Myriad Genetics’s stock price has taken a beating over the past six months, shedding 47.8% of its value and falling to $14.75 per share. This might have investors contemplating their next move.

Is there a buying opportunity in Myriad Genetics, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons why there are better opportunities than MYGN and a stock we'd rather own.

Why Do We Think Myriad Genetics Will Underperform?

Founded in 1991, Myriad Genetics (NASDAQ: MYGN) provides genetic testing and precision medicine solutions, with a focus on identifying hereditary risks for cancer, guiding treatment decisions, and supporting mental health diagnosis.

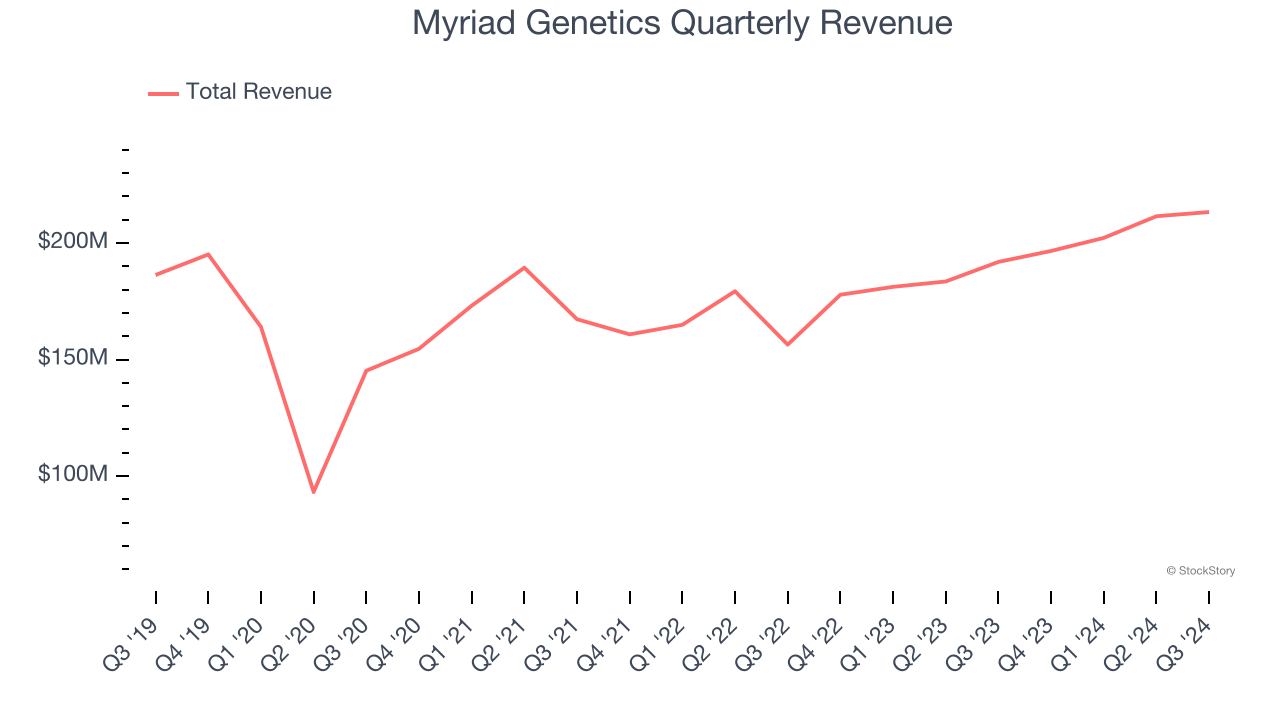

1. Long-Term Revenue Growth Flatter Than a Pancake

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Unfortunately, Myriad Genetics struggled to consistently increase demand as its $823.6 million of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and signals it’s a low quality business.

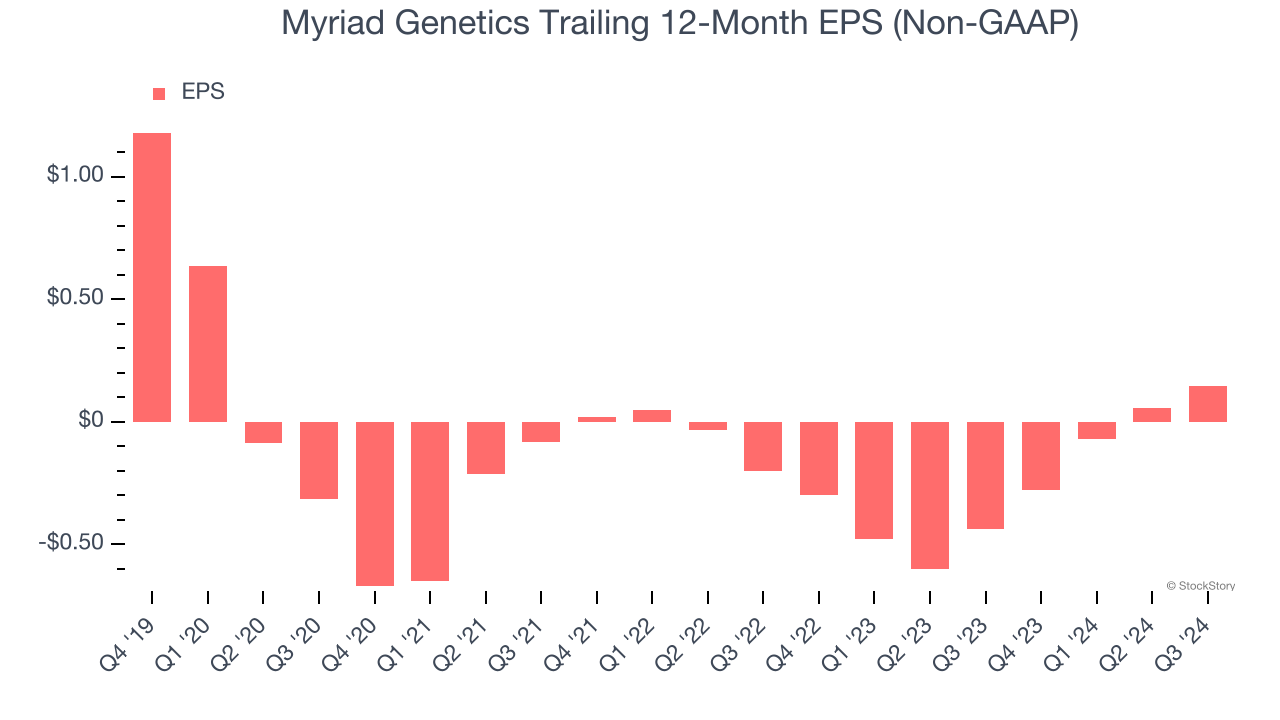

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Myriad Genetics, its EPS declined by 35.7% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

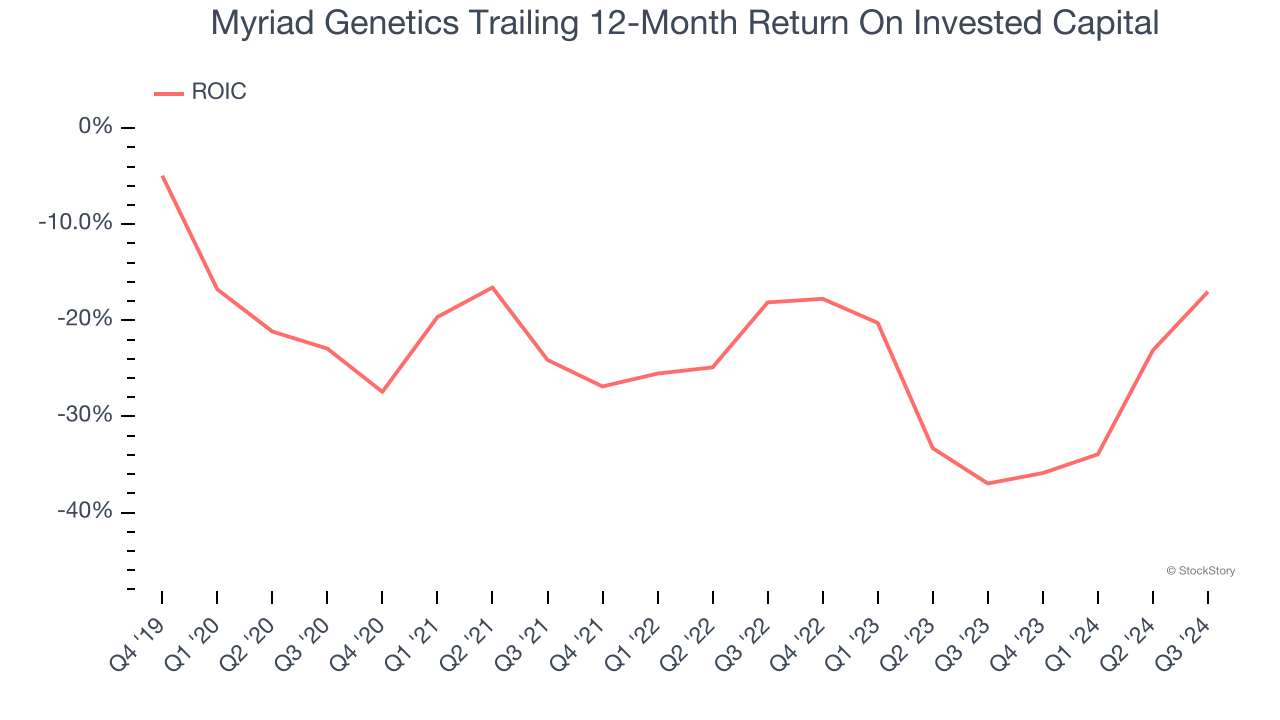

3. Previous Growth Initiatives Have Lost Money

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Myriad Genetics’s five-year average ROIC was negative 23.8%, meaning management lost money while trying to expand the business. Its returns were among the worst in the healthcare sector.

Final Judgment

Myriad Genetics falls short of our quality standards. After the recent drawdown, the stock trades at 71.2× forward price-to-earnings (or $14.75 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. We’d suggest looking at the most dominant software business in the world.

Stocks We Would Buy Instead of Myriad Genetics

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.