What a time it’s been for Marqeta. In the past six months alone, the company’s stock price has increased by a massive 60.2%, reaching $6.15 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Marqeta, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Marqeta Not Exciting?

Despite the momentum, we're sitting this one out for now. Here are three reasons why we avoid MQ and a stock we'd rather own.

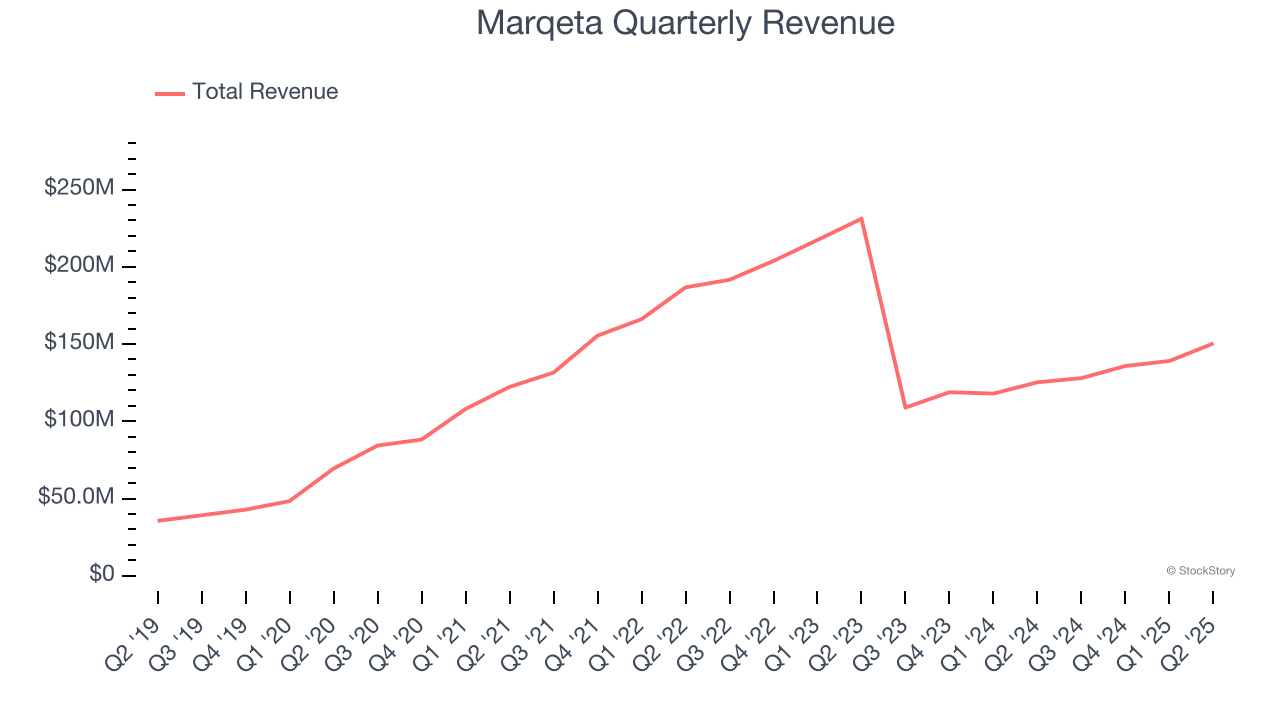

1. Revenue Spiraling Downwards

A company’s long-term sales performance is one signal of its overall quality.

Any business can put up a good quarter or two, but many enduring ones grow for years.

Over the last three years, Marqeta’s demand was weak and its revenue declined by 4.7% per year. This was below our standards and signals it’s a lower quality business.

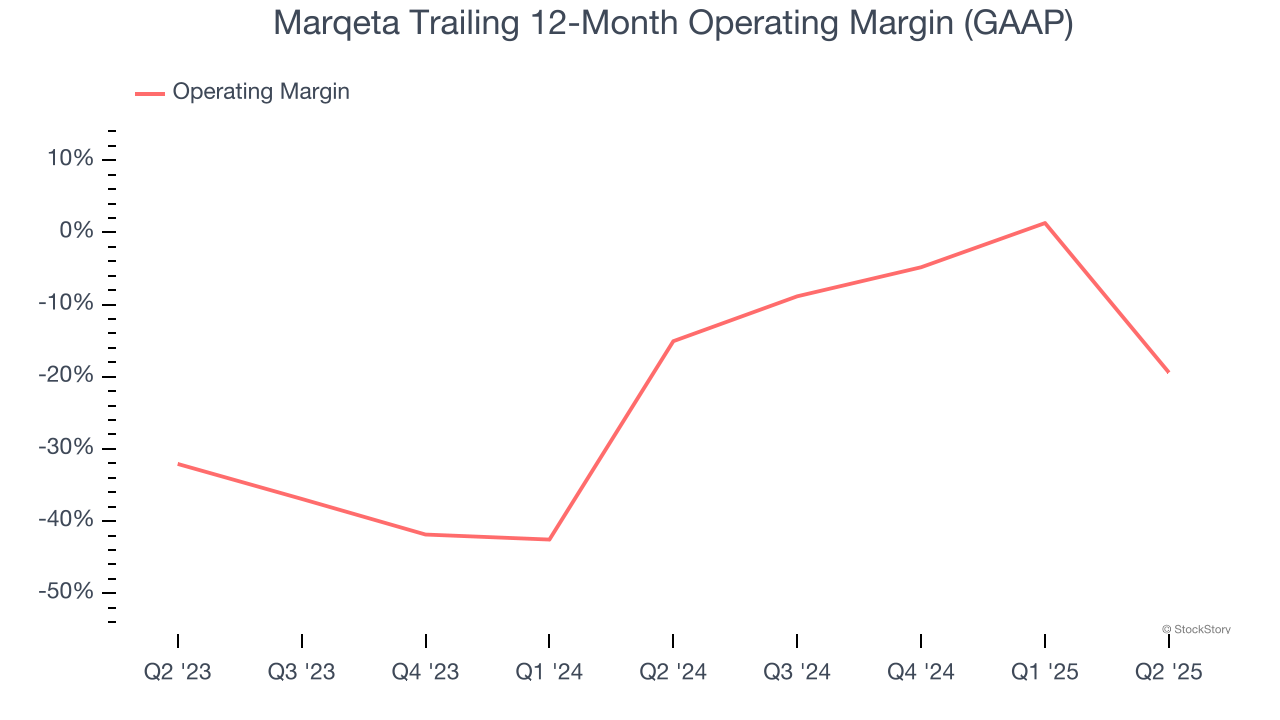

2. Shrinking Operating Margin

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Analyzing the trend in its profitability, Marqeta’s operating margin decreased by 4.3 percentage points over the last year. Marqeta’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was negative 19.4%.

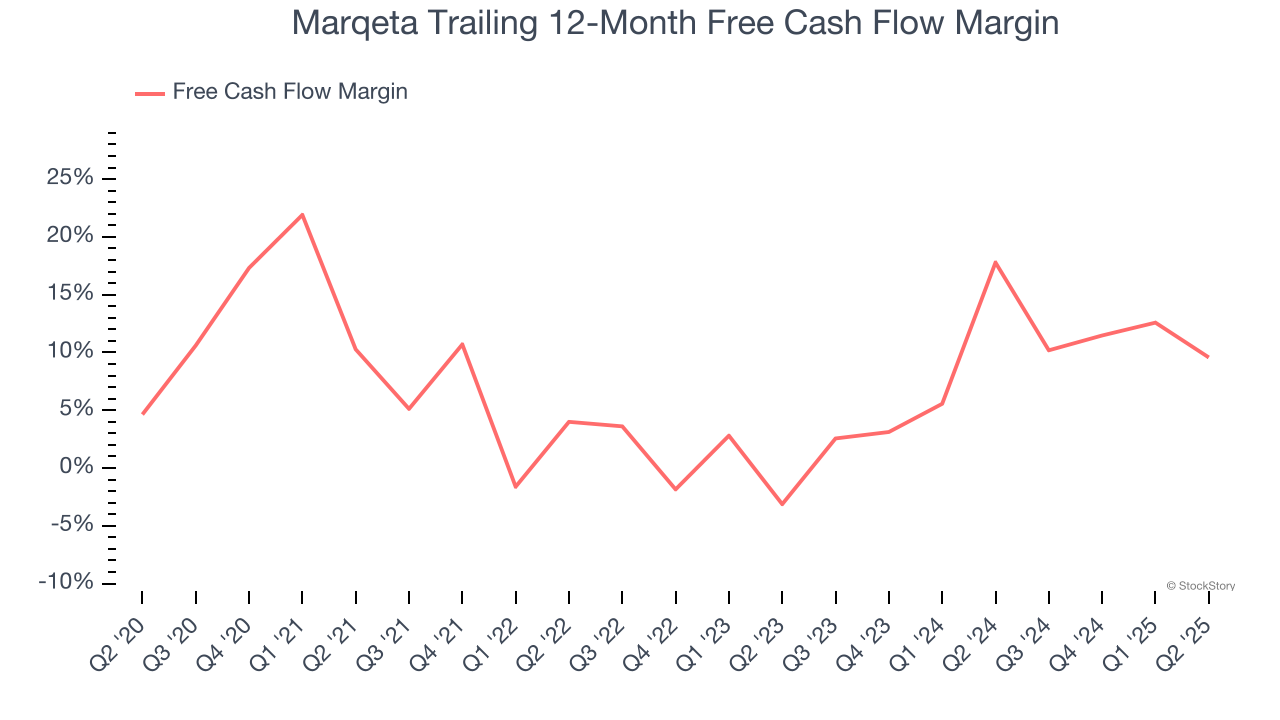

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Marqeta has shown mediocre cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 9.6%, subpar for a software business.

Final Judgment

Marqeta’s business quality ultimately falls short of our standards. Following the recent surge, the stock trades at 4.4× forward price-to-sales (or $6.15 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward our favorite semiconductor picks and shovels play.

Stocks We Like More Than Marqeta

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.