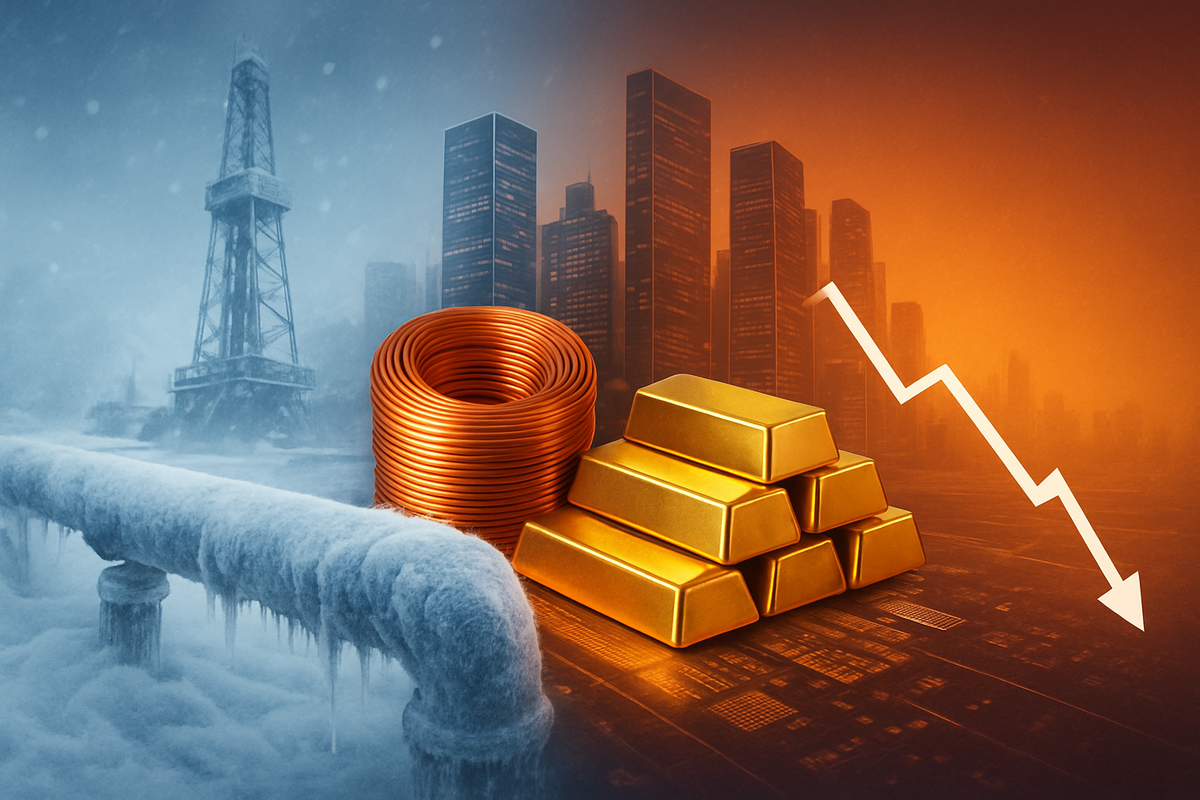

The global commodity market is currently navigating a period of intense volatility as a series of short-term supply shocks clash with a looming long-term surplus. According to the World Bank’s latest Commodity Markets Outlook, the start of 2026 has been defined by a sharp reversal of the downward trend seen throughout 2025. The energy price index surged by 12% in January alone, while the metals index jumped 9.3%, creating immediate inflationary pressure that has caught many market participants off guard.

Despite these dramatic spikes, the World Bank’s central thesis remains unchanged: by the end of 2026, global commodity prices are expected to hit their lowest levels in six years. This projection points toward a "fourth consecutive year of decline" driven by a massive oversupply of crude oil and a broader slowdown in global manufacturing demand. For investors and policymakers, the current price surges represent a "last gasp" of volatility before a significant deflationary period settles in for the remainder of the decade.

A Perfect Storm: Natural Gas Freezes and Metal Scarcity

The 12% surge in the energy price index was largely driven by a historic disruption in the North American natural gas market. In late January 2026, "Winter Storm Fern"—a record-breaking Arctic weather system—triggered widespread "wellhead freeze-offs," knocking approximately 15% of total U.S. natural gas production offline. This occurred just as heating demand reached a generational peak, leading to the largest weekly storage withdrawal in recorded history. While the immediate crisis has subsided as of early March, the price ripples continue to affect global liquefied natural gas (LNG) markets.

Simultaneously, the 9.3% jump in the metals index was fueled by a combination of geopolitical instability and aggressive industrial policy. The U.S. government’s launch of "Project Vault," a $12 billion strategic initiative to stockpile critical minerals, significantly tightened the spot market for copper and lithium. Further complicating the supply side, renewed geopolitical tensions over resource rights in Greenland led to a flight to safety, pushing gold above the $5,000 per ounce mark and dragging industrial metals like aluminum and tin higher in its wake.

Winners and Losers in the 2026 Price Swing

The sudden spike in natural gas prices has been a boon for major North American producers. Companies like EQT Corporation (NYSE: EQT) and Cheniere Energy (NYSE: LNG) have seen significant margin expansion as they capitalized on record spot prices during the January freeze. These firms, which had been bracing for a low-price environment throughout 2026, now find themselves with unexpected cash windfalls that may be used for accelerated debt reduction or shareholder returns.

Conversely, the heavy industrial sector and the transportation industry are feeling the burn. For airlines like Delta Air Lines, Inc. (NYSE: DAL) and American Airlines Group Inc. (NASDAQ: AAL), the uptick in crude oil prices—which rose 4.6% in sympathy with the gas spike—threatens to erode the fuel-cost savings they had projected for the 2026 fiscal year. In the metals space, mining giants such as Freeport-McMoRan (NYSE: FCX) and Rio Tinto (NYSE: RIO) are benefiting from the "Project Vault" demand, but downstream manufacturers, particularly electric vehicle makers, are facing renewed supply chain headwinds.

Analyzing the Shift: The "New Era" of Commodity Disconnection

The World Bank report highlights a growing "disconnection" between different commodity classes. Historically, energy, metals, and food prices tended to move in relative synchronization. However, 2026 is marking a pivot toward a more fragmented market. While oil prices are being weighed down by a massive global glut—forecast to reach 65% above 2020 levels by year-end—metals are finding a structural floor due to the relentless demand from data centers and the Generative AI revolution.

This shift has profound regulatory and policy implications. Central banks, which had been hoping for a smooth glide path toward 2% inflation targets, must now contend with "input-driven" volatility. While the World Bank expects food prices to decline by 7% through the rest of the year, the persistent high cost of copper and other transition minerals could keep the "green inflation" (greenflation) narrative alive, potentially complicating the pace of interest rate cuts.

The Long Road to a Six-Year Low

Looking ahead to the remainder of 2026, the primary narrative will be the "Global Oil Glut." The World Bank forecasts that Brent crude will average just $60 per barrel by the end of the year, down from a $68 average in 2025. This downward pressure is expected to be the primary catalyst for the commodity index reaching its six-year nadir. The rapid adoption of electric vehicles and hybrid technology, coupled with stagnant demand from major economies like China, is creating a "structural surplus" that even OPEC+ may struggle to manage.

Strategic pivots will be required for companies tied to the fossil fuel economy. We are likely to see a continued shift toward "efficiency over expansion" among the supermajors like Exxon Mobil Corporation (NYSE: XOM) and Chevron Corporation (NYSE: CVX). Meanwhile, the market opportunities will likely shift toward "recycled" commodities and midstream infrastructure that can handle the increased volatility of the transition period.

Market Outlook: Navigating the 2026 Respite

The key takeaway from the World Bank's recent report is that the current price spikes are an anomaly within a broader deflationary trend. For the global economy, this "commodity respite" offers a window of opportunity to implement fiscal reforms and stabilize energy security. However, the World Bank warns that this period of lower prices may be temporary if investment in new mineral extraction continues to lag behind the needs of the energy transition.

Investors should watch the crude oil surplus and U.S. natural gas storage levels closely in the coming months. If the projected oil glut materializes as expected, it could provide the final disinflationary push needed to solidify a low-interest-rate environment globally. However, as the January energy surge demonstrated, the market remains highly vulnerable to "black swan" weather events and geopolitical shifts that can instantly derail long-term forecasts.

This content is intended for informational purposes only and is not financial advice