One can gauge the level of uncertainty in the market when a man who made his first fortune by winning at blackjack is advocating for safe stocks. Bill Gross, the billionaire founder of Pacific Investment Management Co. (PIMCO), and the one who made active trading in bonds mainstream, is “staying away” from the AI names that have defined market returns in recent years.

Sounding cautious about the AI trade, Gross remarked, "Maybe it’s not a single elimination game but it feels like it. I'm staying away." Instead, the “Bond King” is finding value in names that have a long track record of navigating several market cycles, operate stable businesses, and have a history of paying dividends.

Which income stocks are they? Let's take a closer look.

Income Stock #1: Verizon (VZ)

Founded in 2000, Verizon (VZ) is one of the largest telecommunications companies in the world. It provides a wide range of communications and technology services to consumers, businesses, and governmental entities across the United States and internationally. Its core operations include wireless and fixed wireline voice and data services, broadband and fiber-optic broadband, wireless equipment and related devices, and business solutions such as IoT connectivity, managed networks, and security services.

Valued at a market capitalization of $211 billion, VZ stock is up 22% on a year-to-date (YTD) basis. The stock offers a dividend yield of 5.5%, which is much higher than the sector median of 1.55%. Notably, the company is on track to be a “Dividend Aristocrat,” having raised dividends consecutively over the past 21 years.

The results for the most recent quarter saw Verizon reporting a beat on both revenue and earnings. Revenue for the quarter came in at $36.4 billion, up 2% from the previous year. However, earnings dropped marginally to $1.09 per share from $1.10 per share in the year-ago period.

Yet, the company continues to generate healthy cash flow from operations as net cash from operating activities for 2025 came in at $37.1 billion, up from $36.9 billion in the previous year. Overall, Verizon closed 2025 with a cash balance of about $19 billion.

Meanwhile, VZ stock is trading at a forward price-to-earnings (P/E) ratio and price-to-cash flow (P/CF) ratio of 10.1 times and 5.5 times, respectively, lower than the sector medians of 13.8 times and 8.1 times.

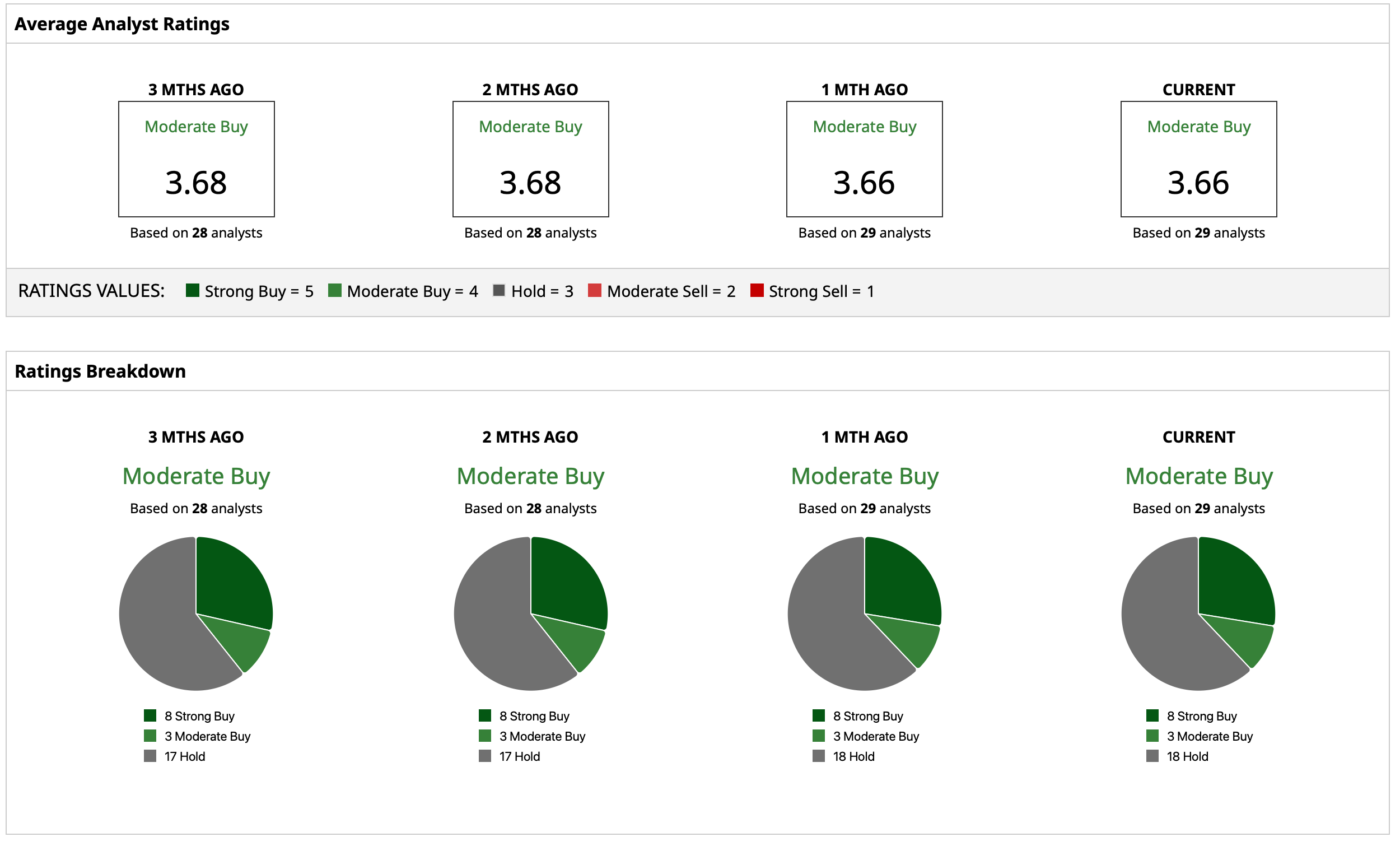

Overall, analysts rate VZ stock as a consensus “Moderate Buy." The mean target price of $49.72 is in-line with current levels, while the high target price of $71 indicates potential upside of about 43%. Out of 29 analysts covering the stock, eight have a “Strong Buy” rating, three have a “Moderate Buy” rating, and 18 have a “Hold” rating.

Income Stock #2: AT&T (T)

The second name on this list is Verizon's rival, AT&T (T). Originally founded way back in 1885, AT&T operates as a large integrated telecommunications and technology company providing wireless and wireline communications services, broadband internet, video services, managed network services, and advertising and media interfaces.

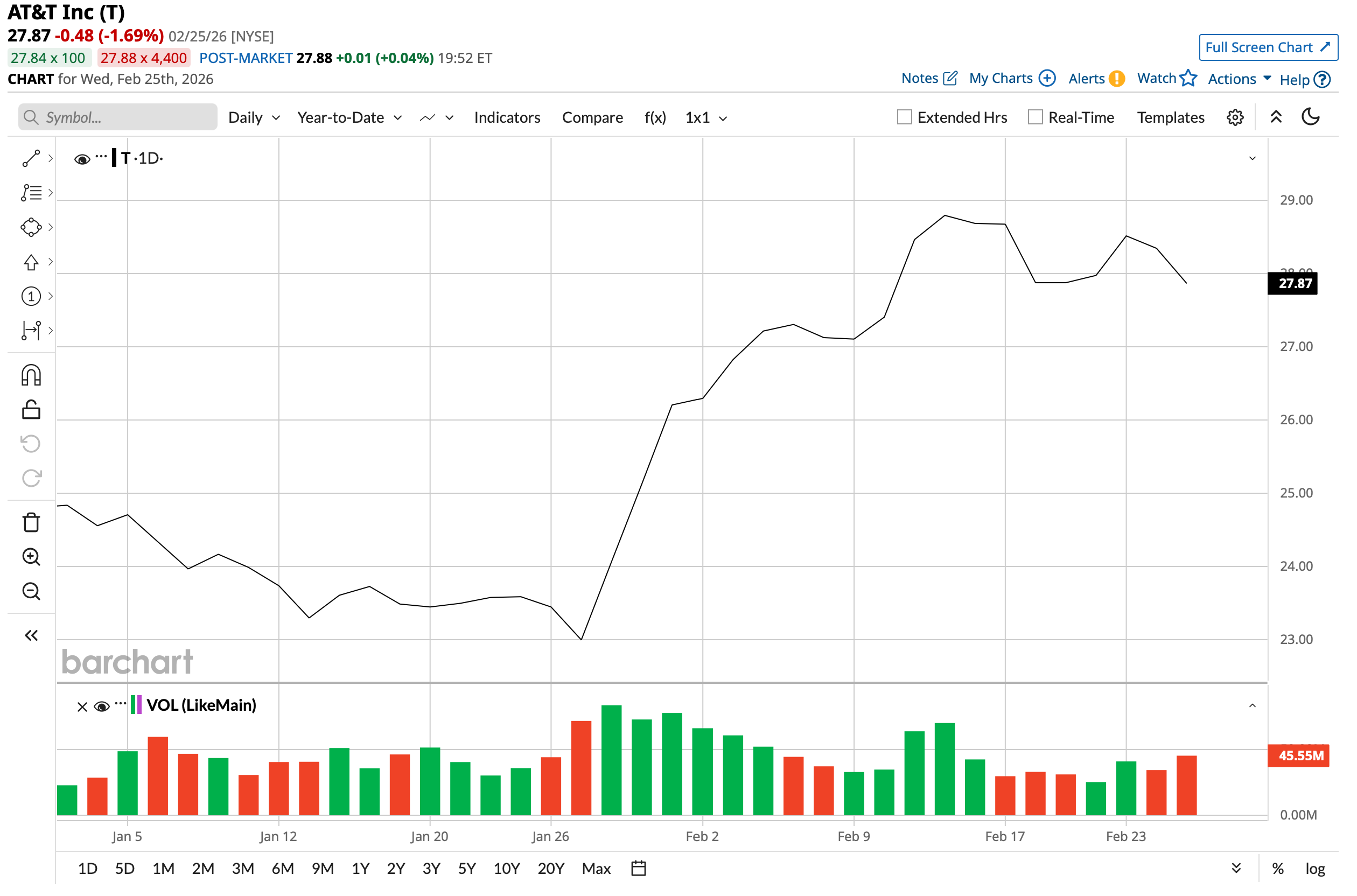

The company's market cap currently stands at $196 billion, with T stock offering a dividend yield of 3.96%, which is higher than the sector median. Overall, T stock is up 13% on a YTD basis.

Notably, the company's latest results for Q4 showed a beat on both the top and bottom line. While revenues grew nearly 4% from the previous year to $33.5 billion, earnings went up by 21% in the same period to $0.52 per share. Notably, this marked another quarter showing an earnings beat from the company.

Although cash flow from operating activities witnessed a slight decline on a YOY basis, it remained robust at $11.3 billion. Overall, the company ended the quarter with a cash balance of $18.2 billion, exceeding its short-term debt levels of about $9 billion.

In terms of valuation, T stock seems undervalued. Its forward P/E and P/CF ratios of 12.1 and 5.4, respectively, are lower than the sector medians.

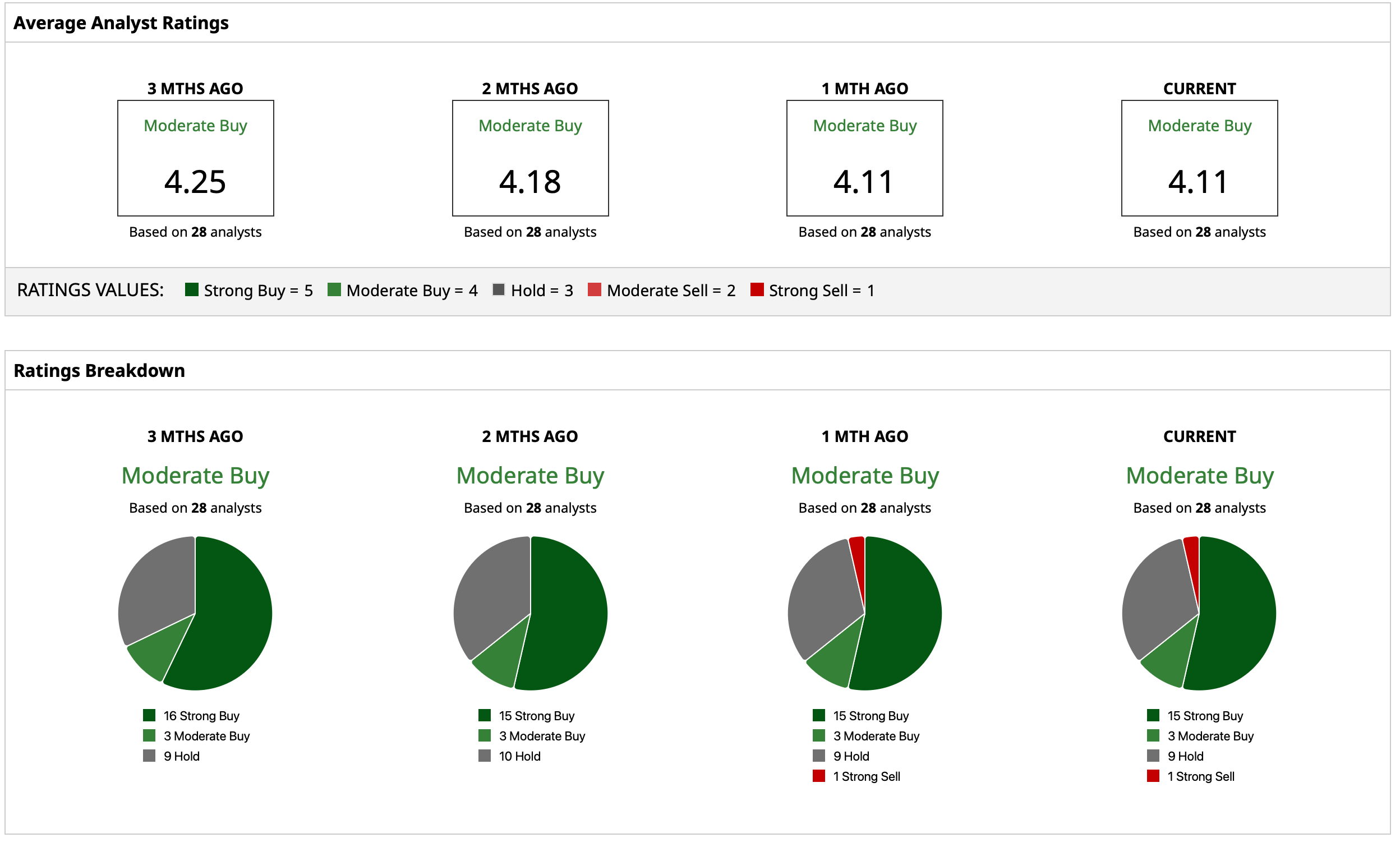

Analysts have an overall rating of “Moderate Buy” for the stock, with a mean target price of $29.63 denoting potential upside of about 6% from current levels. Out of 28 analysts covering the stock, 15 have a “Strong Buy” rating, three have a “Moderate Buy” rating, nine have a “Hold” rating, and one has a “Strong Sell” rating.

Income Stock #3: Western Midstream Partners (WES)

Western Midstream Partners (WES) is an energy infrastructure company founded in 2007. Its core business is the midstream segment of the oil and gas value chain, including gathering, compressing, treating, and transporting natural gas, crude oil, and natural gas liquids (NGLs), as well as processing gas and handling produced water for upstream producers. It owns and operates extensive pipeline networks, processing facilities, and storage systems across Texas, New Mexico, and the Rocky Mountains region.

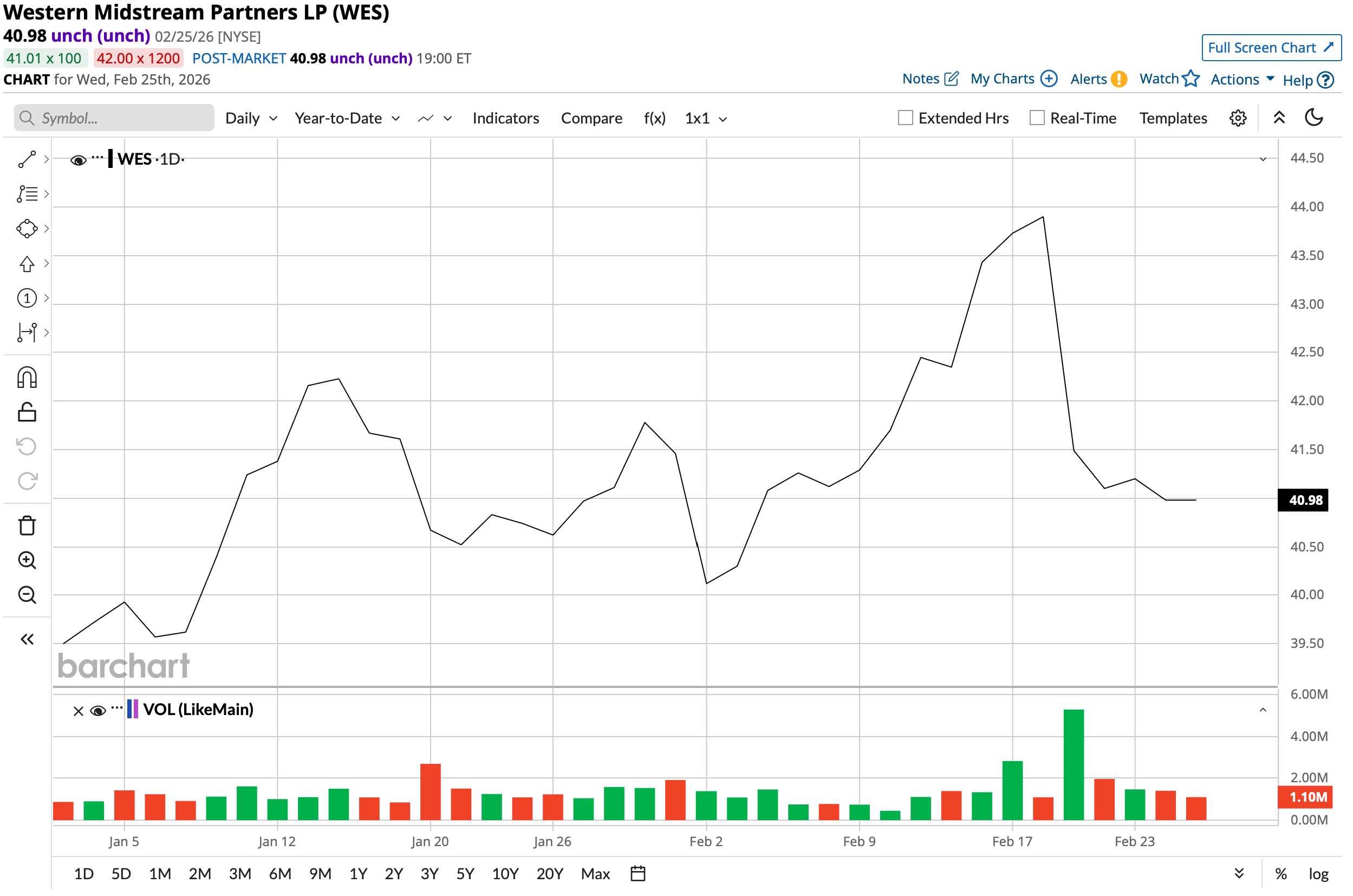

Valued at a market cap of $16.4 billion, WES stock is up 6% on a YTD basis. The stock offers a healthy dividend yield of 8.75%, which is high even for energy companies that are generally quite generous with their dividend payouts.

That said, Western Midstream's latest quarterly results were poor, with both revenue and earnings missing estimates. Total revenues for the quarter came in at just above $1 billion, higher by 11% on a YOY basis. However, earnings cratered to just $0.47 per share from $0.85 per share in the previous year as operating expenses shot up by 41% in the same period to $$744.2 million.

Net cash from operating activities increased to $2.22 billion in 2025 from $2.14 billion in 2024, as the company closed the quarter with a cash balance of $819.5 million, lower than its current liabilities of $1.24 billion.

Valuations are also sending mixed signals. While the forward P/E multiple of 12.2 times is lower than the sector median of 16, the P/CF ratio of 8.9 times is higher than the sector median of 6.5.

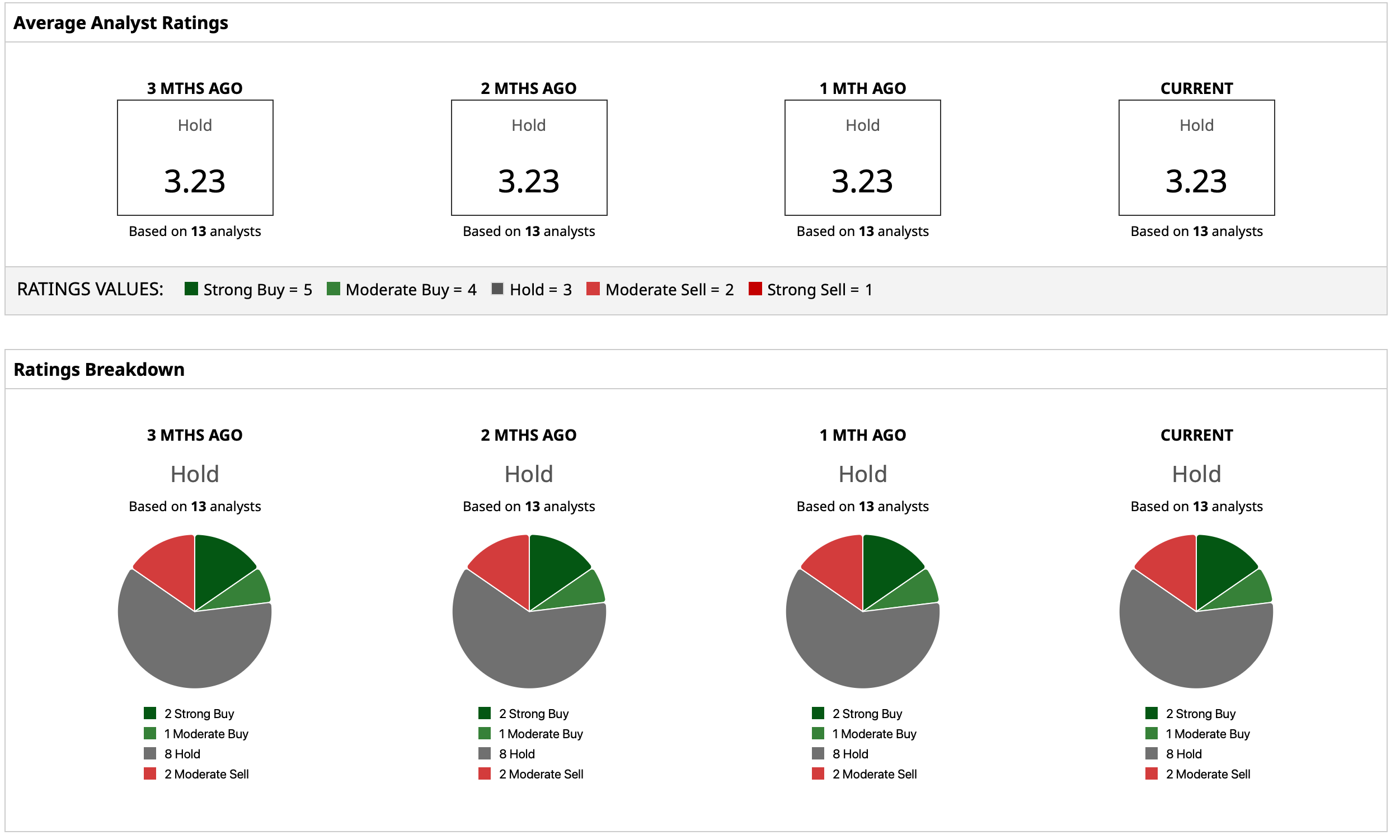

Analysts have deemed WES stock as a consensus “Hold,” with a mean target price of $42 in-line with current levels. Out of 13 analysts covering the stock, two have a “Strong Buy” rating, one has a “Moderate Buy” rating, eight have a “Hold” rating, and two have a “Moderate Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart