Retail investors are watching warehouse and club-store names closely as shoppers hunt for value amid higher prices and growing geopolitical volatility. While United States retail sales cooled into late 2025, bargain-seeking consumers have kept membership-based formats resilient. One company investors should circle on their calendars is Costco Wholesale (COST). Its fiscal Q2 results, due March 5, 2026, will test whether Costco’s steady traffic, membership growth, and new AI-driven efficiencies can sustain margins and justify a premium valuation.

With comps and household memberships showing early strength and analysts broadly positive, this earnings report may confirm why investors have bid COST higher in early 2026 or expose limits to further upside for cautious investors right now.

Costco Deploys AI Tools in Pharmacy and Fuel Operations

Costco has quietly been ramping up technology in its warehouses. It rolled out a Costco Digital Wallet, door scanners, and pre-scan baskets that have significantly sped up checkouts. New AI-driven tools are being deployed behind the scenes; for example, the pharmacy inventory system now auto-reorders drugs and compares prices, boosting fill rates and margins. Management has even begun “gradually introducing AI” in fuel station operations.

On the digital retail front, Costco upgraded its website with improved product pages, search, and AI-powered personalization recommending products based on members’ past searches. It also added a “Buy Now, Pay Later” option for big items. All this tech is aimed at improving efficiency and member loyalty, something Costco has highlighted to analysts. Indeed, improved checkout speeds and digital services help offset Costco’s extended warehouse hours, preserving its lean cost structure.

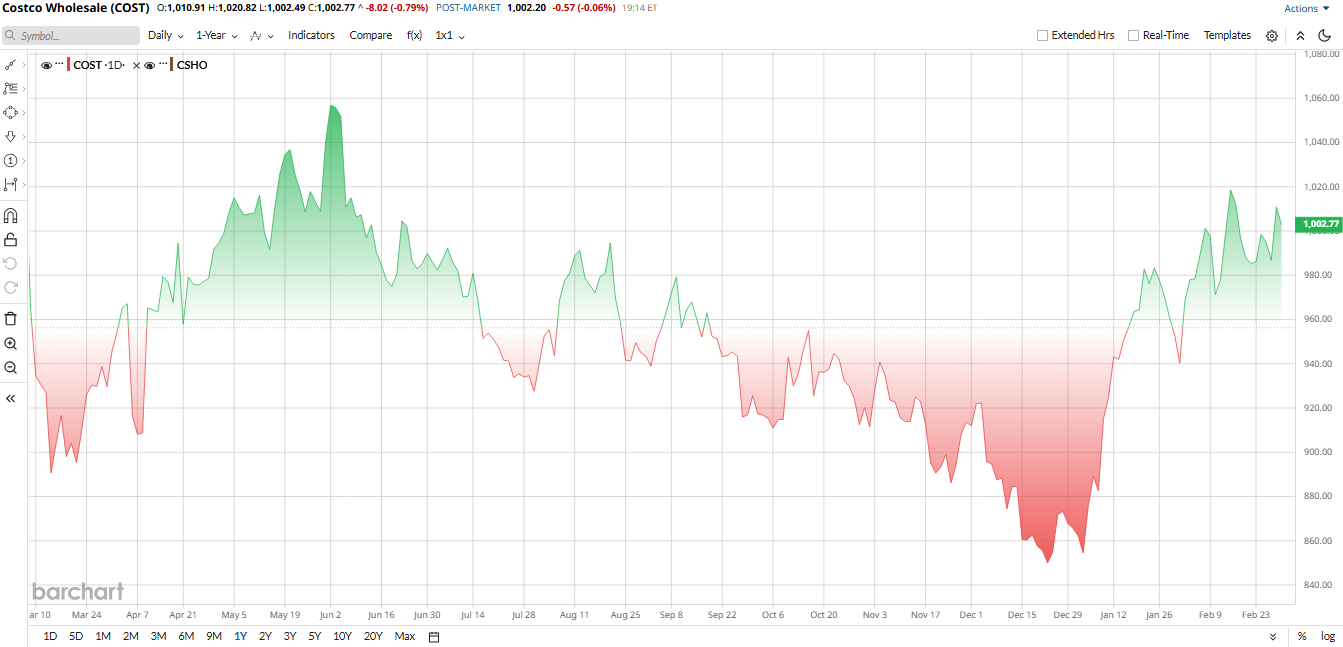

COST stock is surging in early 2026. After a soft end to 2025, shares are up roughly 17% year-to-date (YTD). That rally reflects strong early-year sales and a broader retail bounce. Analysts credit Costco’s growth to new stores, digital expansion, and a defensive business model for the gains. In short, investors are willing to pay up for its consistent performance even though higher interest rates and an expensive valuation argue for caution.

Despite the momentum, Costco trades richly by normal measures. Its price-to-earnings (P/E) ratio is significantly higher than the sector median, indicating the stock is expensive compared to its peers. Furthermore, the price-to-book ratio is over 432% higher than the sector, reflecting a very expensive stock.

Upcoming Earnings Preview

Costco Wholesale Corporation is set to report fiscal second-quarter results after the market closes on Thursday, March 5, and expectations are building. Wall Street is looking for revenue of about $69.2 billion, up roughly 9% year-over-year (YoY), and earnings per share of $4.54, implying low double-digit growth.

Investors will be zeroed in on comparable-store sales, membership trends, and margins. In January, Costco posted a 9% jump in net sales over four weeks, with comps rising more than 7%, suggesting solid momentum heading into the quarter. Management has also highlighted a 5% increase in household memberships in the prior quarter, along with steady upgrades to higher-tier plans.

Digital sales growth, fuel trends, and fresh food demand will also be key. Historically, Costco has a track record of topping earnings estimates, even in tougher consumer environments. If membership growth and pricing discipline hold, this quarter could extend that pattern.

Analysts’ Views and Price Targets

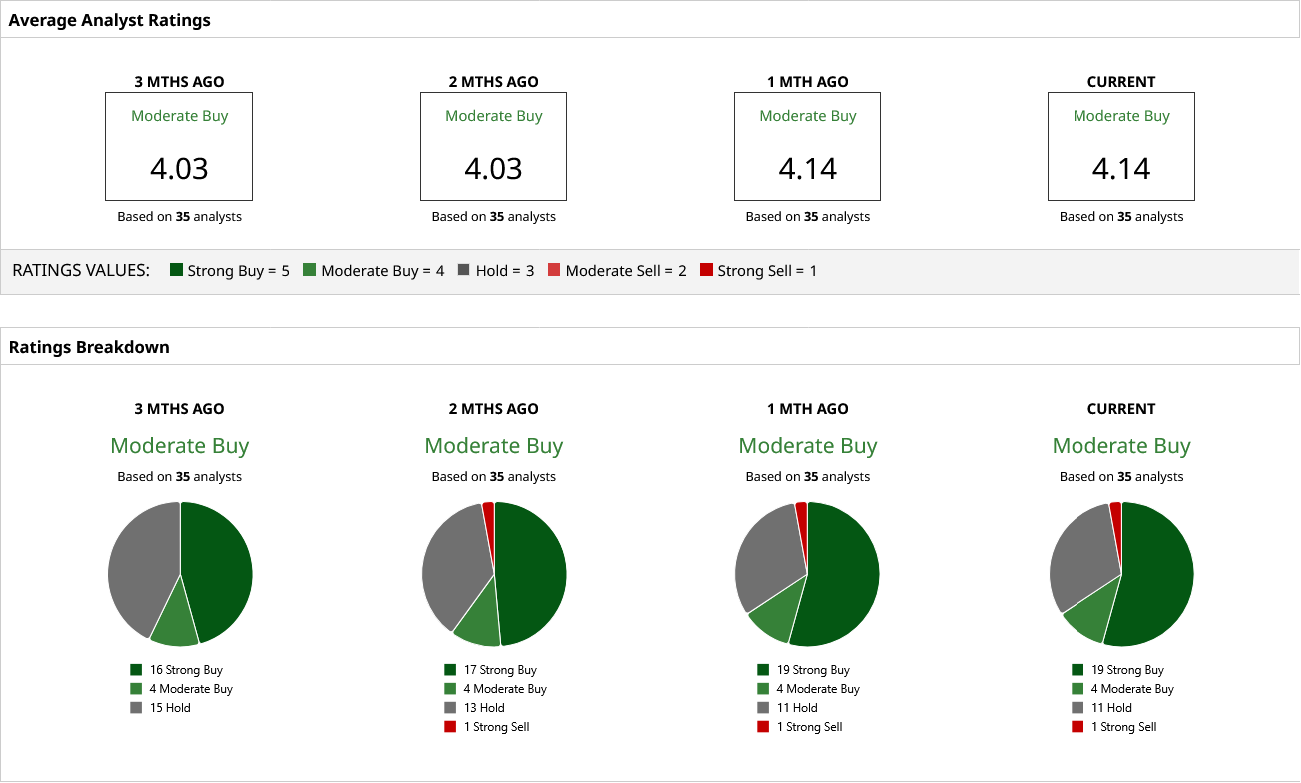

Costco has generally a positive rating on Wall Street and was rated a consensus “Moderate Buy.” Analysts project the price to average $1,064.9 in the coming year, approximately 6% higher than the current price.

Bank of America is just beginning to cover Costco and has rated it a “Buy” with a price target of $1,185. The firm says that Costco appeals to the higher-income customers and gives good value.

Similarly, Morgan Stanley maintained an “Overweight” rating and a $1225 target, citing growth in online sales and fees. Goldman Sachs has a bullish $1,133 target, citing strong sales of fresh fruit. Generally, analysts affirm that Costco boasts strong earnings and a stable customer base, although the stock is not cheap.

In the short term, analysts will examine the March 5 earnings report to assess any surprises regarding renewals, sales comparisons, and costs. The investors would like to know whether Costco will be able to exceed expectations once again and earn enough to warrant its high price, or will the financial performance merely substantiate the positive attitude already imbued in the stock?

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart