WD-40’s 11.9% return over the past six months has outpaced the S&P 500 by 5.4%, and its stock price has climbed to $239.59 per share. This performance may have investors wondering how to approach the situation.

Is now still a good time to buy WDFC? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Why Does WD-40 Spark Debate?

Short for “Water Displacement perfected on the 40th try”, WD-40 (NASDAQ: WDFC) is a renowned American consumer goods company known for its iconic and versatile spray, WD-40 Multi-Use Product.

Two Things to Like:

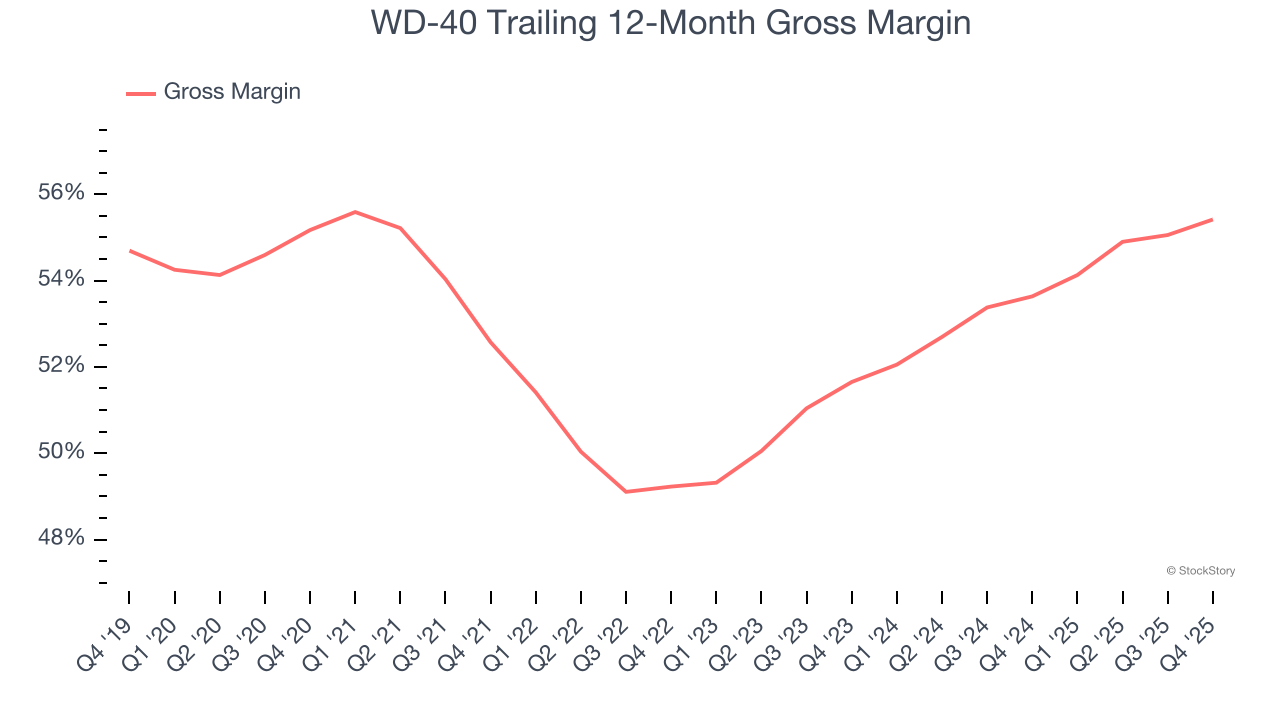

1. Elite Gross Margin Powers Best-In-Class Business Model

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products, has a stronger brand, and commands pricing power.

WD-40 has best-in-class unit economics for a consumer staples company, enabling it to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an elite 54.5% gross margin over the last two years. That means WD-40 only paid its suppliers $45.46 for every $100 in revenue.

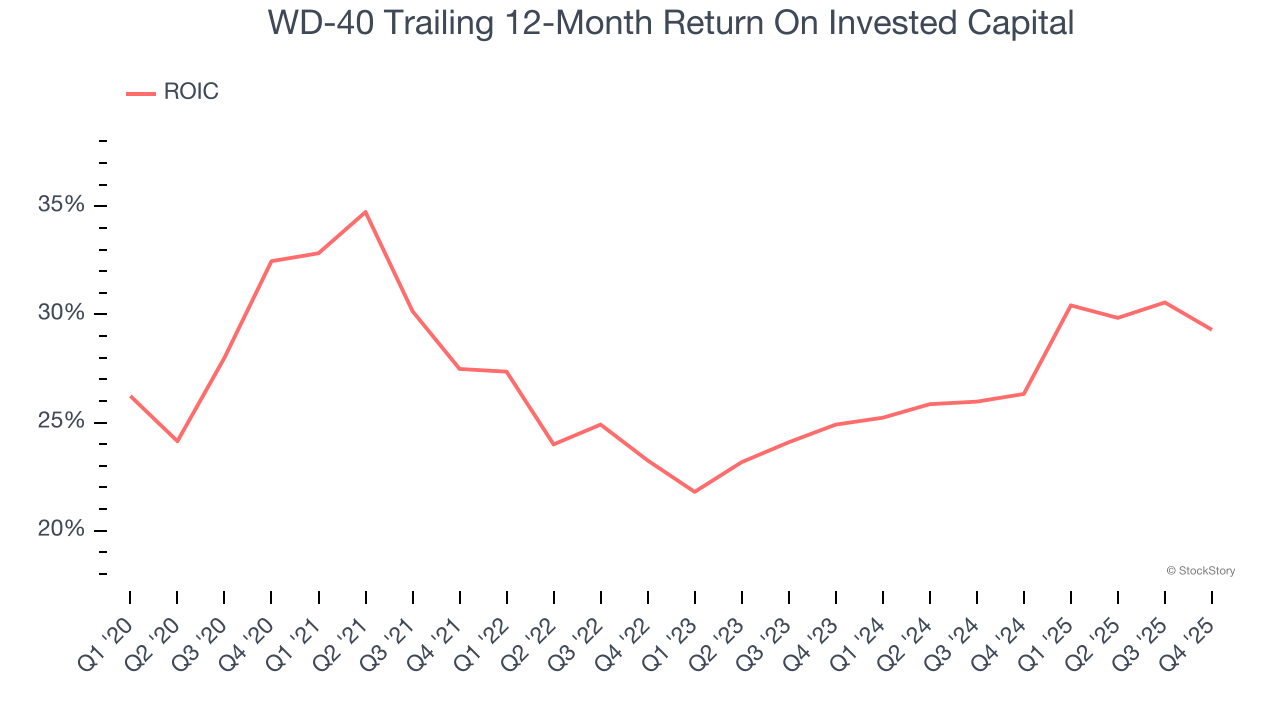

2. Stellar ROIC Showcases Lucrative Growth Opportunities

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

WD-40’s five-year average ROIC was 26.2%, placing it among the best consumer staples companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

One Reason to be Careful:

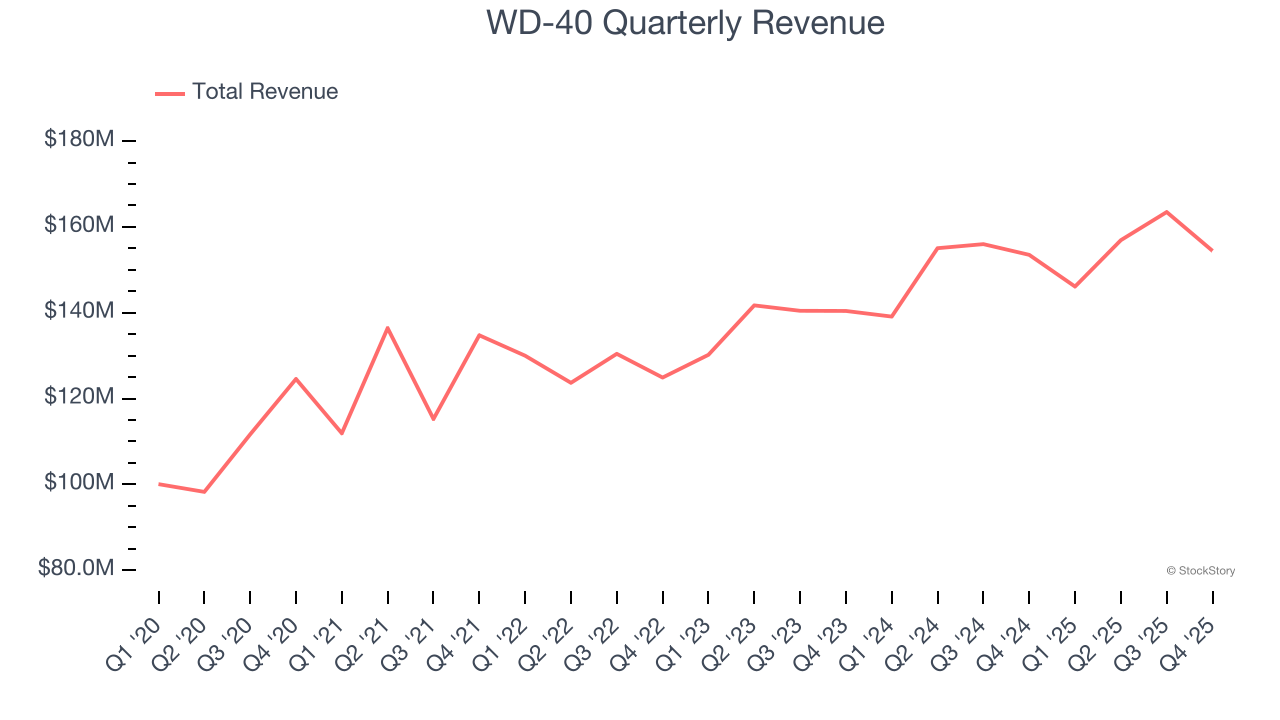

Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, WD-40’s 6.9% annualized revenue growth over the last three years was mediocre. This wasn’t a great result compared to the rest of the consumer staples sector, but there are still things to like about WD-40.

Final Judgment

WD-40 has huge potential even though it has some open questions, and with its shares outperforming the market lately, the stock trades at 38.4× forward P/E (or $239.59 per share). Is now a good time to buy? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.