SoundHound AI has gotten torched over the last six months - since September 2025, its stock price has dropped 42% to $8.27 per share. This might have investors contemplating their next move.

Is now the time to buy SoundHound AI, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is SoundHound AI Not Exciting?

Despite the more favorable entry price, we don't have much confidence in SoundHound AI. Here are three reasons we avoid SOUN and a stock we'd rather own.

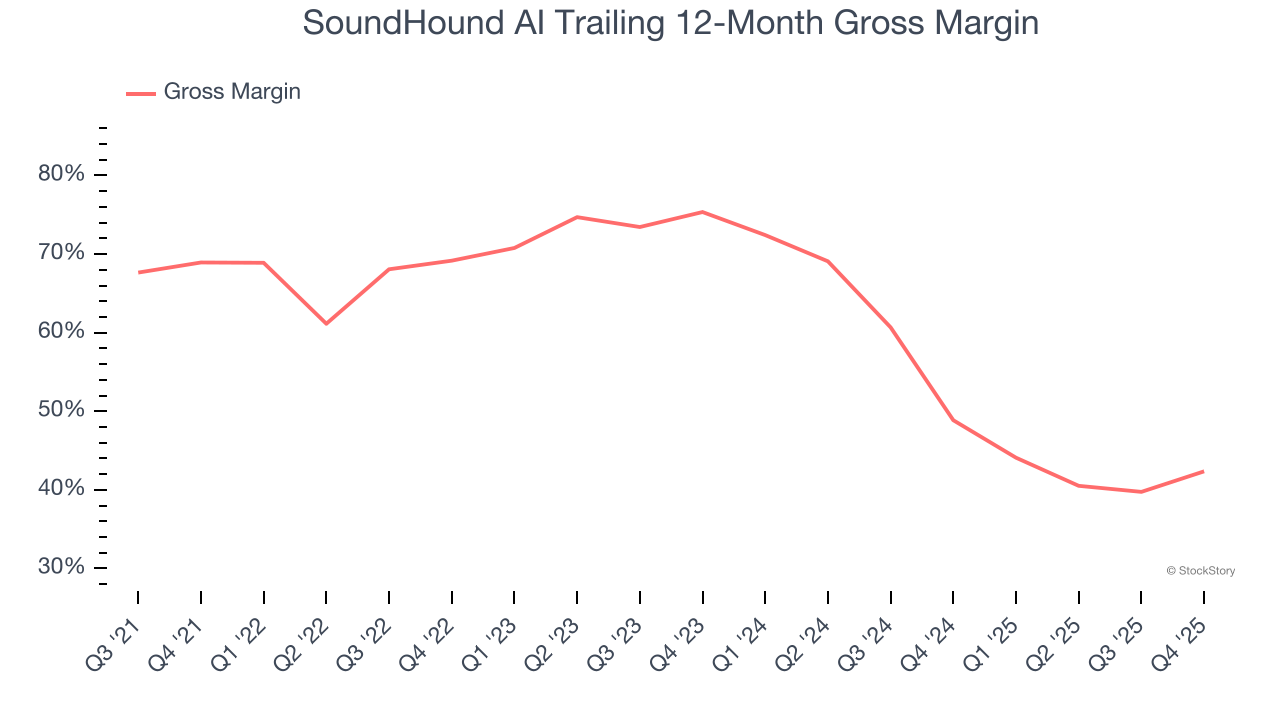

1. Low Gross Margin Reveals Weak Structural Profitability

For software companies like SoundHound AI, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

SoundHound AI’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 42.4% gross margin over the last year. That means SoundHound AI paid its providers a lot of money ($57.64 for every $100 in revenue) to run its business.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. SoundHound AI has seen gross margins decline by 33 percentage points over the last 2 year, which is among the worst in the software space.

2. Long Payback Periods Delay Returns

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

SoundHound AI’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

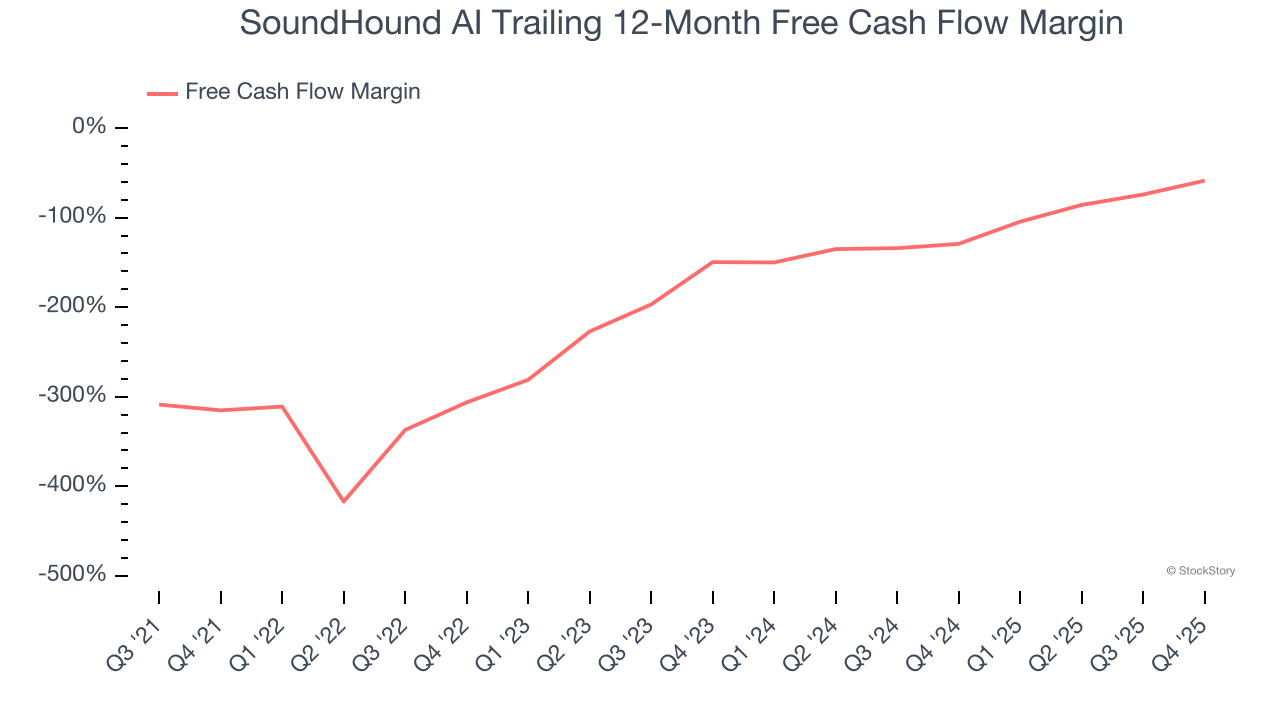

3. Cash Burn Ignites Concerns

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

SoundHound AI’s demanding reinvestments have drained its resources over the last year, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 58.7%, meaning it lit $58.68 of cash on fire for every $100 in revenue.

Final Judgment

SoundHound AI isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 15.6× forward price-to-sales (or $8.27 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.