Over the last six months, Zoetis’s shares have sunk to $129.91, producing a disappointing 16.4% loss - a stark contrast to the S&P 500’s 7.2% gain. This may have investors wondering how to approach the situation.

Given the weaker price action, is now the time to buy ZTS? Find out in our full research report, it’s free.

Why Does Zoetis Spark Debate?

Originally spun off from Pfizer in 2013 as the world's largest pure-play animal health company, Zoetis (NYSE: ZTS) discovers, develops, and sells medicines, vaccines, diagnostic products, and services for pets and livestock animals worldwide.

Two Positive Attributes:

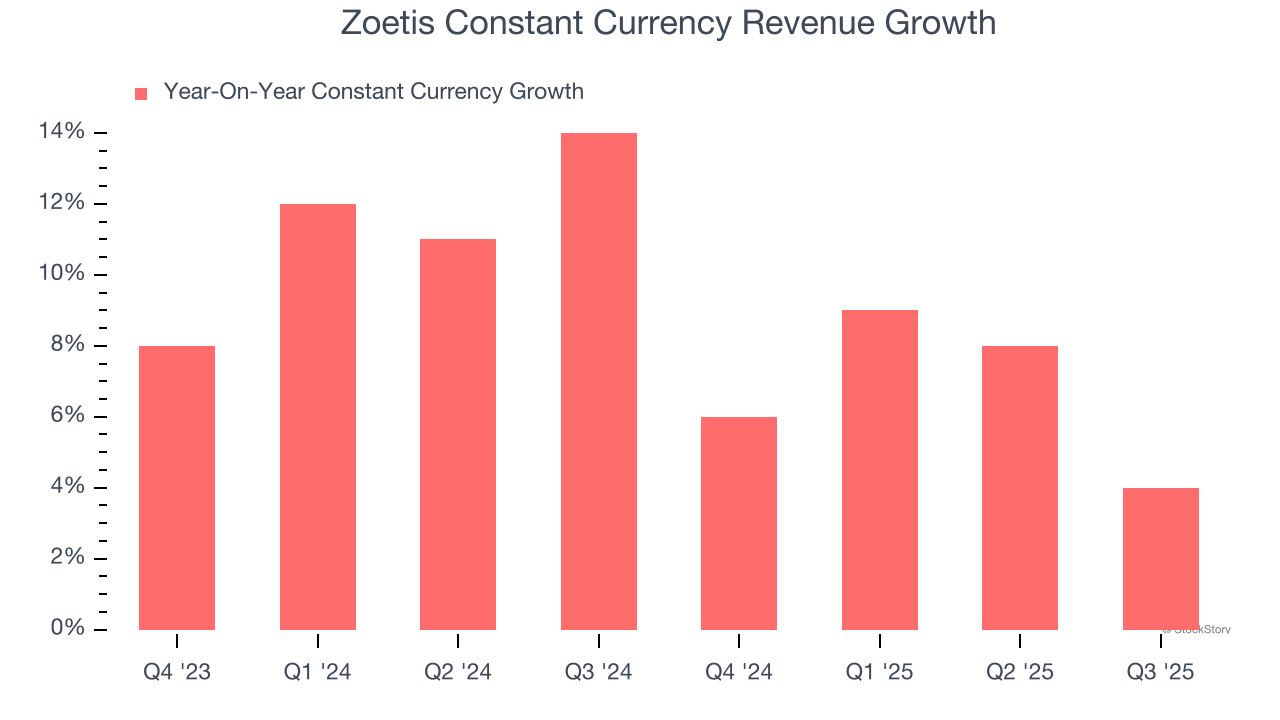

1. Constant Currency Revenue Drives Growth

In addition to reported revenue, constant currency revenue is a useful data point for analyzing Branded Pharmaceuticals companies. This metric excludes currency movements, which are outside of Zoetis’s control and are not indicative of underlying demand.

Over the last two years, Zoetis’s constant currency revenue averaged 9.1% year-on-year growth. This performance was solid and shows it can expand steadily on a global scale regardless of the macroeconomic environment.

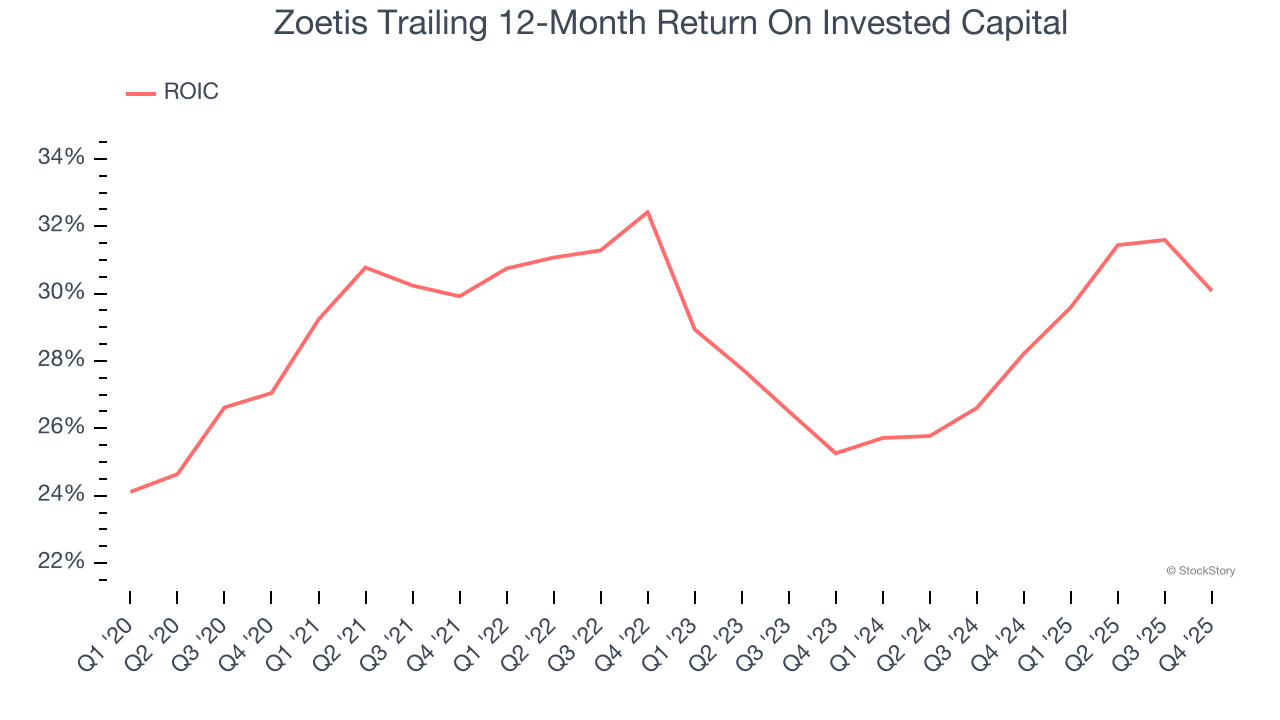

2. Stellar ROIC Showcases Lucrative Growth Opportunities

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Zoetis’s five-year average ROIC was 29.2%, placing it among the best healthcare companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

One Reason to be Careful:

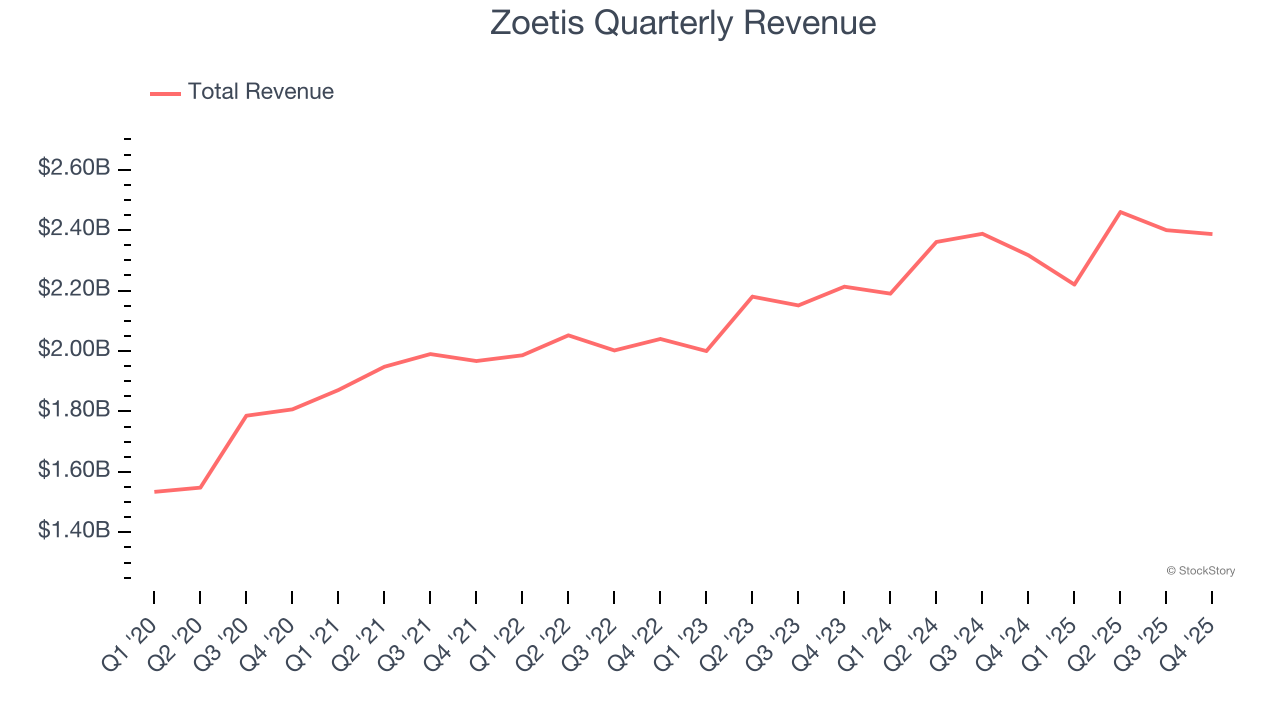

Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Zoetis’s sales grew at a mediocre 7.2% compounded annual growth rate over the last five years. This wasn’t a great result compared to the rest of the healthcare sector, but there are still things to like about Zoetis.

Final Judgment

Zoetis has huge potential even though it has some open questions. After the recent drawdown, the stock trades at 18.4× forward P/E (or $129.91 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.