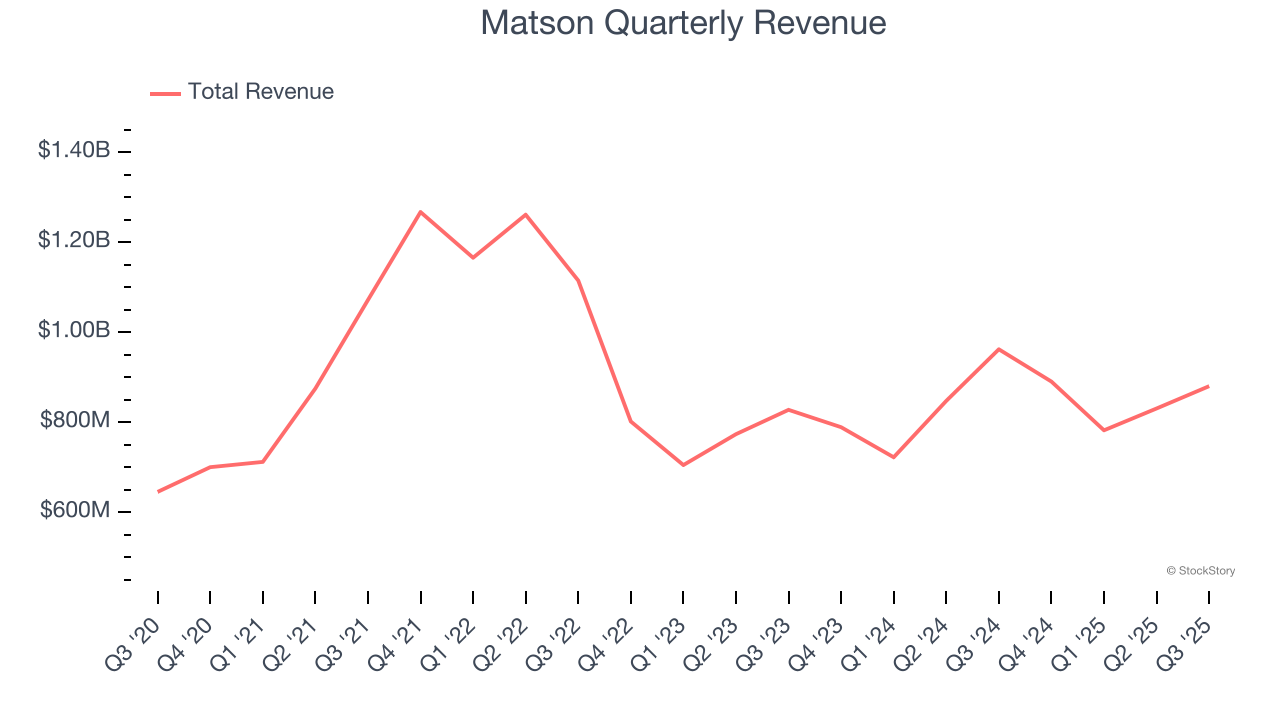

Maritime transportation company Matson (NYSE: MATX) reported Q3 CY2025 results exceeding the market’s revenue expectations, but sales fell by 8.5% year on year to $880.1 million. Its GAAP profit of $4.24 per share was 30.3% above analysts’ consensus estimates.

Is now the time to buy Matson? Find out by accessing our full research report, it’s free for active Edge members.

Matson (MATX) Q3 CY2025 Highlights:

- Revenue: $880.1 million vs analyst estimates of $837.4 million (8.5% year-on-year decline, 5.1% beat)

- EPS (GAAP): $4.24 vs analyst estimates of $3.25 (30.3% beat)

- Adjusted EBITDA: $212.3 million vs analyst estimates of $167 million (24.1% margin, 27.1% beat)

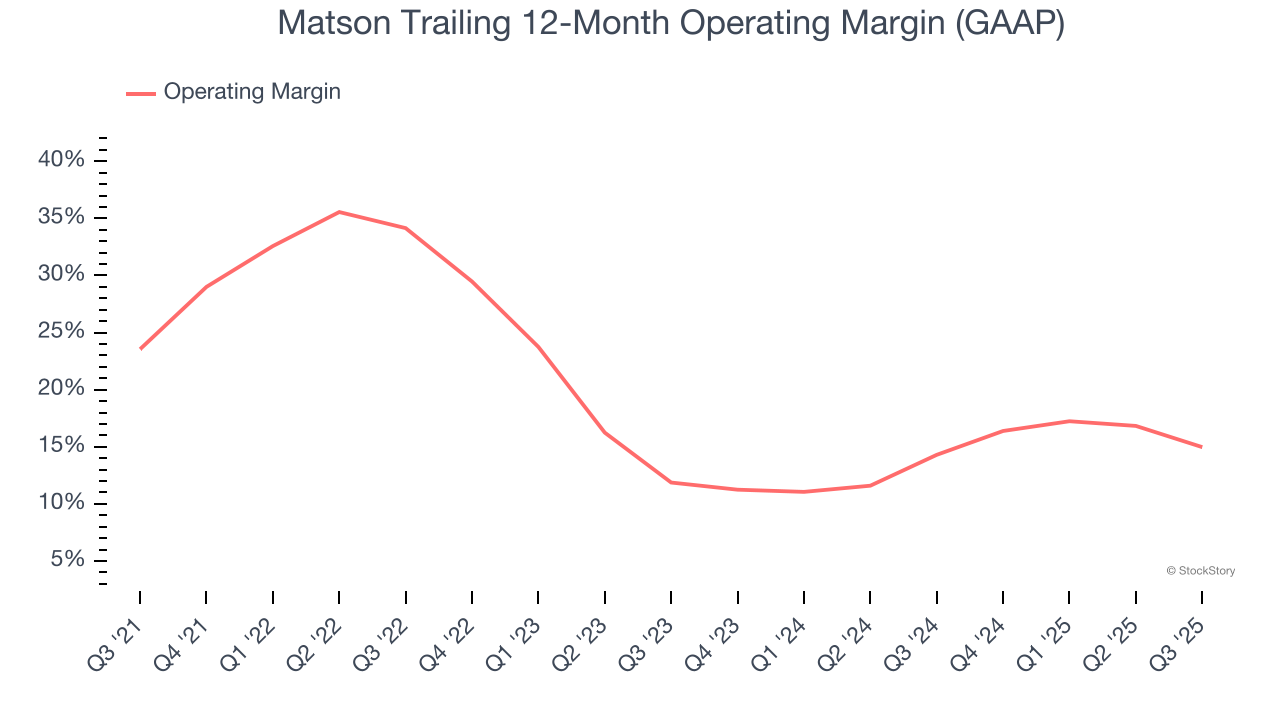

- Operating Margin: 18.3%, down from 24.7% in the same quarter last year

- Free Cash Flow Margin: 26.6%, up from 19.6% in the same quarter last year

- Market Capitalization: $3.18 billion

Matt Cox, Matson's Chairman and Chief Executive Officer, commented, "Matson's Ocean Transportation and Logistics business segments performed well in a difficult environment marked by continued uncertainty and volatility arising from tariffs and global trade. In Ocean Transportation, our operating income was lower year-over-year primarily due to lower year-over-year freight rates and container volume in our China service. The Transpacific tradelane experienced a muted peak season compared to the elevated demand levels last year due to businesses advancing cargo in the late second quarter and early third quarter ahead of U.S. tariff deadlines, which led to lower third quarter demand for our expedited services."

Company Overview

Founded by a Swedish orphan, Matson (NYSE: MATX) is a provider of ocean transportation and logistics services.

Revenue Growth

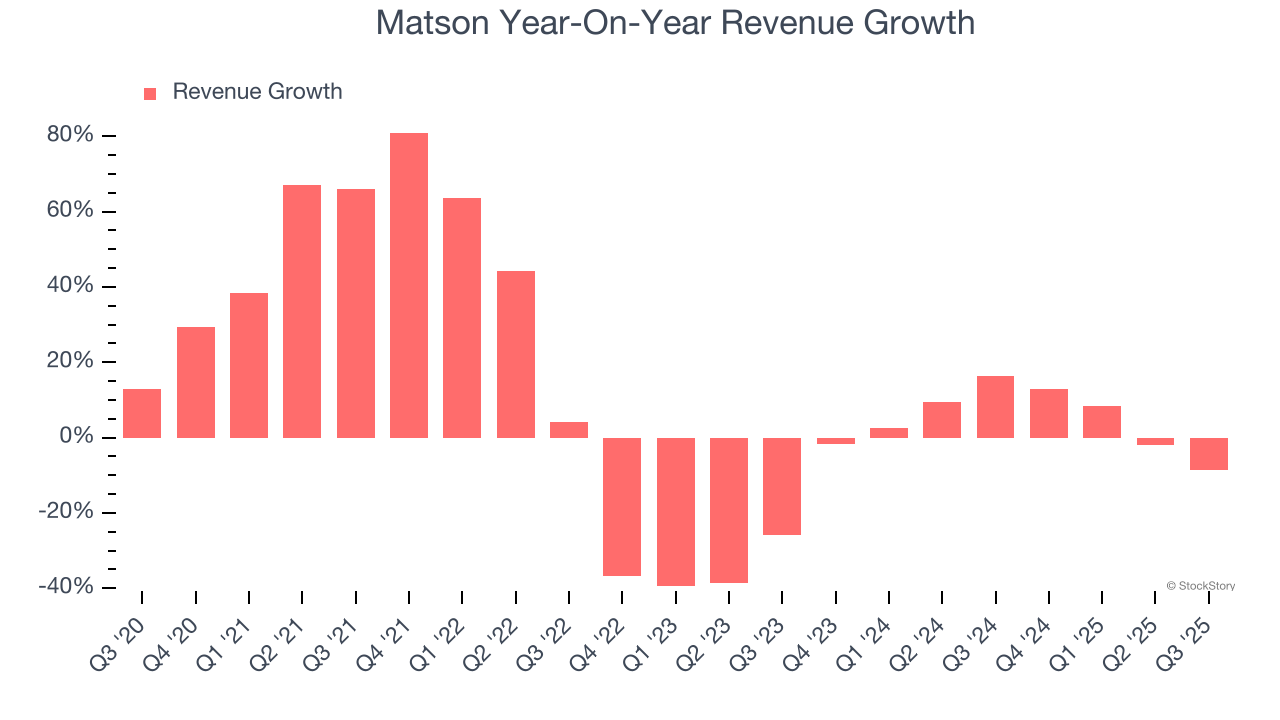

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Matson’s sales grew at a decent 8.8% compounded annual growth rate over the last five years. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Matson’s recent performance shows its demand has slowed as its annualized revenue growth of 4.3% over the last two years was below its five-year trend. We also note many other Marine Transportation businesses have faced declining sales because of cyclical headwinds. While Matson grew slower than we’d like, it did do better than its peers.

This quarter, Matson’s revenue fell by 8.5% year on year to $880.1 million but beat Wall Street’s estimates by 5.1%.

Looking ahead, sell-side analysts expect revenue to decline by 6.9% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will see some demand headwinds.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Operating Margin

Matson has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 21%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Matson’s operating margin decreased by 8.6 percentage points over the last five years. Many Marine Transportation companies also saw their margins fall (along with revenue, as mentioned above) because the cycle turned in the wrong direction. We hope Matson can emerge from this a stronger company, as the silver lining of a downturn is that market share can be won and efficiencies found.

In Q3, Matson generated an operating margin profit margin of 18.3%, down 6.4 percentage points year on year. Conversely, its gross margin actually rose, so we can assume its recent inefficiencies were driven by increased operating expenses like marketing, R&D, and administrative overhead.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

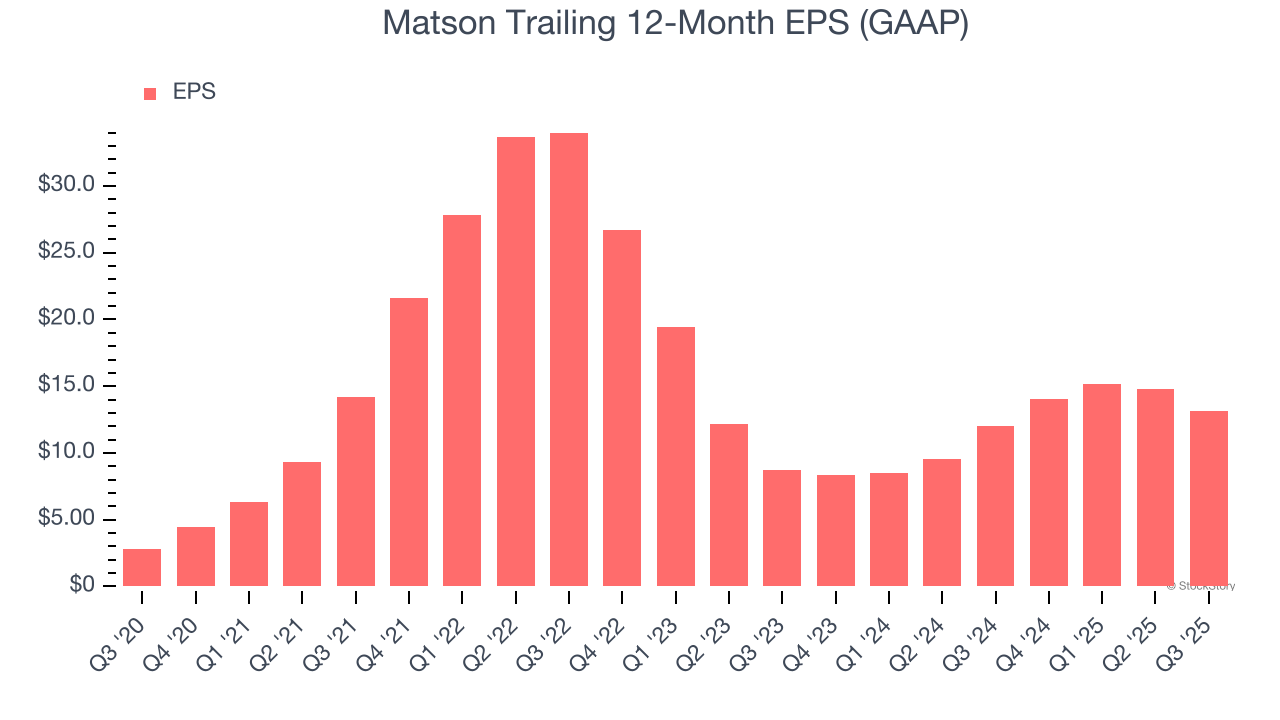

Matson’s EPS grew at an astounding 35.8% compounded annual growth rate over the last five years, higher than its 8.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

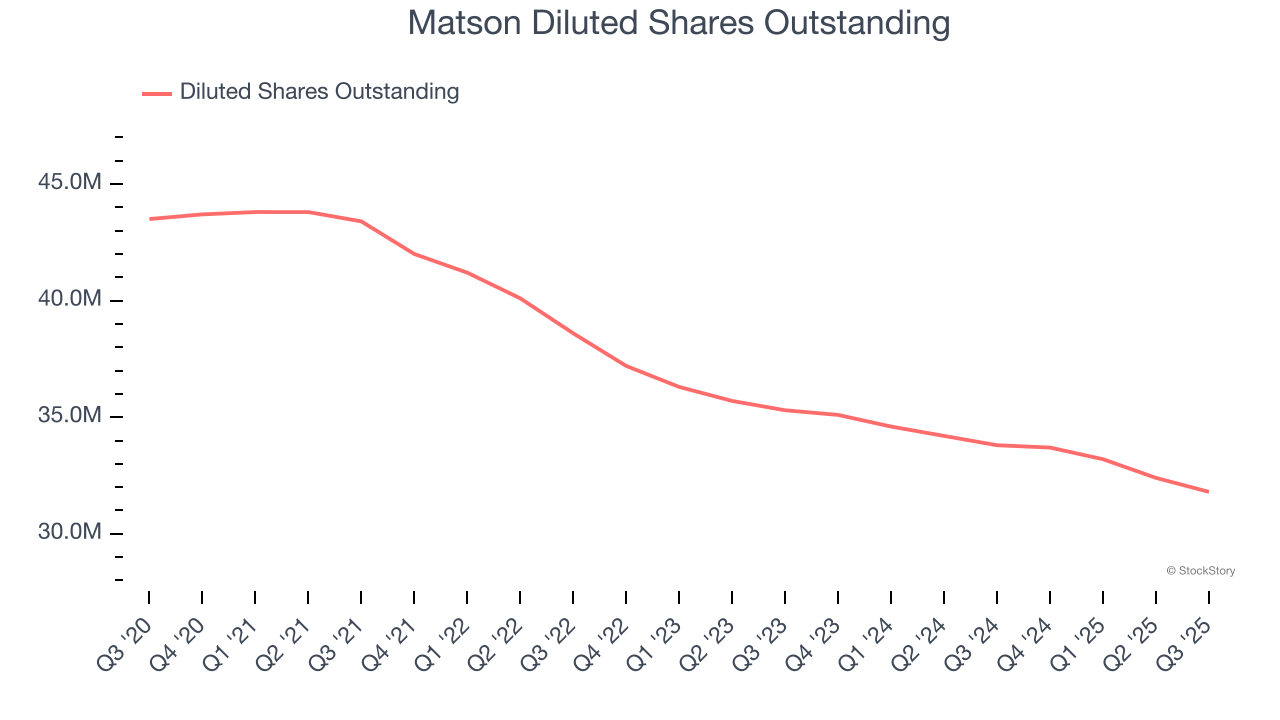

We can take a deeper look into Matson’s earnings to better understand the drivers of its performance. A five-year view shows that Matson has repurchased its stock, shrinking its share count by 26.9%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Matson, its two-year annual EPS growth of 22.9% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q3, Matson reported EPS of $4.24, down from $5.89 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Matson’s full-year EPS of $13.14 to shrink by 22.5%.

Key Takeaways from Matson’s Q3 Results

It was good to see Matson beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock remained flat at $98.66 immediately after reporting.

Matson had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.