Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Parker-Hannifin (NYSE: PH) and the best and worst performers in the gas and liquid handling industry.

Gas and liquid handling companies possess the technical know-how and specialized equipment to handle valuable (and sometimes dangerous) substances. Lately, water conservation and carbon capture–which requires hydrogen and other gasses as well as specialized infrastructure–have been trending up, creating new demand for products such as filters, pumps, and valves. On the other hand, gas and liquid handling companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 13 gas and liquid handling stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 1.6% on average since the latest earnings results.

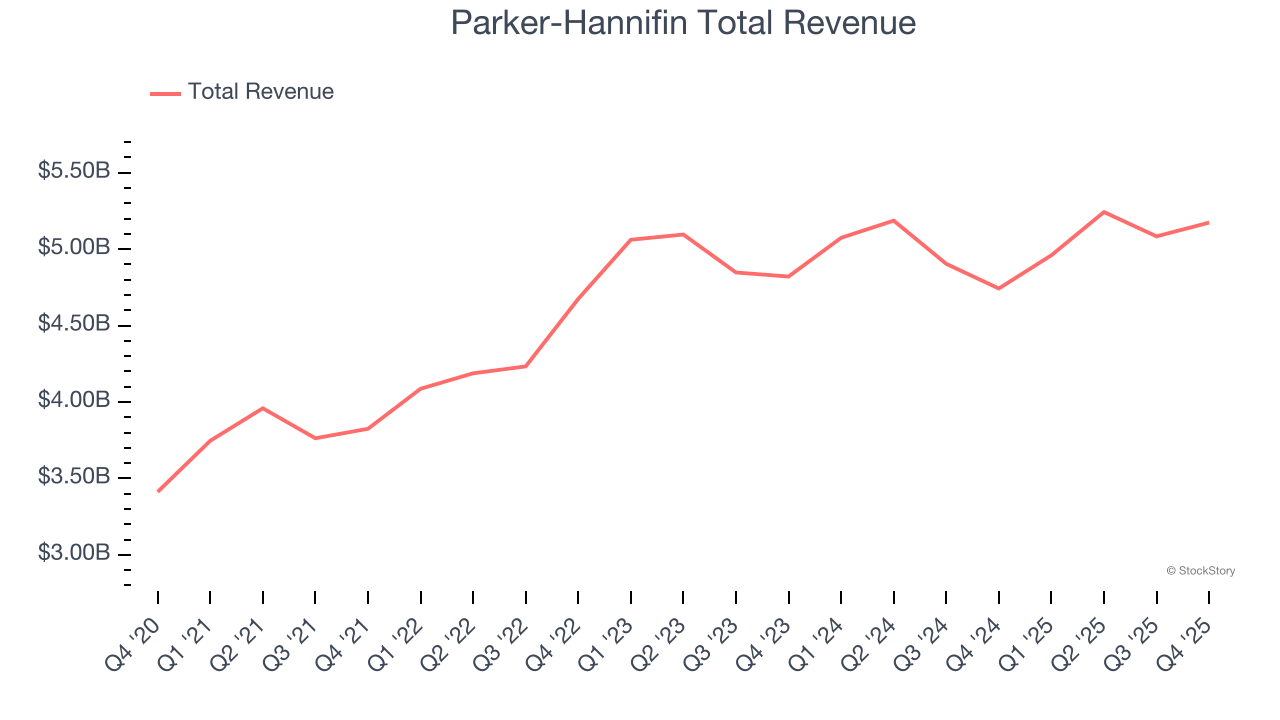

Parker-Hannifin (NYSE: PH)

Founded in 1917, Parker Hannifin (NYSE: PH) is a manufacturer of motion and control systems for a wide variety of mobile, industrial and aerospace markets.

Parker-Hannifin reported revenues of $5.17 billion, up 9.1% year on year. This print exceeded analysts’ expectations by 2.1%. Overall, it was a strong quarter for the company with a solid beat of analysts’ organic revenue estimates and an impressive beat of analysts’ revenue estimates.

“This was another outstanding quarter that reflected the performance of our global team, the power of our business system The Win Strategy™, and the strength of our transformed portfolio,” said Jenny Parmentier, Chairman and Chief Executive Officer.

Interestingly, the stock is up 7.7% since reporting and currently trades at $987.

Is now the time to buy Parker-Hannifin? Access our full analysis of the earnings results here, it’s free.

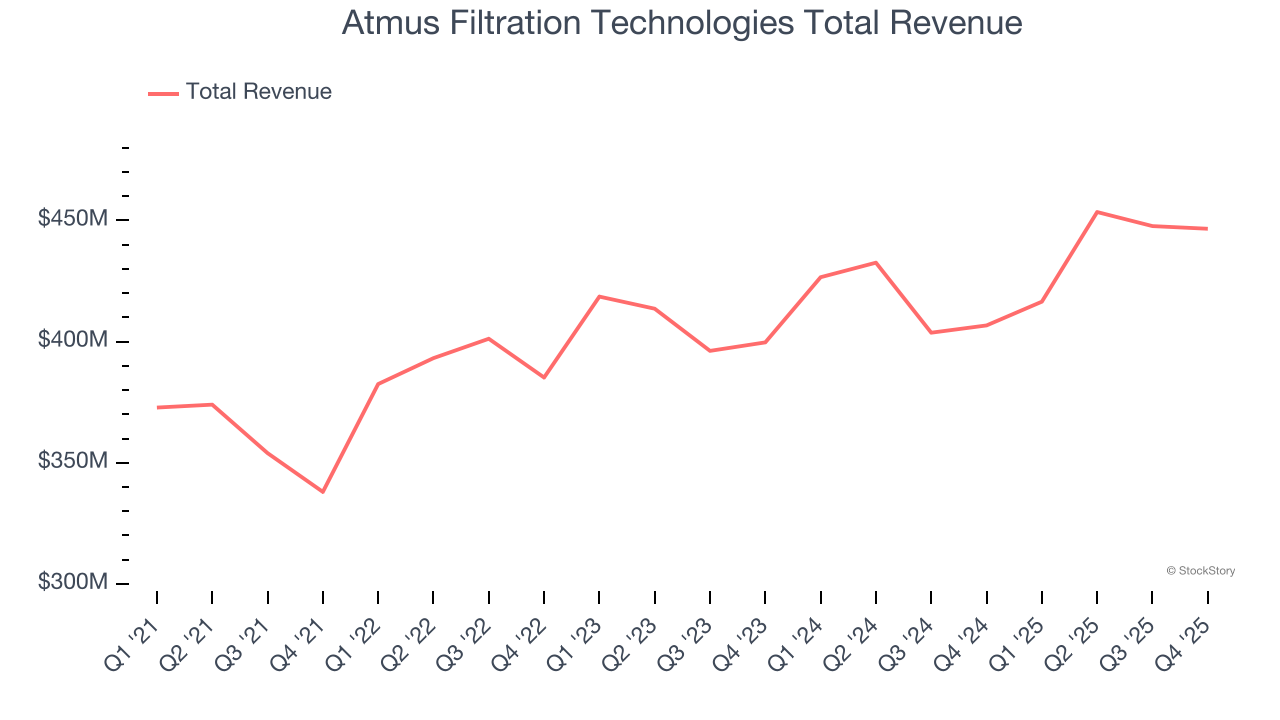

Best Q4: Atmus Filtration Technologies (NYSE: ATMU)

Spun out of Cummins in 2023 after 65 years as part of the engine maker, Atmus Filtration Technologies (NYSE: ATMU) manufactures filters for trucks, construction equipment, and agriculture machinery to reduce emissions and protect engines.

Atmus Filtration Technologies reported revenues of $446.6 million, up 9.8% year on year, outperforming analysts’ expectations by 5.5%. The business had a stunning quarter with a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ adjusted operating income estimates.

The market seems content with the results as the stock is up 2.6% since reporting. It currently trades at $63.74.

Is now the time to buy Atmus Filtration Technologies? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Chart (NYSE: GTLS)

Installing the first bulk Co2 tank for McDonalds’s sodas, Chart (NYSE: GTLS) provides equipment to store and transport gasses.

Chart reported revenues of $1.08 billion, down 2.5% year on year, falling short of analysts’ expectations by 8.4%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue estimates and a significant miss of analysts’ adjusted operating income estimates.

Chart delivered the weakest performance against analyst estimates and slowest revenue growth in the group. The stock is flat since the results and currently trades at $207.31.

Read our full analysis of Chart’s results here.

Ingersoll Rand (NYSE: IR)

Started with the invention of the steam drill, Ingersoll Rand (NYSE: IR) provides mission-critical air, gas, liquid, and solid flow creation solutions.

Ingersoll Rand reported revenues of $2.09 billion, up 10.1% year on year. This result beat analysts’ expectations by 2.6%. It was a very strong quarter as it also recorded a solid beat of analysts’ adjusted operating income estimates and an impressive beat of analysts’ revenue estimates.

The stock is down 2.8% since reporting and currently trades at $91.58.

Read our full, actionable report on Ingersoll Rand here, it’s free.

Helios (NYSE: HLIO)

Founded on the principle of treating others as one wants to be treated, Helios (NYSE: HLIO) designs, manufactures, and sells motion and electronic control components for various sectors.

Helios reported revenues of $210.7 million, up 17.4% year on year. This print topped analysts’ expectations by 6.4%. Overall, it was a very strong quarter as it also put up EPS guidance for next quarter exceeding analysts’ expectations and an impressive beat of analysts’ adjusted operating income estimates.

Helios delivered the biggest analyst estimates beat but had the weakest full-year guidance update among its peers. The stock is down 6.2% since reporting and currently trades at $69.78.

Read our full, actionable report on Helios here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.