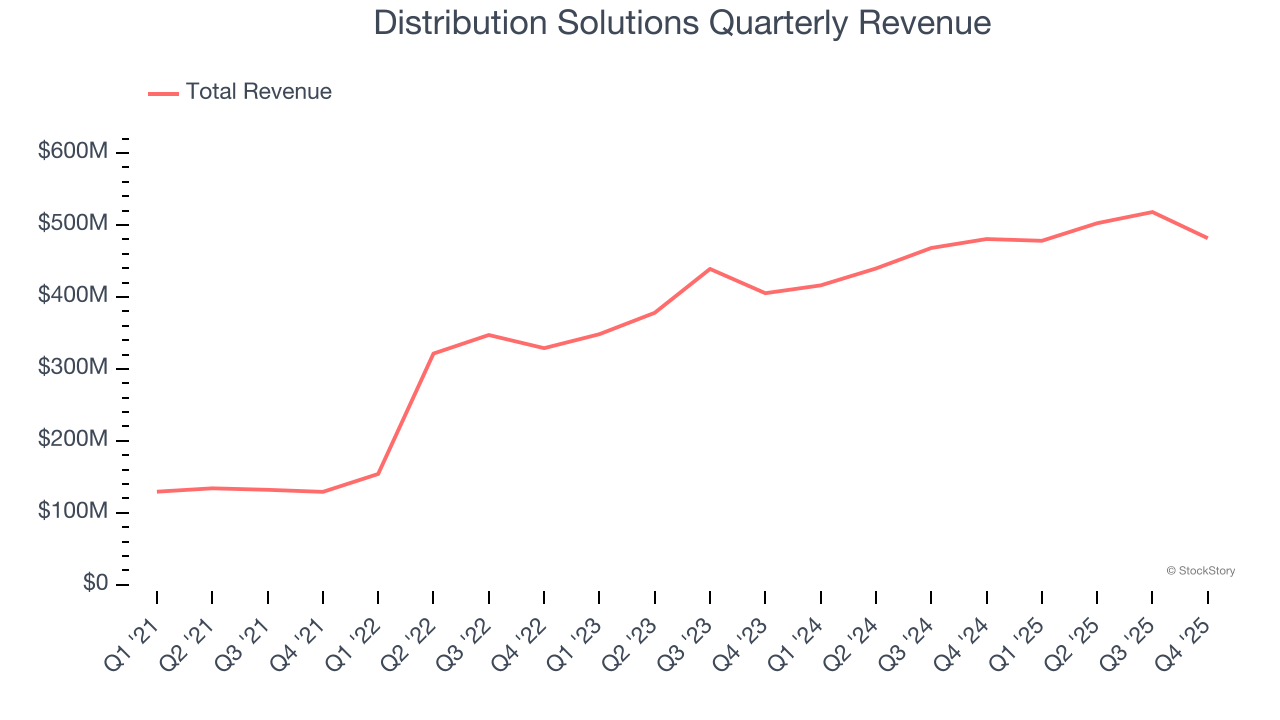

Industrial and safety product distributor Distribution Solutions (NASDAQ: DSGR) missed Wall Street’s revenue expectations in Q4 CY2025, with sales flat year on year at $481.6 million. Its non-GAAP profit of $0.18 per share was 43.2% below analysts’ consensus estimates.

Is now the time to buy Distribution Solutions? Find out by accessing our full research report, it’s free.

Distribution Solutions (DSGR) Q4 CY2025 Highlights:

- Revenue: $481.6 million vs analyst estimates of $496.3 million (flat year on year, 3% miss)

- Adjusted EPS: $0.18 vs analyst expectations of $0.32 (43.2% miss)

- Adjusted EBITDA: $35.44 million vs analyst estimates of $43.9 million (7.4% margin, 19.3% miss)

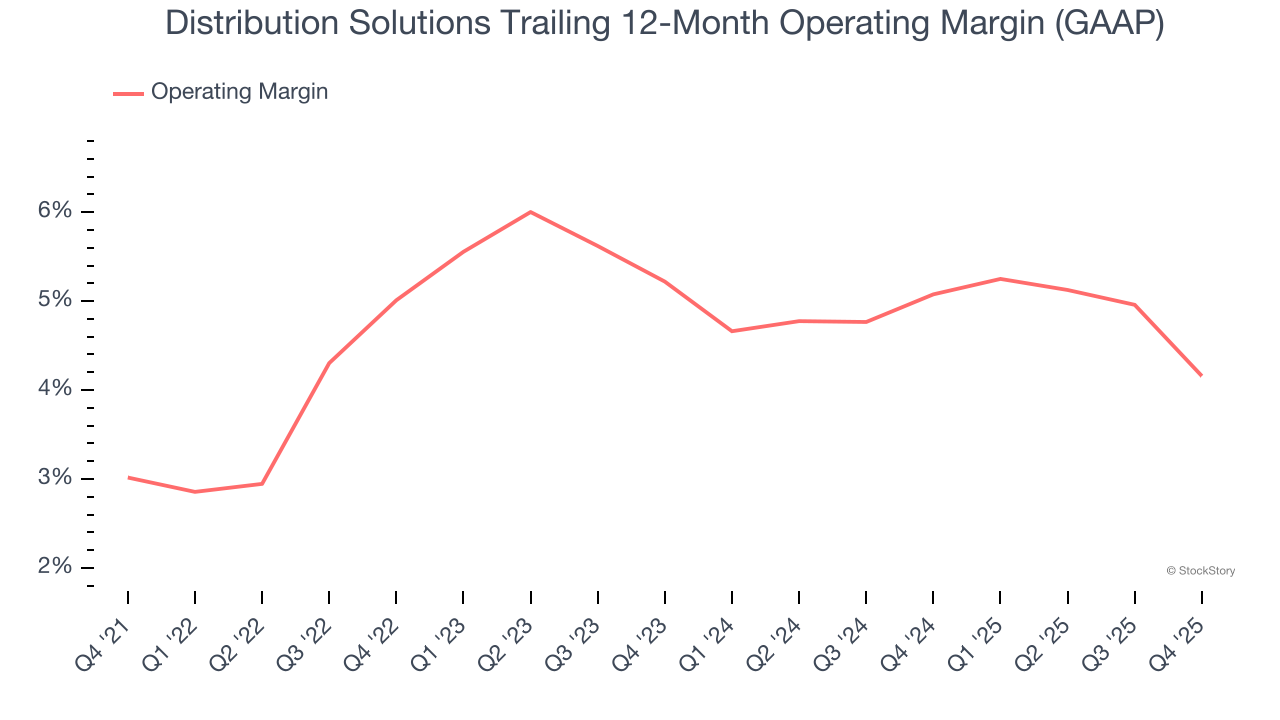

- Operating Margin: 1.6%, down from 4.9% in the same quarter last year

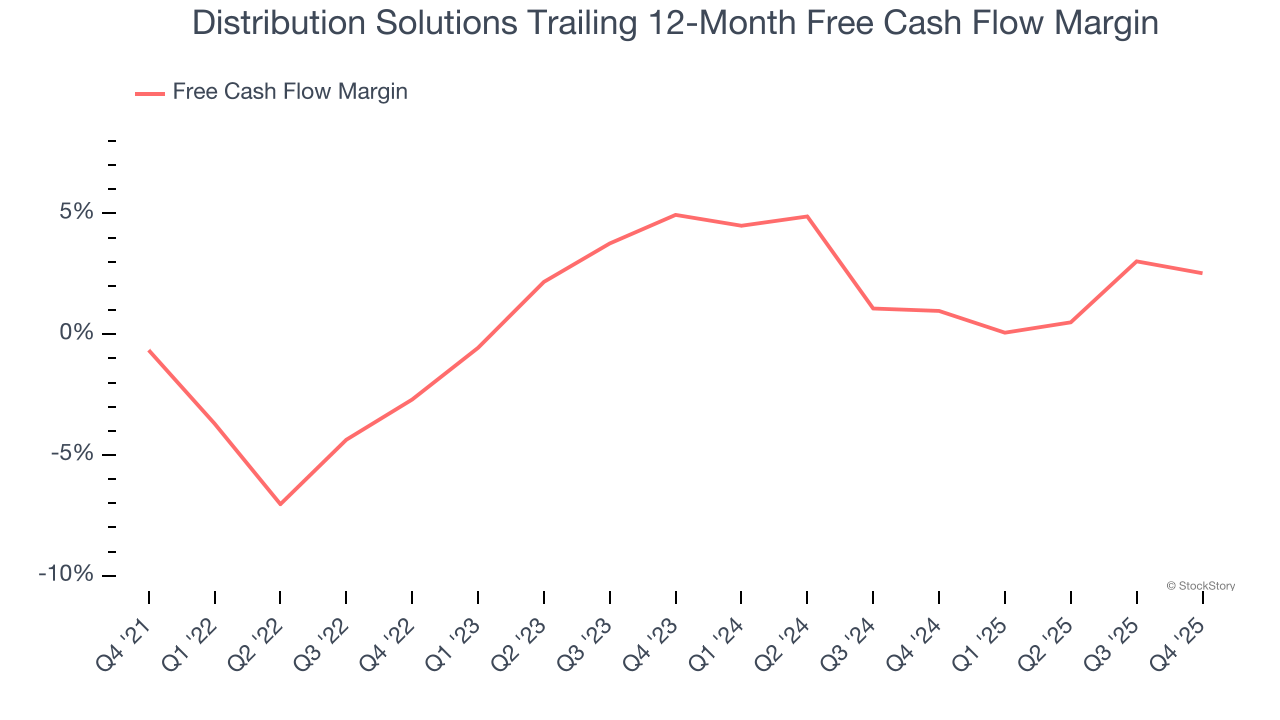

- Free Cash Flow Margin: 2.4%, down from 4.5% in the same quarter last year

- Market Capitalization: $1.37 billion

Bryan King, CEO and Chairman, said, "For the full year, we delivered sales growth of 9.8% despite one less selling day, supported by organic average daily sales growth of 3.6%. This performance reflects the strength of our operating model and execution amidst a challenging macroeconomic environment affecting most U.S. companies in 2025. We generated improved GAAP net income and strong operating cash flow for the year, demonstrating the resilience of our business while continuing to invest in growth initiatives. While margins were pressured by end-market softness, sales mix, timing of certain expenses and continued investments, we believe actions being taken within our verticals are positioning us better for long-term profitable growth.

Company Overview

Founded in 1952, Distribution Solutions (NASDAQ: DSGR) provides supply chain solutions and distributes industrial, safety, and maintenance products to various industries.

Revenue Growth

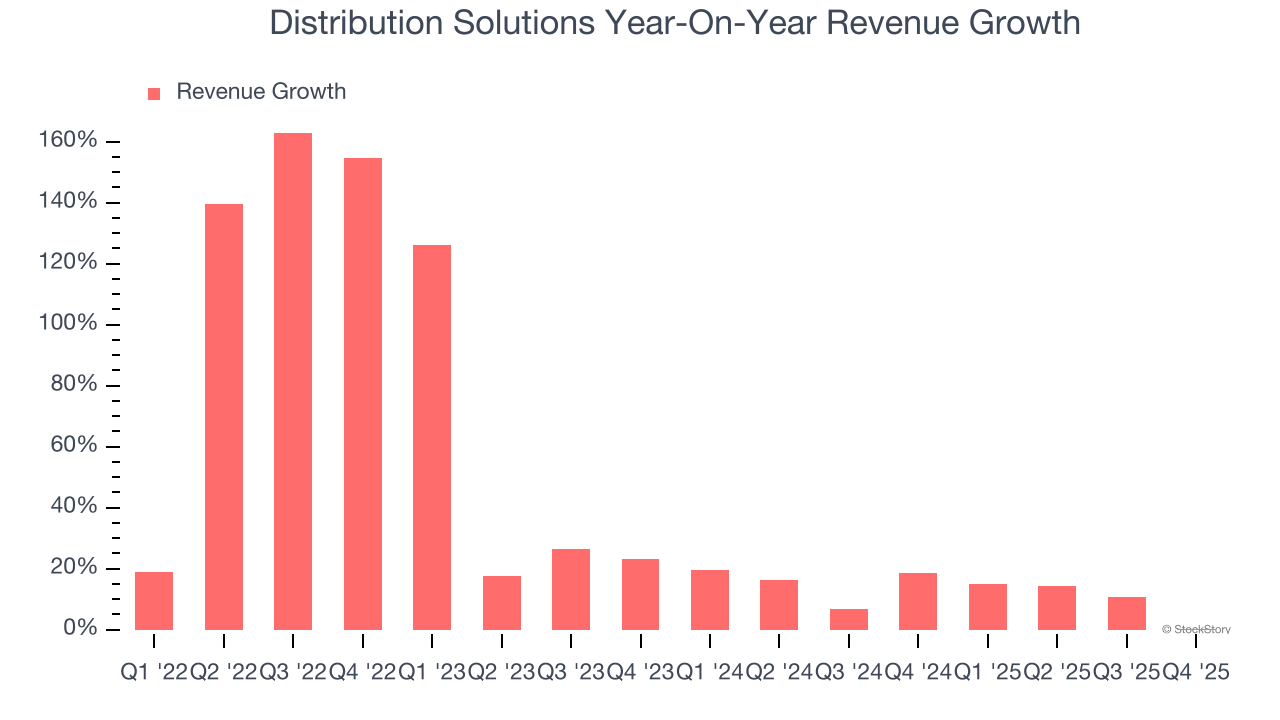

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Distribution Solutions’s sales grew at an incredible 39.4% compounded annual growth rate over the last four years. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Distribution Solutions’s annualized revenue growth of 12.3% over the last two years is below its four-year trend, but we still think the results suggest healthy demand.

This quarter, Distribution Solutions’s $481.6 million of revenue was flat year on year, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 5% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Distribution Solutions was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.7% was weak for an industrials business. This result is surprising given its high gross margin as a starting point.

On the plus side, Distribution Solutions’s operating margin rose by 1.1 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q4, Distribution Solutions generated an operating margin profit margin of 1.6%, down 3.3 percentage points year on year. Since Distribution Solutions’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Distribution Solutions has shown poor cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.6%, below what we’d expect for an industrials business.

Taking a step back, an encouraging sign is that Distribution Solutions’s margin expanded by 3.2 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Distribution Solutions’s free cash flow clocked in at $11.72 million in Q4, equivalent to a 2.4% margin. The company’s cash profitability regressed as it was 2 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

Key Takeaways from Distribution Solutions’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 8.3% to $27.25 immediately following the results.

Distribution Solutions underperformed this quarter, but does that create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).