Although the S&P 500 is down 1.6% over the past six months, Gorman-Rupp’s stock price has fallen further to $35.58, losing shareholders 8.9% of their capital. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Following the pullback, is now a good time to buy GRC? Find out in our full research report, it’s free.

Why Does Gorman-Rupp Spark Debate?

Powering fluid dynamics since 1934, Gorman-Rupp (NYSE: GRC) has evolved from its Ohio origins into a global manufacturer and seller of pumps and pump systems.

Two Things to Like:

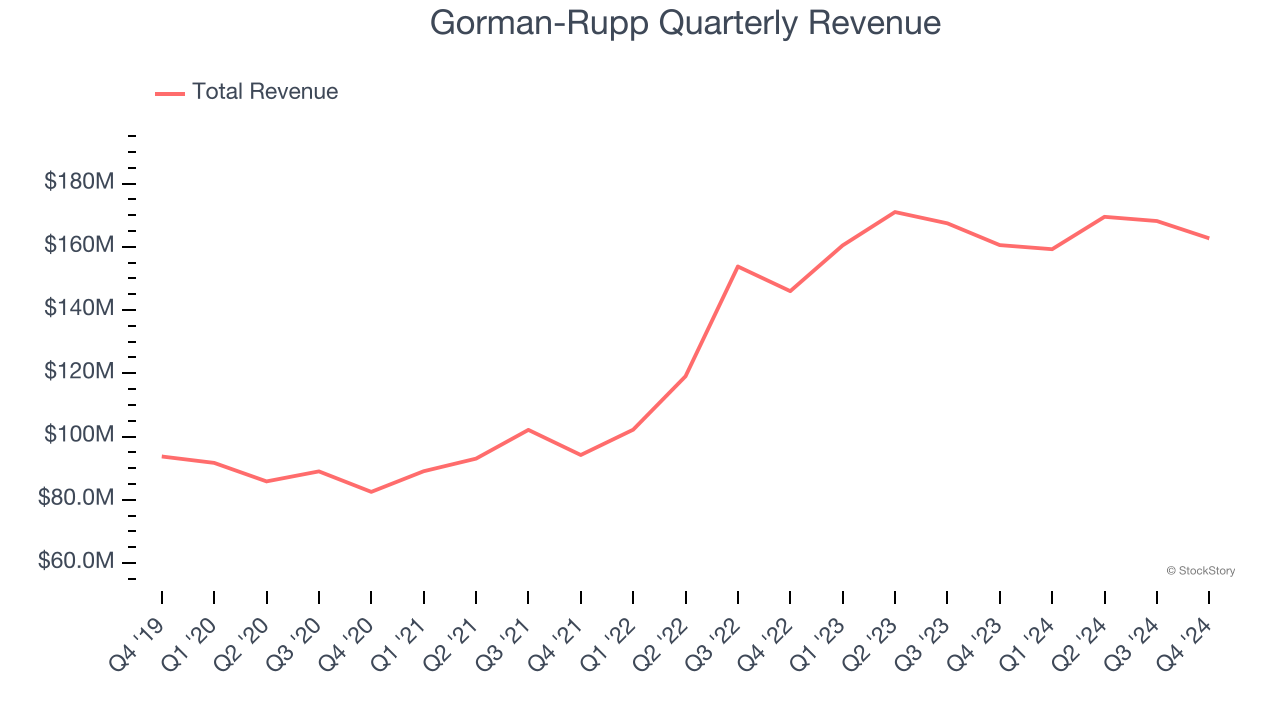

1. Skyrocketing Revenue Shows Strong Momentum

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Gorman-Rupp’s sales grew at an impressive 10.6% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

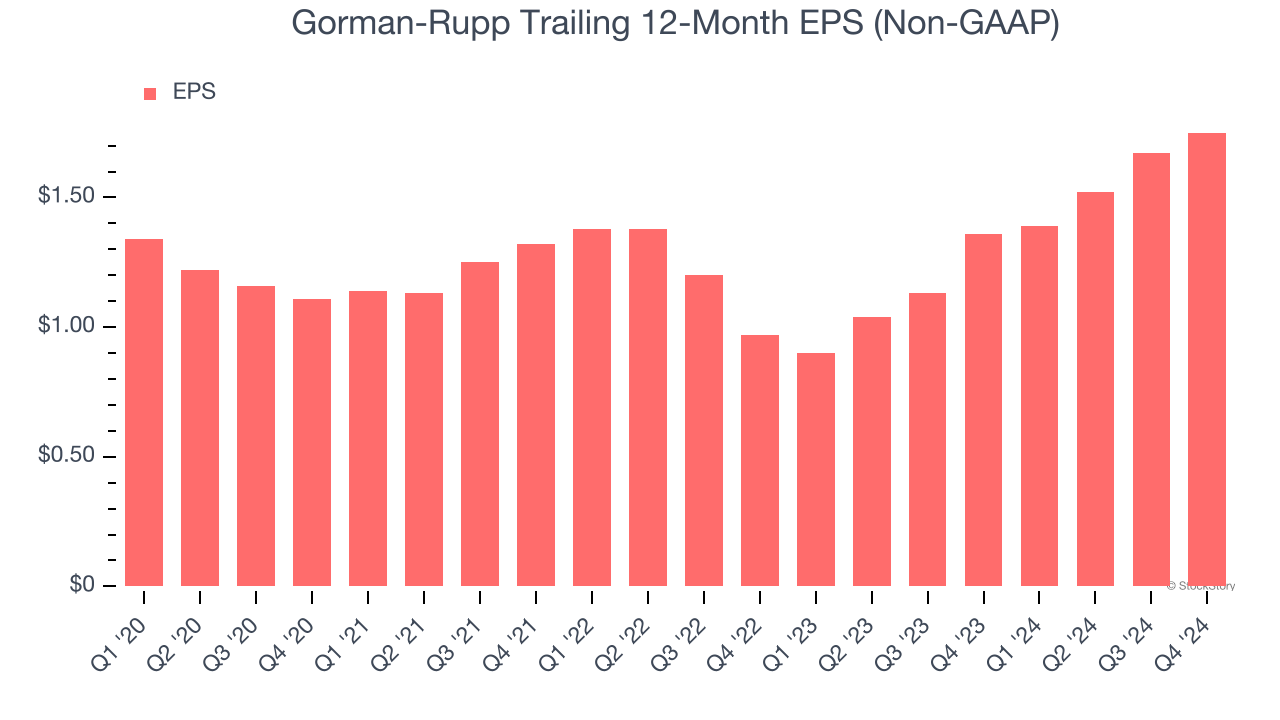

2. EPS Surges Higher Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Gorman-Rupp’s EPS grew at an astounding 34.3% compounded annual growth rate over the last two years, higher than its 12.5% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

One Reason to be Careful:

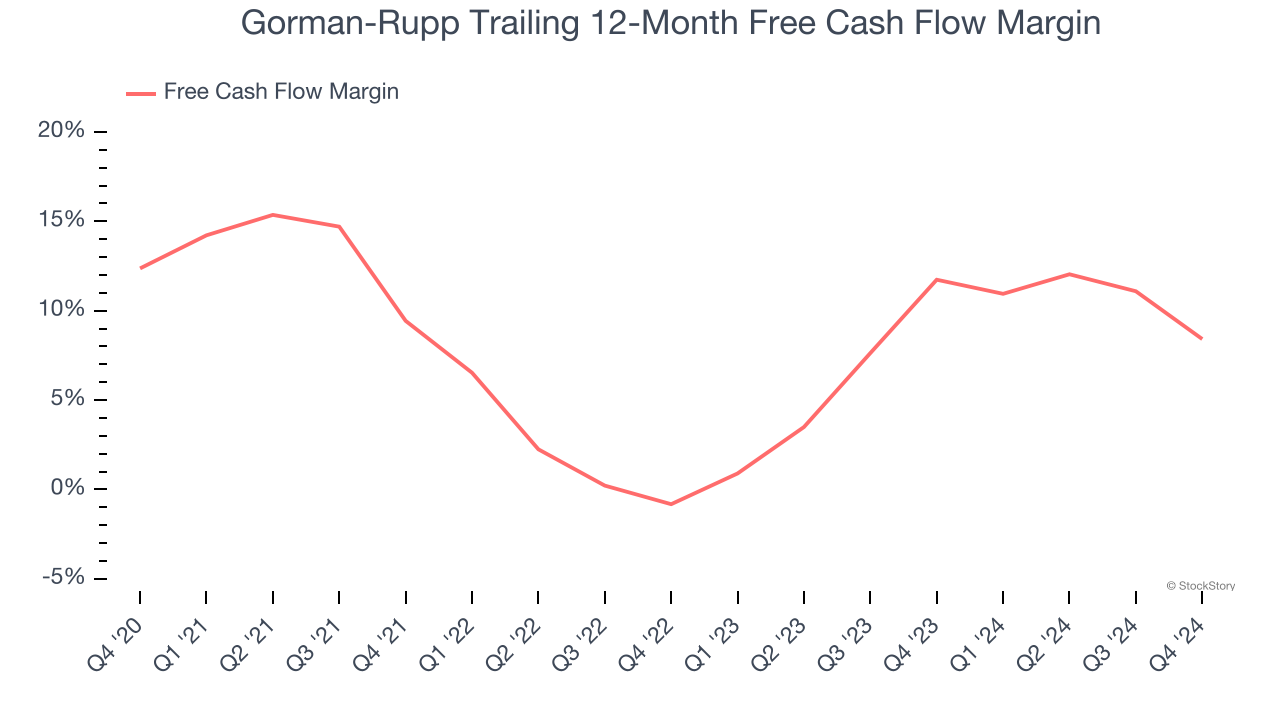

Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Gorman-Rupp’s margin dropped by 4 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Gorman-Rupp’s free cash flow margin for the trailing 12 months was 8.4%.

Final Judgment

Gorman-Rupp’s positive characteristics outweigh the negatives. With the recent decline, the stock trades at 18.1× forward price-to-earnings (or $35.58 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Gorman-Rupp

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.