Medtronic’s (MDT) diabetes care subsidiary, MiniMed Group, has officially kicked off its IPO roadshow in a bid to list as an independent company on the Nasdaq. About 28 million shares of the common stock will be offered to the public at an expected price range of $25 to $28 per share. The company will trade under the ticker MMED.

Medtronic will still hold somewhere between 89% and 90% of the company post-IPO. The funds generated through the IPO will be utilized to strengthen the balance sheet as well as pay for some general expenses. More importantly for investors, the public offering will allow investors to value Medtronic’s diabetes portfolio and the rest of the business separately rather than as a single entity. This could potentially unlock a better valuation in the future. While the IPO doesn’t drastically change anything for the company in the short term, it is part of a multi-year transformation that will eventually help the company increase its focus on the higher-margin parts of the business.

About Medtronic Stock

Medtronic is a global medical technology company that develops and manufactures device-based therapies for over 70 different health conditions. The company’s diabetes care business, MiniMed Group, makes continuous glucose monitors, insulin pumps, and other diabetes management devices.

MDT’s one-year performance of 4.6% has underperformed the broader market. However, the trend has been witnessed across the whole healthcare sector, with the Vanguard Health Care Index Fund ETF (VHT) delivering only 7.99% returns during the same period. Medtronic also offers a dividend yield of 2.88%, which makes it a suitable choice for income investors who happily take the performance trade-off for the dividend cushion.

Medtronic has raised its dividend for 48 consecutive years now. The stock still trades at a discount to the Healthcare sector, which is why dividend investors love to accumulate it. Currently, the stock’s forward P/E ratio of 23.29x offers a moderate discount to the five-year average P/E of 25.18x. This valuation is justified by a slow but stable growth, with the company expected to grow its profits by 7.95% in 2027, 7.74% in 2028, and 8.18% in 2029. A payout ratio of 50% shows the company should have no issues continuing to pay dividends while capitalizing on any growth opportunities.

The firm is expected to pay out a dividend of $2.87 in 2026, a meager 1.4% growth. 2027 is when the higher dividend kicks in, with a consensus 7.7% growth taking the 2027 dividend to $3.09 for the fiscal year. Considering the stock is 8% down from its 52-week high, investors might want to lock in a 2027 forward dividend yield of 3.15% today.

As far as MiniMed is concerned, the firm generated about 8% of the company’s revenue in FY2025. If the IPO is priced at $25, it would value the company at around 6% of Medtronic’s market cap. Considering MiniMed is growing faster than the parent company at the moment, the IPO seems fairly valued, especially if the separation unlocks better valuation in the future.

Medtronic Beats Wall Street Earnings Estimates

Medtronic reported its Q3 earnings on Feb. 17, comfortably beating the consensus estimates. The EPS of $1.36 per share narrowly beat expectations of $1.35, while the revenue of $9.02 billion also surpassed the estimated $8.99 billion. The company’s Cardiac Ablation Solutions business was the fastest-growing segment, registering over 80% YoY growth. For fiscal year 2026, the healthcare company expects an EPS between $5.62 and $5.66.

When asked about how the company can deliver growth in 2027, management highlighted improving gross margins and operating margin leverage. There was no significant comment from the management regarding the MiniMed IPO, but that could change pretty soon as the March 5 date nears. That’s when the IPO subscription period officially begins.

What Are Analysts Saying About MDT Stock?

Wells Fargo maintained its “Buy” rating on the MDT stock on Feb. 19. One day before this, Truist lowered the stock’s price target from $107 to $103.

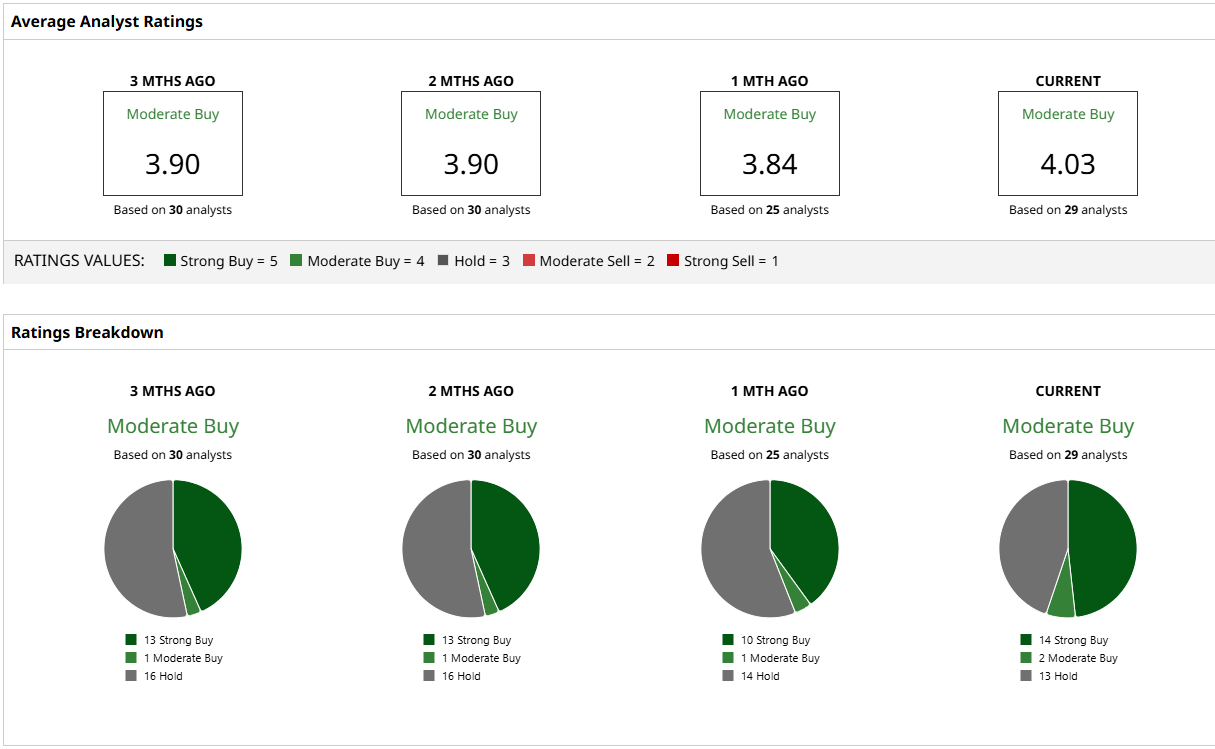

Despite 14 “Strong Buy” ratings from Wall Street analysts, the company also has 13 “Hold” ratings, which suggests analysts are divided about the stock’s prospects. Once the MiniMed Group goes public, MDT might be able to focus on its high-margin business, thus potentially improving analyst sentiment. Until then, Medtronic remains a consensus “Moderate Buy.”

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Micron Technology Short-Put Plays Have Huge Yields - Attractive to Value Investors

- Sandisk Stock Hype Could ‘Vanish in a Single Earnings Call’ According to Citron Research. Is It Time to Ditch SNDK Here?

- Up 183% Over the Past Year, Does Teradyne Stock Have More Room to Run?

- Dear Broadcom Stock Fans, Mark Your Calendars for March 4