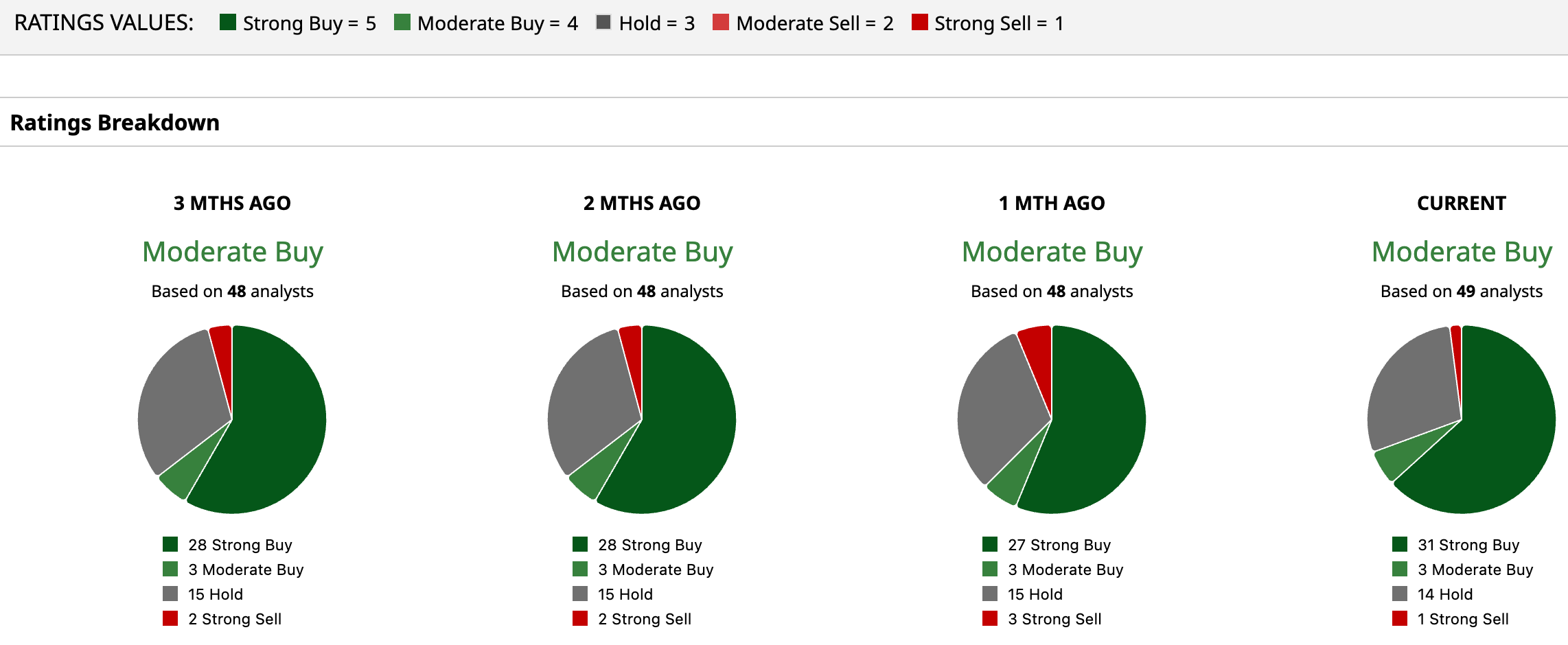

Overall, analysts are confident in CRWD stock but with a dash of caution. The stock has a consensus “Moderate Buy” rating. Of the 49 analysts covering it, 31 recommend a “Strong Buy,” three suggest a “Moderate Buy,” 14 play it safe with a “Hold” rating, and the remaining analyst is outright skeptical, giving a “Strong Sell” rating.

The average analyst price target of $492.14 indicates potential upside of 11.6%. The Street-high price target of $706 suggests that CRWD stock could rally as much as 60% from here.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Why Wedbush Analysts Love AppLovin Stock Right Now

- Bumble Just Shot Above Its Key Moving Averages. Is There More Room for BMBL Stock to Run?

- Why This Analyst Is Betting That MicroStrategy Stock Can Gain 25% from Here

- As Analysts Praise the New MacBook Neo as a Game-Changer, Should You Buy Apple Stock?