Since July 2025, McDonald's has been in a holding pattern, posting a small return of 1.5% while floating around $306.50. The stock also fell short of the S&P 500’s 11.1% gain during that period.

Is now the time to buy MCD? Find out in our full research report, it’s free.

Why Does McDonald's Spark Debate?

With nicknames spanning Mickey D's in the U.S. to Makku in Japan, McDonald’s (NYSE: MCD) is a fast-food behemoth known for its convenience and broken ice cream machines.

Two Things to Like:

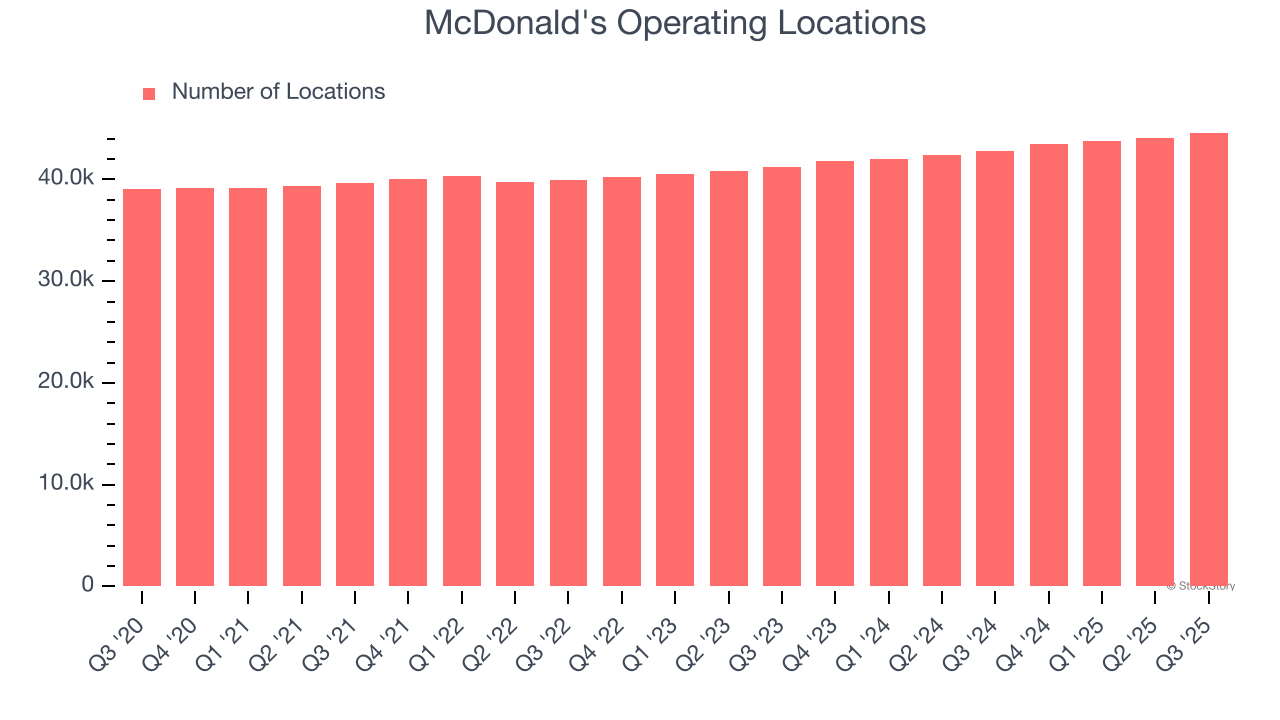

1. Restaurant Growth Signals an Offensive Strategy

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

McDonald's operated 44,599 locations in the latest quarter. It has opened new restaurants at a rapid clip over the last two years, averaging 4% annual growth, much faster than the broader restaurant sector. Furthermore, one dynamic making expansion more seamless is the company’s franchise model, where franchisees are primarily responsible for opening new restaurants while McDonald's provides support.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

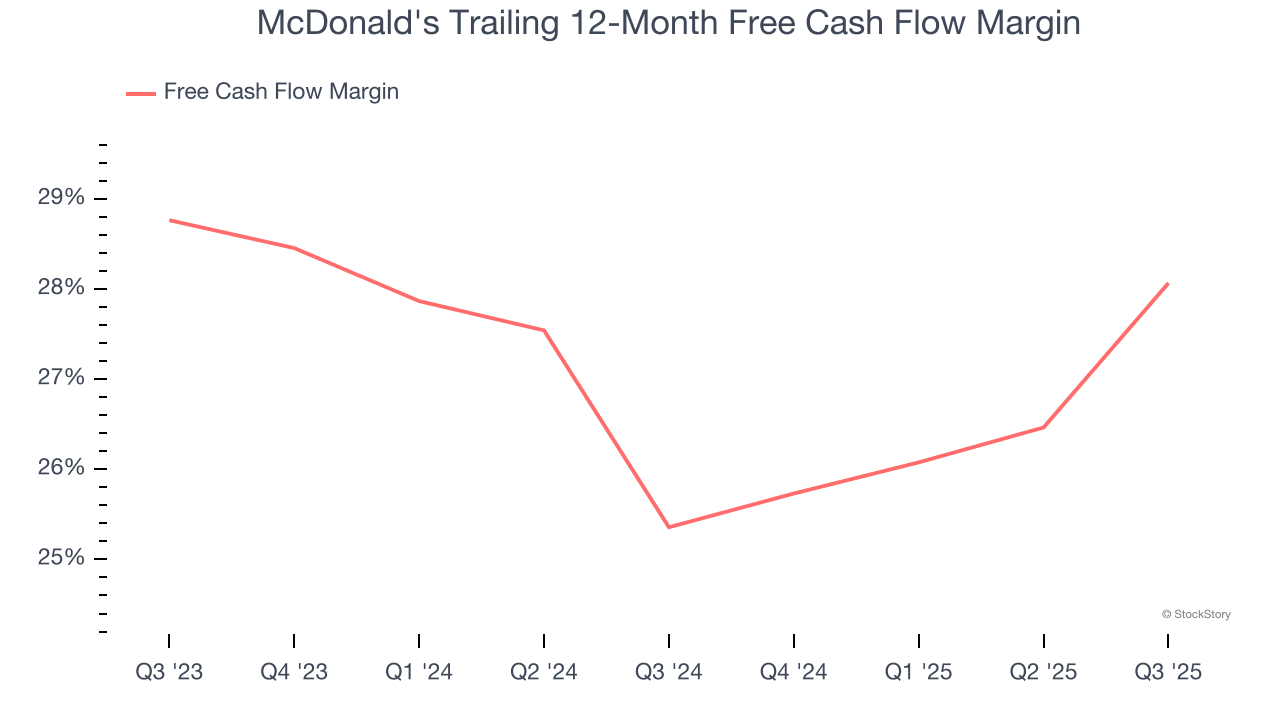

2. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

McDonald's has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the restaurant sector, averaging 26.7% over the last two years.

One Reason to be Careful:

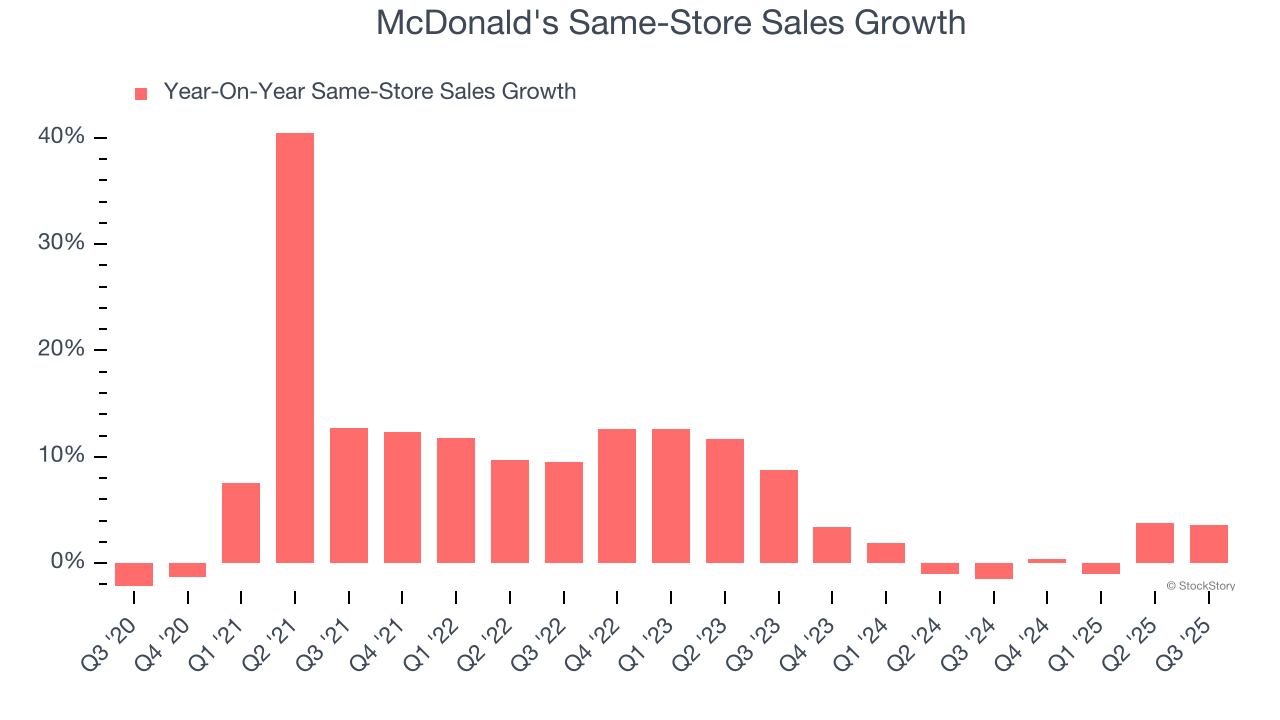

Same-Store Sales Falling Behind Peers

Same-store sales show the change in sales at restaurants open for at least a year. This is a key performance indicator because it measures organic growth.

McDonald’s demand within its existing dining locations has been relatively stable over the last two years but was below most restaurant chains. On average, the company’s same-store sales have grown by 1.2% per year.

Final Judgment

McDonald’s positive characteristics outweigh the negatives. With its shares trailing the market in recent months, the stock trades at 23.7× forward P/E (or $306.50 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than McDonald's

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.