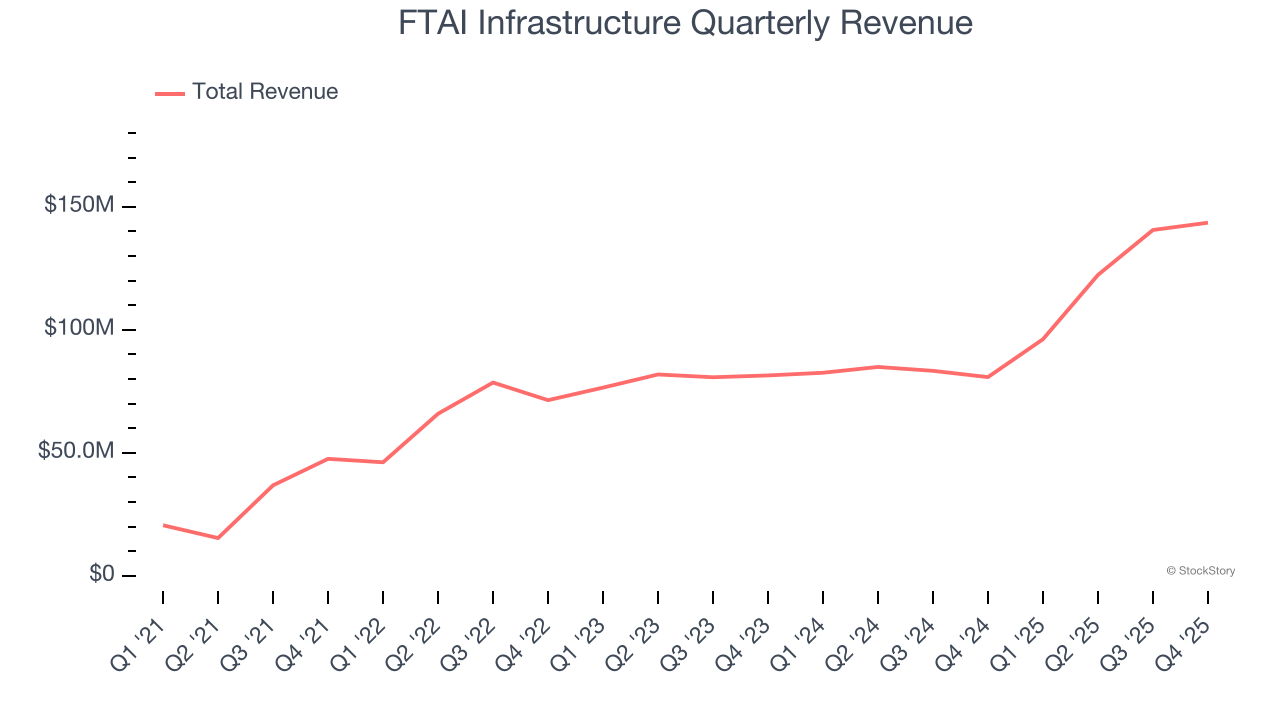

Infrastructure investment and operations firm FTAI Infrastructure (NASDAQ: FIP) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 77.7% year on year to $143.5 million. Its GAAP loss of $1.08 per share was significantly below analysts’ consensus estimates.

Is now the time to buy FTAI Infrastructure? Find out by accessing our full research report, it’s free.

FTAI Infrastructure (FIP) Q4 CY2025 Highlights:

- Revenue: $143.5 million vs analyst estimates of $169.2 million (77.7% year-on-year growth, 15.2% miss)

- EPS (GAAP): -$1.08 vs analyst estimates of -$0.43 (significant miss)

- Adjusted EBITDA: $89.16 million vs analyst estimates of $77.73 million (62.1% margin, 14.7% beat)

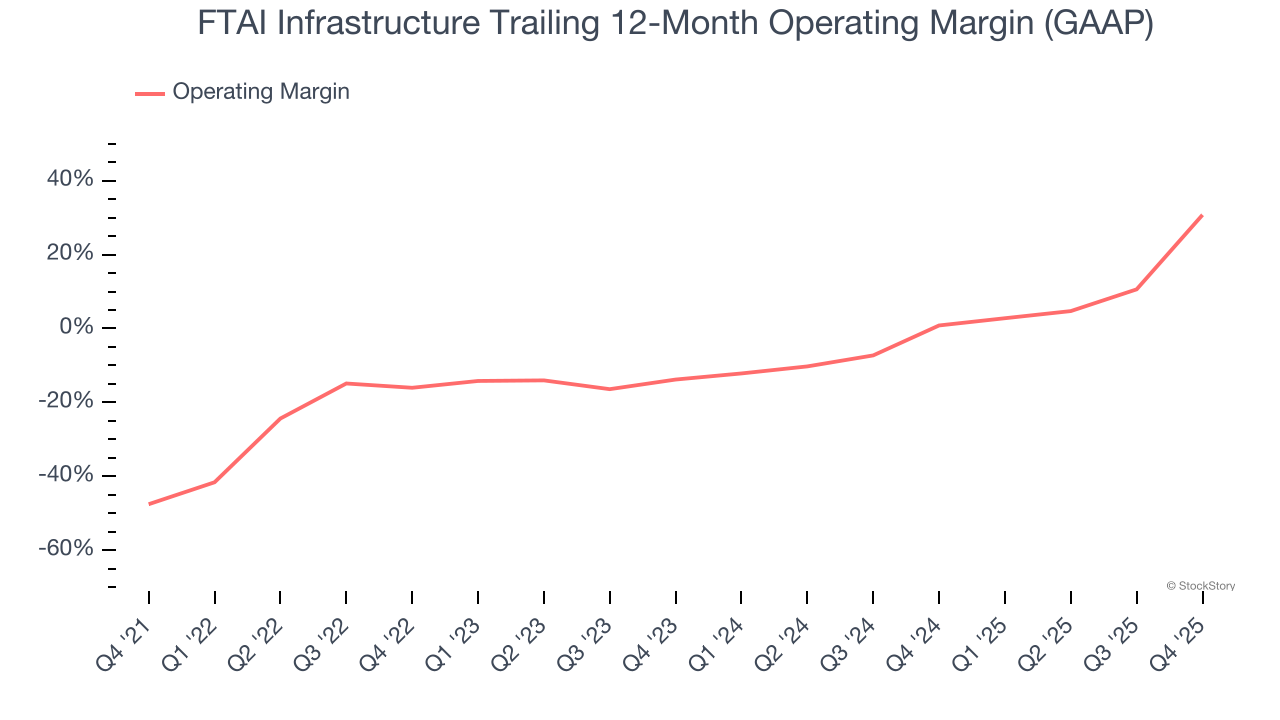

- Operating Margin: 88.9%, up from 24.4% in the same quarter last year

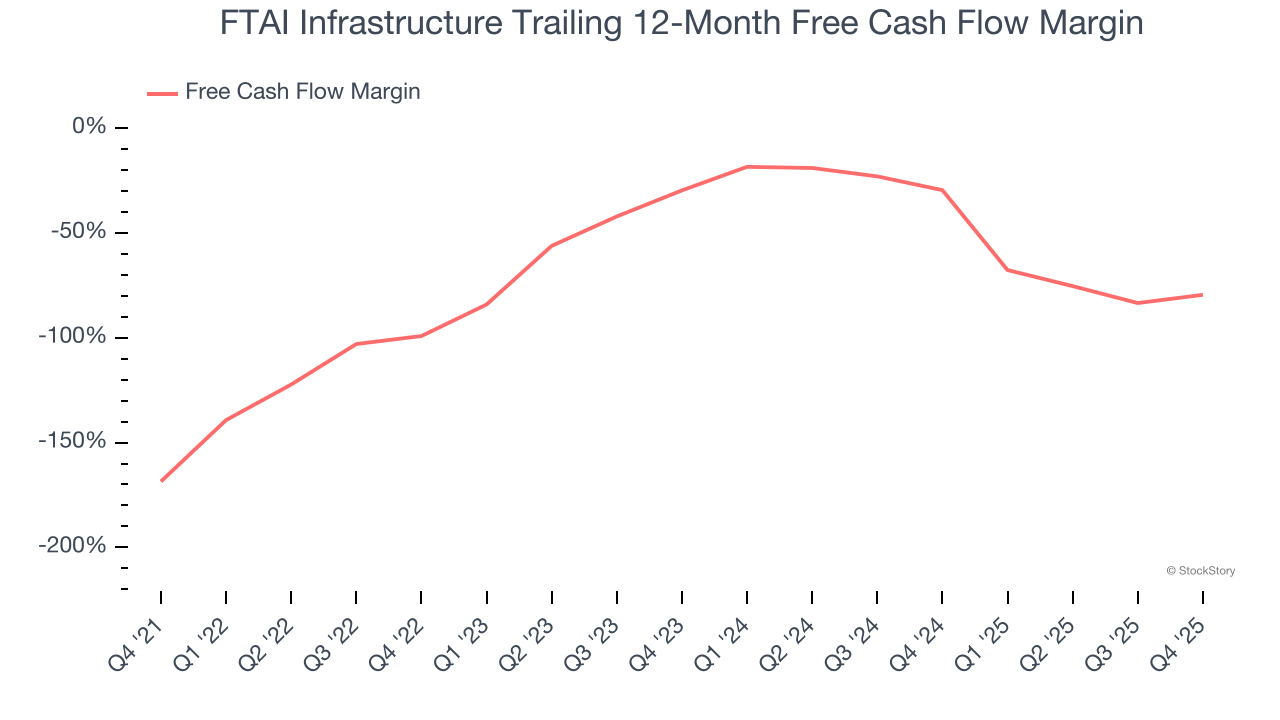

- Free Cash Flow was -$68.64 million compared to -$35.93 million in the same quarter last year

- Market Capitalization: $744.3 million

Company Overview

Spun off from FTAI Aviation in 2021, FTAI Infrastructure (NASDAQ: FIP) invests in and operates infrastructure and related assets across the transportation and energy sectors.

Revenue Growth

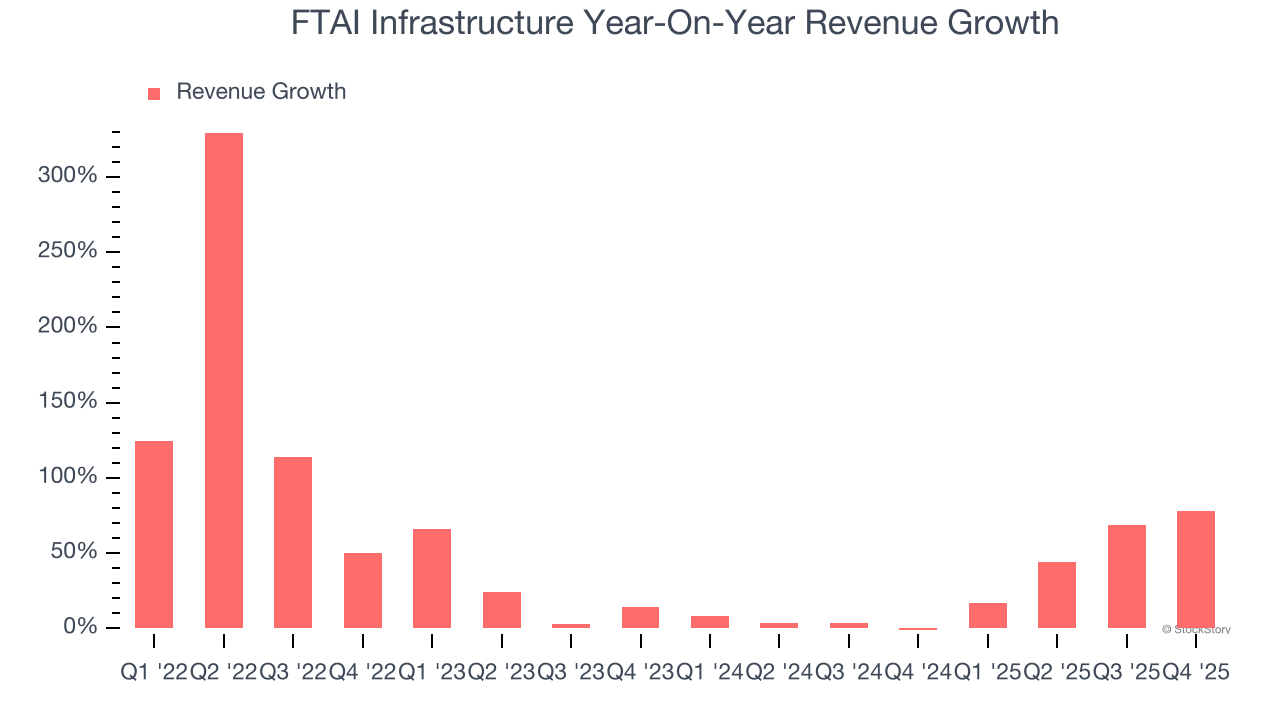

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last four years, FTAI Infrastructure grew its sales at an incredible 43% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. FTAI Infrastructure’s annualized revenue growth of 25.2% over the last two years is below its four-year trend, but we still think the results suggest healthy demand.

This quarter, FTAI Infrastructure achieved a magnificent 77.7% year-on-year revenue growth rate, but its $143.5 million of revenue fell short of Wall Street’s lofty estimates.

Looking ahead, sell-side analysts expect revenue to grow 65.7% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and implies its newer products and services will spur better top-line performance.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

FTAI Infrastructure was roughly breakeven when averaging the last five years of quarterly operating profits, inadequate for an industrials business. This result is surprising given its high gross margin as a starting point.

On the plus side, FTAI Infrastructure’s operating margin rose by 78.3 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, FTAI Infrastructure generated an operating margin profit margin of 88.9%, up 64.5 percentage points year on year. The increase was driven by stronger leverage on its cost of sales (not higher efficiency with its operating expenses), as indicated by its larger rise in gross margin.

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

FTAI Infrastructure’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 68.7%, meaning it lit $68.68 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that FTAI Infrastructure’s margin expanded by 89 percentage points during that time. In light of its glaring cash burn, however, this improvement is a bucket of hot water in a cold ocean.

FTAI Infrastructure burned through $68.64 million of cash in Q4, equivalent to a negative 47.8% margin. The company’s cash burn increased from $35.93 million of lost cash in the same quarter last year.

Key Takeaways from FTAI Infrastructure’s Q4 Results

We were impressed by how significantly FTAI Infrastructure blew past analysts’ EBITDA expectations this quarter. On the other hand, its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 1.6% to $6.34 immediately following the results.

FTAI Infrastructure’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).