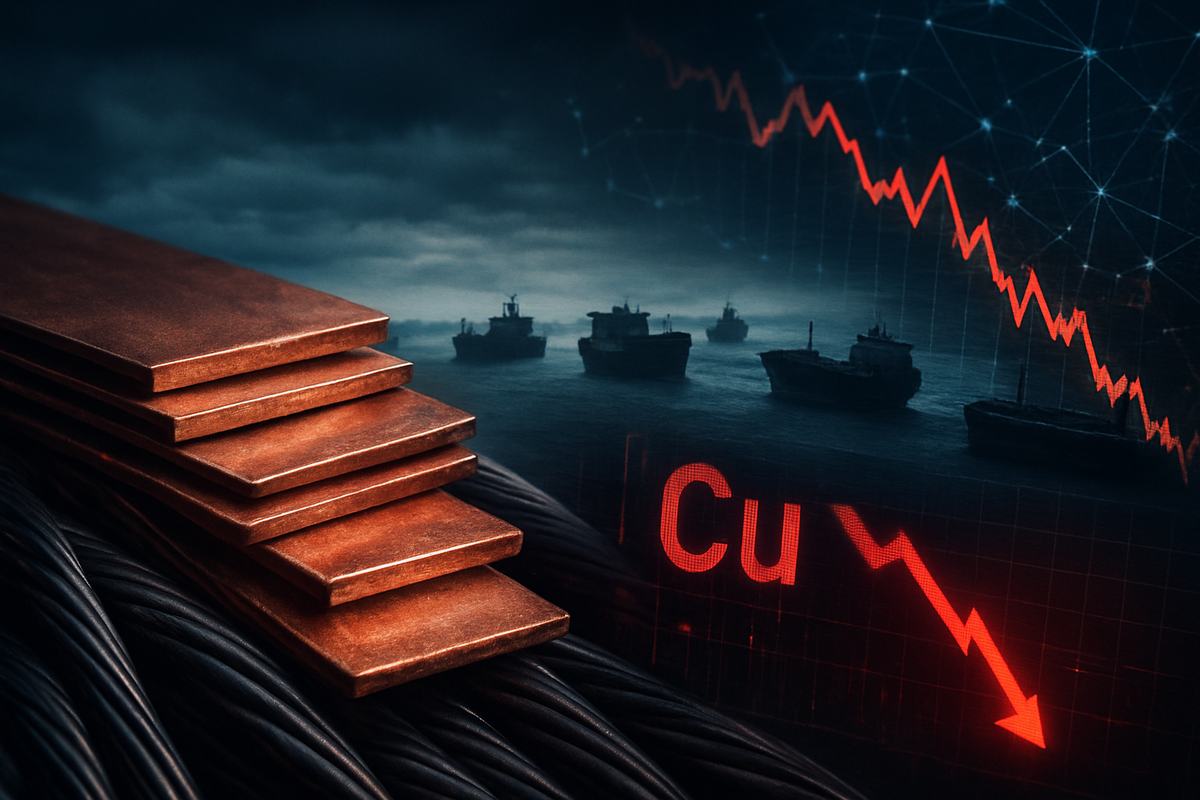

The historic rally in the copper market, which propelled the industrial metal to unprecedented heights earlier this year, has come to a jarring halt. On March 4, 2026, copper prices plummeted in a massive reversal, signaling the end of a speculative frenzy that had gripped global markets since the start of the year. This sudden downturn comes as a "crowded" industrial metals trade collapses under the weight of escalating geopolitical tensions and a tightening global supply chain.

The immediate catalyst for the sell-off is a combination of deteriorating conditions in the Middle East and a technical correction long signaled by institutional heavyweights. As the "Dr. Copper" indicator—often viewed as a bellwether for global economic health—turns bearish, investors are grappling with a market landscape suddenly dominated by war risk premiums, soaring energy costs, and the threat of a mid-year industrial slowdown.

The Peak and the Plunge: A Timeline of Volatility

The path to the current crisis began in late January 2026, when copper reached a record nominal high on the London Metal Exchange (LME) of $14,527.50 per tonne. Driven by massive demand for artificial intelligence infrastructure and a rush by U.S. manufacturers to front-load inventories ahead of anticipated trade policy shifts, the metal seemed unstoppable. However, the tide turned on March 4, 2026, as a "de-grossing" event saw hedge funds and institutional investors flee the sector in unison.

The reversal was triggered by the worsening blockade of the Strait of Hormuz. Following military escalations in late February, Iranian forces effectively halted roughly 20% of the world’s petroleum and liquefied natural gas (LNG) flows. While crude oil prices spiked, industrial metals like copper suffered a "price-shock paradox." The market pivoted from viewing copper as a scarce growth asset to a liability in an environment of "energy-led inflation." By the close of trading on March 4, copper had shed nearly 10% of its peak value, retesting the critical $12,000 support level.

Industry analysts at The Goldman Sachs Group, Inc. (NYSE: GS) had already voiced caution, but the speed of the descent caught many off guard. The investment bank’s research team, which had previously projected a larger correction for mid-2026, noted that the speculative "scarcity premium" evaporated almost overnight as the logistical nightmare in the Persian Gulf shifted the focus from future growth to immediate survival.

Winners and Losers: Mining Giants Under Pressure

The fallout from the March 4 reversal has sent shockwaves through the equities market, particularly for major producers. Mining behemoths like BHP Group (ASX: BHP) and Rio Tinto (ASX: RIO) saw their share prices hammered as part of a broader materials rout. For these companies, the dual threat of lower realized copper prices and surging operational costs—driven by the energy spike—poses a significant threat to mid-year earnings.

Freeport-McMoRan Inc. (NYSE: FCX), one of the world’s largest publicly traded copper producers, also faced heavy selling pressure. While the company benefits from its geographically diverse asset base, the sudden shift in market sentiment from "deficit-fearing" to "demand-destruction" has cooled investor appetite. Similarly, Southern Copper Corporation (NYSE: SCCO) saw its premium valuation contract as the "crowded" long trade in industrial metals unwound.

On the winning side, few have escaped the carnage, though specialized "war-room" advisory firms and short-sellers have profited from the volatility. Some downstream manufacturers that had avoided long-term supply contracts may find relief in lower input costs later this year, provided the global economy avoids a full-scale recession. However, for most in the materials space, the day was defined by a rapid erosion of market capitalization, with Fortescue Ltd (ASX: FMG) and other iron-ore-heavy diversified miners also caught in the 4.2% slide of the ASX 200 Materials Index.

Geopolitics and the Death of the 'Crowded' Trade

The wider significance of this reversal lies in the intersection of energy logistics and metallurgical processing. The blockade of the Strait of Hormuz has disrupted the export of sulfur from major Middle Eastern producers. Sulfur is a critical precursor for sulfuric acid, which is used in the solvent extraction and electrowinning (SX-EW) process responsible for approximately 20% of global refined copper production. This "hidden" supply chain link means that even as demand cools, the cost of production is rising, creating a "stagflationary" squeeze for the mining sector.

Historically, copper rallies have been ended by oversupply, but the 2026 reversal is unique because it is being driven by a liquidation of a "crowded" trade. According to recent fund manager surveys, "Long Commodities" had become one of the most over-allocated positions in the market. When the geopolitical situation shifted, the exit door proved too small for the volume of investors trying to leave simultaneously. This event mirrors the "commodity crunch" of the early 2010s but is amplified by the high-frequency trading and algorithmic models that dominate the 2026 market.

The 4.2% drop in the ASX 200 Materials Index on March 4 serves as a stark reminder of Australia’s sensitivity to global trade flows. The index's decline is the worst single-session performance since the global trade tensions of 2025, underscoring how quickly regional markets can be destabilized by events in the Persian Gulf.

Looking Ahead: The Mid-2026 Correction

What comes next for the red metal depends largely on the duration of the Hormuz blockade and the realization of Goldman Sachs' mid-2026 forecast. The bank continues to predict that copper will settle toward the $11,000 to $11,200 range by the end of the year. They argue that the official implementation of new U.S. refined copper tariffs, expected in the second quarter, will finally clear the "uncertainty premium" and allow the market to return to fundamentals.

In the short term, the market will likely see extreme volatility as traders weigh the risks of a global manufacturing slowdown against the reality of long-term supply deficits. Companies may be forced to pivot their strategies, focusing on "near-shoring" supply chains and securing non-Middle Eastern sources of energy and chemical inputs. The emergence of a "two-tier" copper market—distinguishing between "green" copper produced with renewable energy and traditional copper—could also accelerate as ESG-focused investors seek shelter from the carbon-heavy energy shocks currently rattling the Middle East.

Navigating a Post-Peak Market

The events of March 4, 2026, mark a definitive turning point in the post-pandemic commodity cycle. The "supercycle" narrative has been challenged by the reality of geopolitical fragility and the dangers of overcrowded speculative positions. Key takeaways for investors include the renewed importance of supply chain resilience and the need to watch energy price correlations as a leading indicator for industrial metal movement.

Moving forward, the market will be hyper-focused on the resolution of the Hormuz blockade and the subsequent reaction of central banks. If energy prices remain elevated, the resulting "inflation tax" could lead to a more prolonged slump in copper demand than currently anticipated. Investors should keep a close eye on LME inventory levels and the upcoming Q2 earnings calls from major miners for clues on how they are navigating this high-cost, high-risk environment. For now, the "Dr. Copper" diagnosis is one of caution and consolidation.

This content is intended for informational purposes only and is not financial advice.