Shareholders of DNOW would probably like to forget the past six months even happened. The stock dropped 23% and now trades at $12.34. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in DNOW, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is DNOW Not Exciting?

Even though the stock has become cheaper, we're cautious about DNOW. Here are three reasons there are better opportunities than DNOW and a stock we'd rather own.

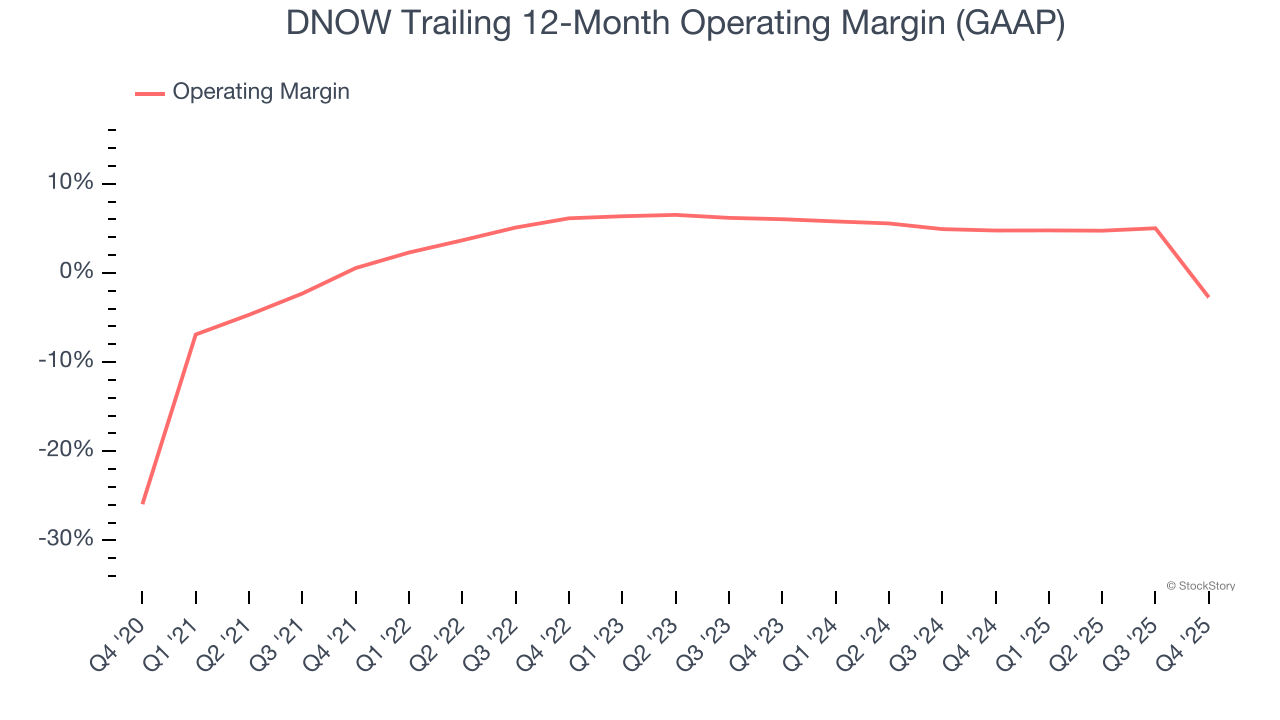

1. Weak Operating Margin Could Cause Trouble

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

DNOW was profitable over the last five years but held back by its large cost base. Its average operating margin of 2.8% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

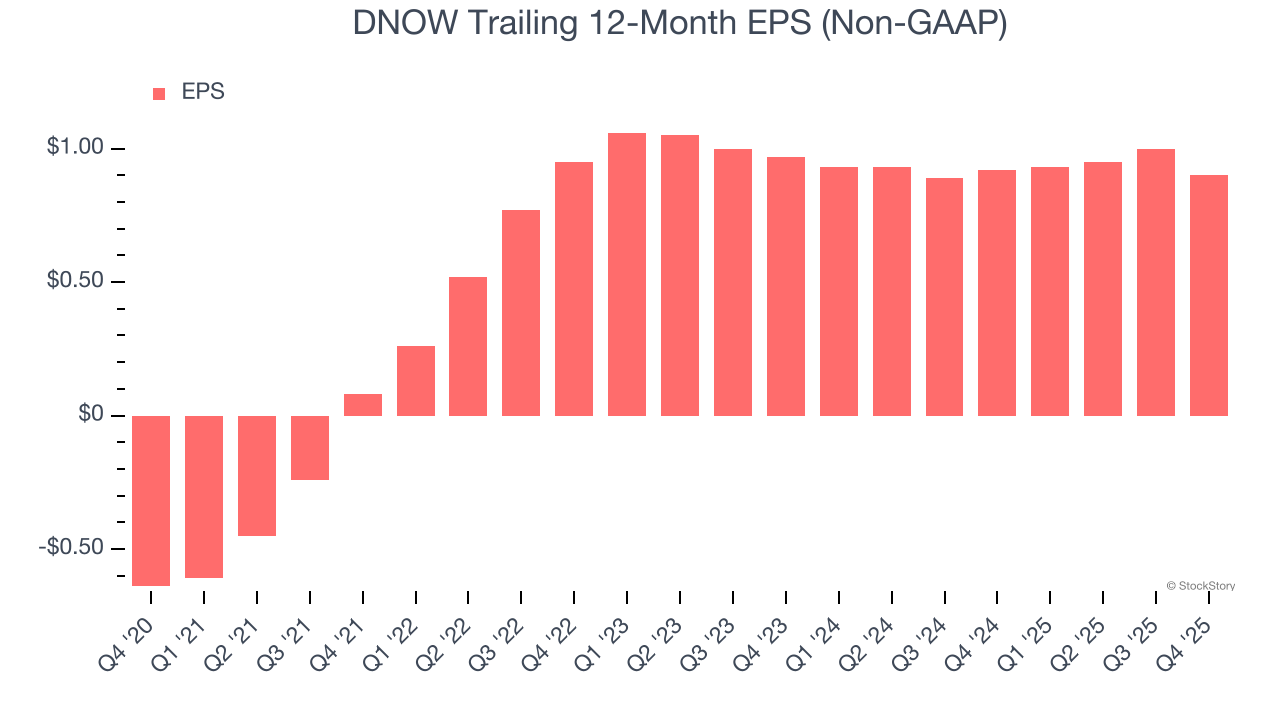

2. EPS Took a Dip Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for DNOW, its EPS declined by 3.7% annually over the last two years while its revenue grew by 10.2%. This tells us the company became less profitable on a per-share basis as it expanded.

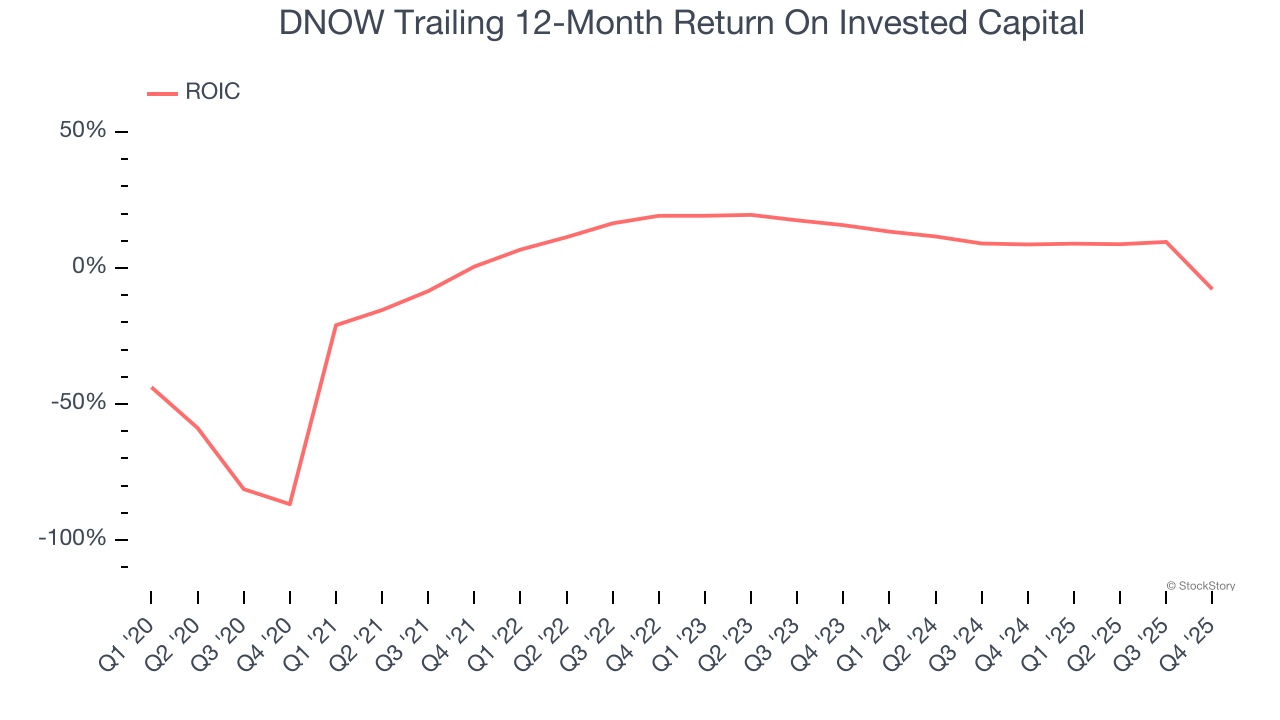

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, DNOW’s ROIC has unfortunately decreased. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

DNOW isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 16.5× forward P/E (or $12.34 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at one of our top digital advertising picks.

Stocks We Like More Than DNOW

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.