Marriott currently trades at $277.60 per share and has shown little upside over the past six months, posting a middling return of 0.8%.

Is there a buying opportunity in Marriott, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Marriott Not Exciting?

We're swiping left on Marriott for now. Here are three reasons why we avoid MAR and a stock we'd rather own.

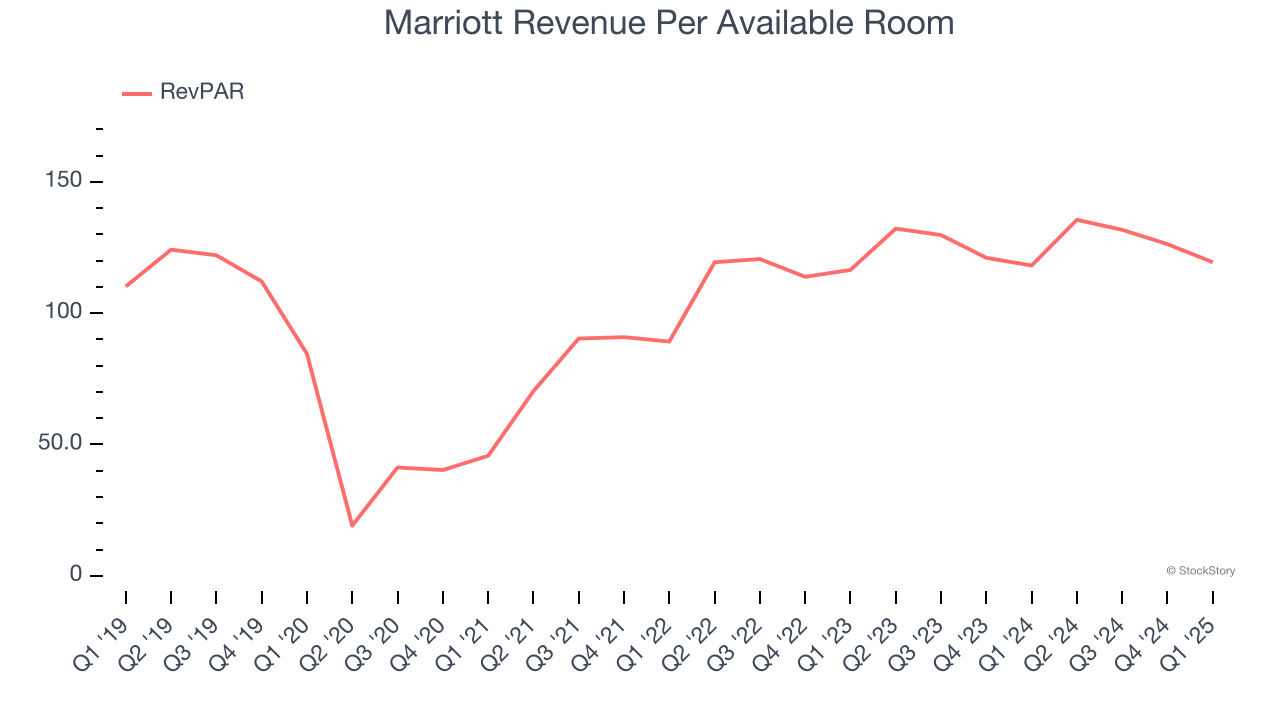

1. Weak RevPAR Growth Points to Soft Demand

Investors interested in Travel and Vacation Providers companies should track RevPAR (revenue per available room) in addition to reported revenue. This metric accounts for daily rates and occupancy levels, painting a holistic picture of Marriott’s demand characteristics.

Marriott’s RevPAR came in at $119.38 in the latest quarter, and over the last two years, its year-on-year growth averaged 4.4%. This performance was underwhelming and suggests it might have to invest in new amenities such as restaurants and bars to attract customers - this isn’t ideal because expansions can complicate operations and be quite expensive (i.e., renovations and increased overhead).

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Marriott’s revenue to rise by 4%, a slight deceleration versus its 4.2% annualized growth for the past five years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

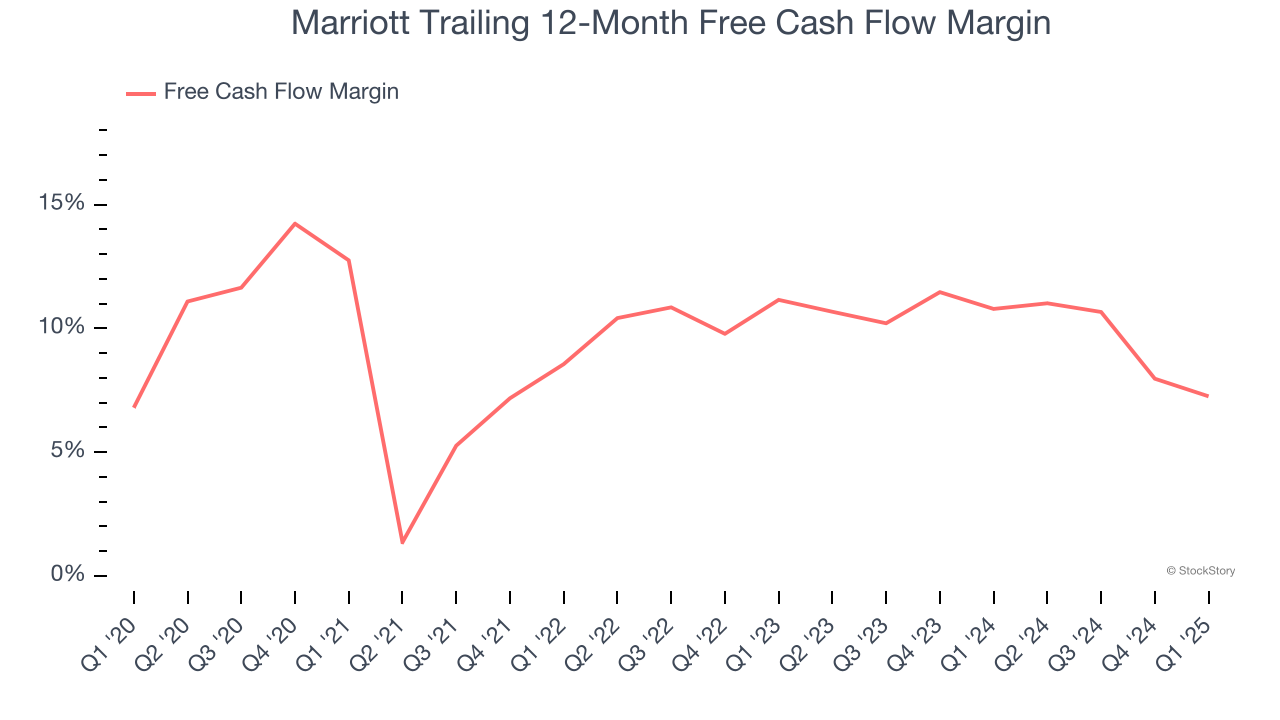

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Marriott has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 9%, subpar for a consumer discretionary business.

Final Judgment

Marriott’s business quality ultimately falls short of our standards. That said, the stock currently trades at 27× forward P/E (or $277.60 per share). At this valuation, there’s a lot of good news priced in - we think there are better opportunities elsewhere. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

High-Quality Stocks for All Market Conditions

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.