Shareholders of ACV Auctions would probably like to forget the past six months even happened. The stock dropped 35% and now trades at $9.59. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy ACV Auctions, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Why Is ACV Auctions Not Exciting?

Even with the cheaper entry price, we don't have much confidence in ACV Auctions. Here are three reasons why ACVA doesn't excite us and a stock we'd rather own.

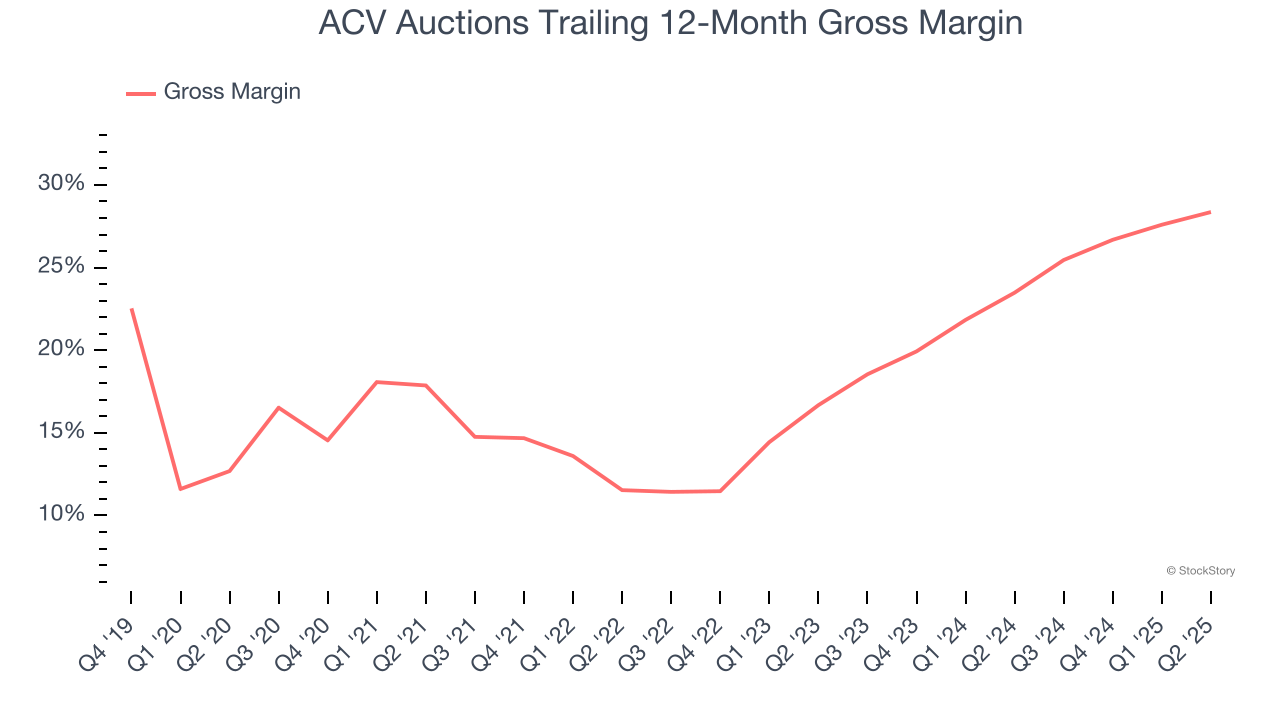

1. Low Gross Margin Reveals Weak Structural Profitability

For online marketplaces like ACV Auctions, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard buyers and sellers, such as identity verification.

ACV Auctions’s unit economics are far below other consumer internet companies, signaling it operates in a competitive market and must pay many third parties a slice of its sales to distribute its products and services. As you can see below, it averaged a 26.2% gross margin over the last two years. Said differently, ACV Auctions had to pay a chunky $73.76 to its service providers for every $100 in revenue.

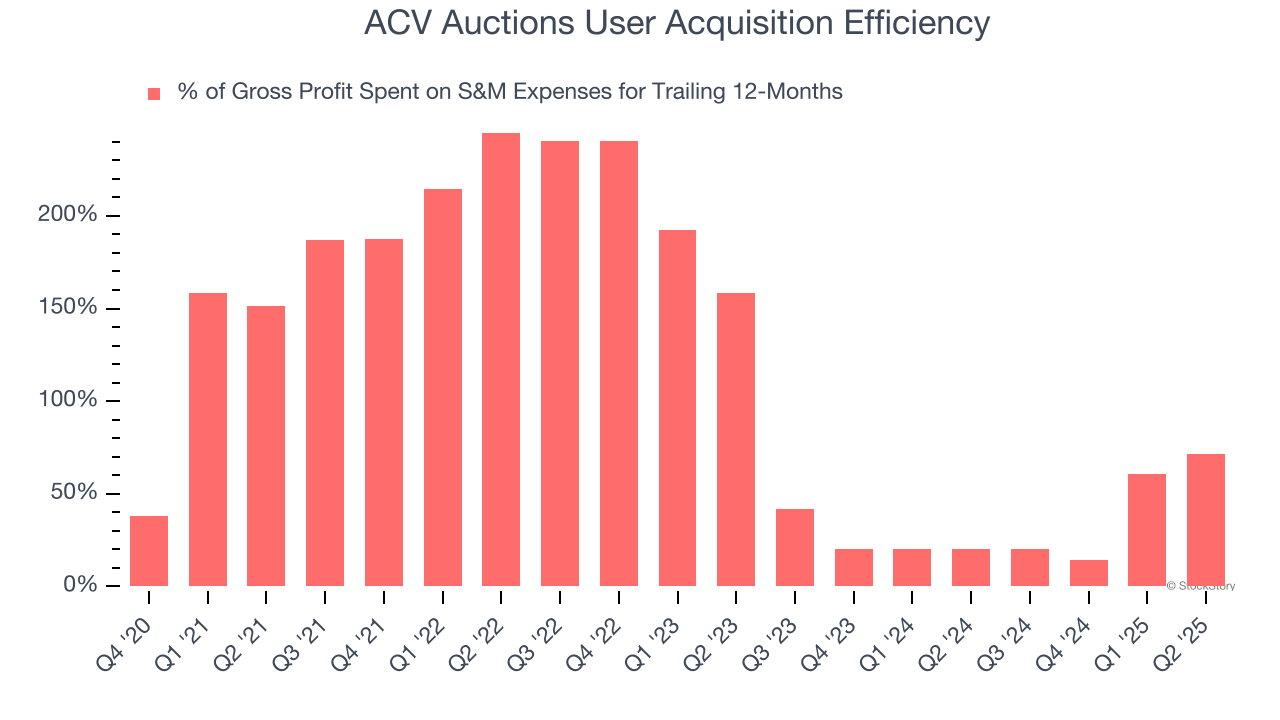

2. Poor Marketing Efficiency Drains Profits

Unlike enterprise software that’s typically sold by dedicated sales teams, consumer internet businesses like ACV Auctions grow from a combination of product virality, paid advertisement, and incentives.

It’s very expensive for ACV Auctions to acquire new users as the company has spent 71.5% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates a highly competitive environment with little differentiation between ACV Auctions and its peers.

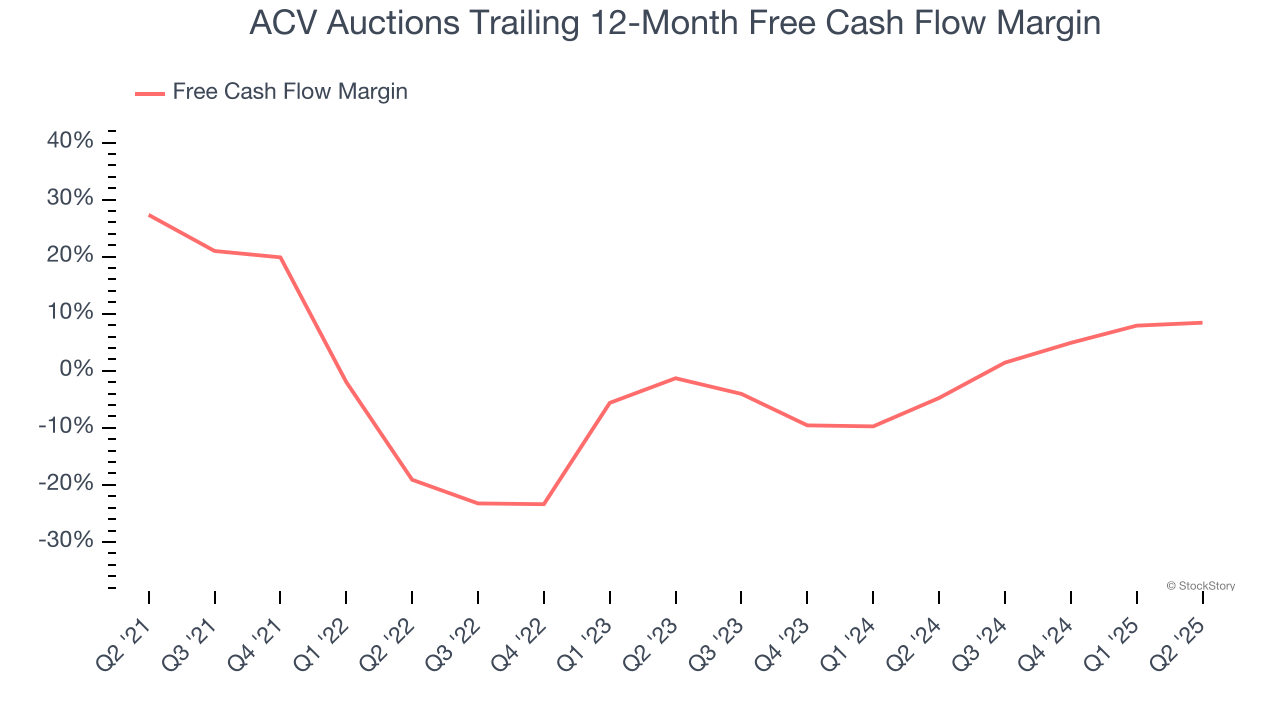

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

ACV Auctions has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.7%, subpar for a consumer internet business.

Final Judgment

ACV Auctions’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 17.2× forward EV/EBITDA (or $9.59 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. Let us point you toward an all-weather company that owns household favorite Taco Bell.

Stocks We Like More Than ACV Auctions

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.