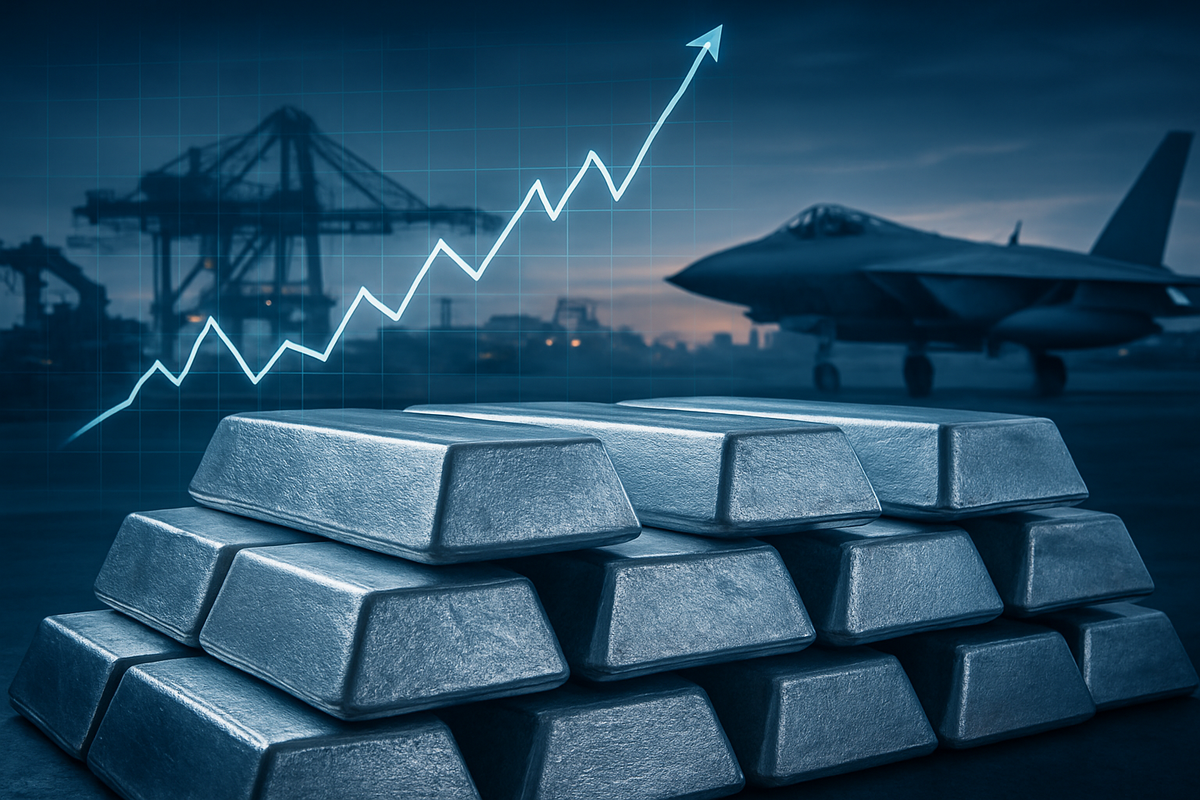

The global aluminum market has reached a critical fever pitch as prices on the London Metal Exchange (LME) surged to a four-year high this month, touching levels not seen since the height of the post-pandemic supply crunch in early 2022. As of February 27, 2026, benchmark aluminum prices are hovering near $3,300 per metric ton, driven by a "perfect storm" of structural supply deficits, aggressive financial speculation, and a seismic shift in Western industrial policy. While the market has seen a slight technical correction in the final week of February as traders lock in profits, the fundamental floor for the metal has shifted significantly higher, signaling a new era of "structural scarcity" for one of the world's most essential industrial commodities.

This price escalation is no longer merely a byproduct of cyclical demand but is increasingly fueled by the twin engines of "reindustrialization" and "remilitarization." As Western nations scramble to decouple supply chains from strategic rivals and bolster defense capabilities amid heightened geopolitical tensions, the demand for high-grade aluminum—essential for everything from fighter jets to power grids—has outpaced the global capacity to produce it. With physical inventories in U.S. warehouses dropping to their lowest levels in years, the market has entered a state of chronic backwardation, where immediate delivery of the metal commands a significant premium over future contracts.

The Path to $3,300: A Narrative of Scarcity

The rally that culminated in February’s four-year peak began in late 2024 and accelerated throughout 2025. The primary catalyst was the hardening of China’s 45-million-ton annual production cap, which removed the global market's traditional "safety valve." For decades, China, which produces roughly 60% of the world's aluminum, could be relied upon to flood the market when prices rose. However, under strict environmental mandates and power-rationing policies, the Aluminum Corporation of China (HKG: 2600 / SHA: 601600), also known as Chalco, and its domestic peers have hit a hard ceiling. This left the global market vulnerable to any sudden demand spikes or supply disruptions.

Throughout 2025, these disruptions became frequent. Geopolitical volatility in the Middle East threatened shipping lanes in the Strait of Hormuz, a critical artery for nearly 7 million tons of annual aluminum exports. Simultaneously, the total phase-out of Russian aluminum from European markets, finalized in early 2026, forced a massive and costly reshuffle of trade flows. By the time the LME benchmark breached $3,100 in January 2026, institutional investors and hedge funds began pouring capital into the metal, viewing it as a "high-conviction" bet on the West’s industrial revival and an effective hedge against persistent inflationary pressures.

The reaction from the manufacturing sector has been one of controlled alarm. Aerospace and automotive giants have moved to secure multi-year supply agreements, often at prices well above the LME spot rate, to avoid production halts. In the U.S. Midwest, the physical premium—the cost to actually get aluminum delivered to a factory—reached record highs this month, effectively pushing the "all-in" price for domestic manufacturers toward $5,000 per metric ton when including the 50% import tariffs implemented in June 2025.

Industry Leaders and the Changing Competitive Landscape

In this high-price environment, established producers with low-cost power assets and domestic supply chains are emerging as the clear victors. Alcoa (NYSE: AA) has seen its financial fortunes dramatically reversed. After years of navigating razor-thin margins, the company reported a massive surge in net income for 2025, reaching $1.17 billion. Alcoa’s strategy of restarting curtailed capacity in Spain and Brazil, combined with its investment in "ELYSIS" inert-anode technology, has positioned it as a preferred supplier for Western firms seeking "green" and "conflict-free" aluminum. However, the company continues to face headwinds from rising maintenance costs and a tightening labor market in the U.S.

On the other side of the globe, the Aluminum Corporation of China (HKG: 2600 / SHA: 601600) has pivotally shifted its strategy. With domestic growth capped, Chalco has moved aggressively into Indonesia, investing billions in massive bauxite-to-smelter projects in Kalimantan to bypass China's internal production limits. While Chalco remains a powerhouse, its reliance on coal-fired power for its primary smelting operations makes it increasingly vulnerable to the European Union’s Carbon Border Adjustment Mechanism (CBAM), which reached full implementation in early 2026. This regulatory shift has effectively created a two-tiered market: high-priced "green" aluminum for the West and lower-cost, high-carbon aluminum for the rest of the world.

The "losers" in this scenario are the downstream manufacturers who lack the pricing power to pass on these costs. Small-to-medium-sized automotive component makers and construction firms are finding their margins evaporated by the double blow of high metal prices and record-high electricity costs. Furthermore, a new and unexpected competitor for energy has emerged: AI data centers. In many regions, aluminum smelters are finding themselves outbid for long-term power contracts by technology firms willing to pay a massive premium for the 24/7 electricity required to run AI clusters, leading to further curtailments of primary smelting capacity in the West.

The Strategic Metal: Defense and the Green Transition

The wider significance of this price surge lies in the reclassification of aluminum as a strategic "national security" metal rather than a simple commodity. The remilitarization of the West has become a primary driver of demand that is essentially price-inelastic. NATO’s commitment to increasing defense spending to 3.5% of GDP has funneled billions into aircraft, missile systems, and armored vehicles—all of which are aluminum-intensive. An F-35 fighter jet, for instance, requires over 6,500 kilograms of specialized aluminum alloys, and as production lines for these platforms scale up, the "defense drain" on high-purity aluminum stocks is becoming a permanent fixture of the market.

Simultaneously, the reindustrialization of the United States and Europe is placing unprecedented pressure on supply. The push to build domestic solar supply chains, modernize the aging electrical grid, and transition to electric vehicles (EVs) requires vast amounts of aluminum for frames, wiring, and battery housings. This "Green Demand" is colliding with the reality of a shrinking energy footprint for heavy industry. The paradox of the 2026 market is that the very transition to a low-carbon economy requires a metal whose production is incredibly energy-intensive, creating a feedback loop that keeps prices elevated.

Historically, such price spikes would trigger a wave of new smelting projects. However, the current environment is different from the 2008 or 2011 peaks. The "reindustrialization" of the West is happening behind high tariff walls, such as the U.S. Section 232 duties. These policies protect domestic producers but also ensure that the U.S. and European markets remain "islands" of high prices, detached from the lower global benchmarks. This policy-driven fragmentation of the market suggests that the era of cheap, globally fungible aluminum may be over.

Looking Ahead: The Pivot to Secondary Aluminum

In the short term, the market is likely to see further volatility as the "slight correction" observed in late February plays out. Technical indicators suggest that the $3,300 level may act as a ceiling for the next few months as buyers wait for the impact of Indonesian supply to hit the market. However, any further escalation in geopolitical tensions or a faster-than-expected deployment of "Industrial Accelerator" funds in Europe could easily see aluminum test the $3,500 mark by the second half of 2026.

Long-term, the industry is forced to pivot toward "secondary" or recycled aluminum. Because recycling aluminum requires only 5% of the energy needed for primary smelting, it has become the ultimate strategic hedge for companies like Alcoa (NYSE: AA). We expect to see a surge in "urban mining" investments and tighter regulations on scrap metal exports as Western governments move to keep their secondary aluminum within their borders. This shift will likely lead to a boom in advanced sorting and recycling technologies, creating new market opportunities for specialty engineering firms.

Summary and Investor Outlook

The aluminum market’s climb to a four-year high in February 2026 marks a structural transition driven by the necessities of a more fragmented and militarized world. The convergence of China's production caps, the energy needs of the AI revolution, and the West’s urgent reindustrialization has created a deficit that cannot be easily filled by traditional capacity expansions. While the current price of $3,326 per metric ton reflects a period of intense heat, the fundamental drivers suggest that the "new normal" for aluminum is significantly higher than the averages seen in the previous decade.

For investors, the coming months require a focus on vertical integration and energy security. Companies that control their own bauxite supply and have secured low-carbon, long-term power contracts will continue to outperform. Watch for Alcoa's (NYSE: AA) progress on its carbon-free smelting tech and Chalco's (HKG: 2600) ability to navigate Indonesian politics and EU carbon taxes. As aluminum evolves from a common base metal into a strategic asset, its price will remain a key barometer for the health of the global industrial and defense sectors.

This content is intended for informational purposes only and is not financial advice