SoFi Technologies (SOFI) shares have declined 44% from their 52-week high of $32.73, reflecting mounting pressure on high-growth fintech stocks. The pullback has been driven by investor concerns over equity dilution following recent capital raises, the company’s elevated valuation after a strong rally, and a broader risk-off market environment.

Despite these headwinds, SoFi’s underlying business fundamentals remain solid. The company has continued to diversify its revenue base, expanding beyond lending into fee-based and capital-light segments that offer more stable, scalable income streams. This strategic shift reduces reliance on interest-sensitive lending revenue and supports longer-term margin resilience.

Management has also taken steps to mitigate share dilution, seeking to balance capital needs with shareholder value considerations.

With operational momentum and a solid revenue mix, SoFi is set to deliver strong growth in 2026.

SoFi’s Growth Trajectory Remains Solid

SoFi delivered strong growth in 2025, with operating momentum expected to continue in the years ahead. The company’s expanding member base and accelerating product adoption will continue to drive its top line.

In the fourth quarter of 2025, SoFi added 1 million new members, bringing total membership to 13.7 million, a 35% increase year-over-year (YoY). Product growth was similarly robust, with 1.6 million new products added during the quarter, driving a 37% YoY increase in total products. Cross-buy activity remained high, with 40% of new products opened by existing members, reflecting the company’s ability to deepen multiproduct relationships.

This growth translated into strong financial results. For the full year 2025, revenue increased 35%, while adjusted earnings per share (EPS) rose 160%.

Management’s 2026 outlook indicates strong growth ahead. SoFi expects total membership to grow by at least 30% YoY. Adjusted net revenue is projected to reach approximately $4.7 billion, implying roughly 30% annual growth. Adjusted EBITDA is expected to total about $1.6 billion, representing an annual EBITDA margin of approximately 34%. And the adjusted EP is forecasted at approximately $0.60, up from $0.39 in 2025.

Over the medium term, management expects adjusted net revenue to grow at a CAGR of at least 30% from 2025 through 2028. SoFi’s adjusted EPS is projected to grow at a CAGR of 38% to 42% over the same period.

A key driver of this growth is the increasing contribution from capital-light, non-lending, and fee-based revenue streams. Growth in SoFi’s Loan Platform business remains solid. Meanwhile, higher referral fees, interchange revenue, and brokerage fees are supporting a more diversified revenue mix. Fee-based revenue increased 50% in Q4 and is now running at nearly $1.8 billion annually, enhancing earnings stability.

Monetization metrics are also improving. Annualized financial services revenue per product reached $104 in the fourth quarter, up 29% from $81 a year earlier, with further upside expected as newer products mature and customer engagement deepens.

The Loan Platform Business was a notable contributor in the fourth quarter, generating $194 million in adjusted net revenue, equivalent to an annualized run rate of $775 million, nearly three times the level recorded in the same period a year earlier. In 2026, SoFi expects sustained demand from both existing and new partners in the Loan Platform business, which will drive its financial results. In addition, interchange revenue will continue to grow, supported by higher spending volumes across money and credit card products.

Lending performance is also likely to remain solid. Notably, lending revenue rose 15% in Q4, driven by higher loan originations.

SoFi’s deposits increased to $37.5 billion, lowering funding costs and supporting improved profitability in the coming years. Overall, SoFi will likely continue to scale its diversified financial services platform and deliver strong revenue and earnings in the coming years, which will support its share price.

Is SOFI Stock a Buy Now?

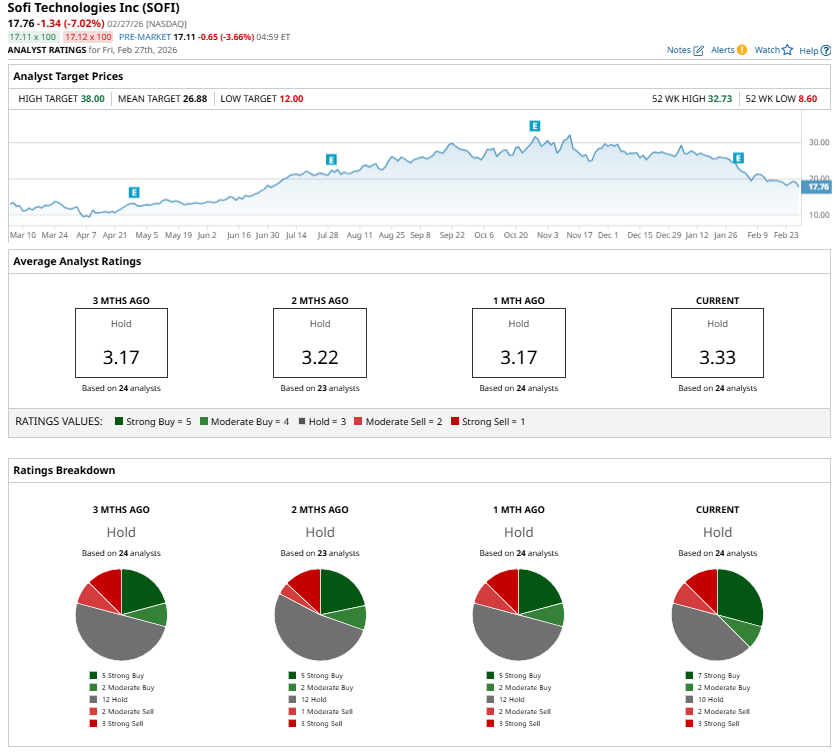

While analysts maintain a “Hold” consensus rating on SOFI stock, sustained member growth, improving monetization, accelerating fee-based revenue, and strengthening profitability will likely drive the stock higher.

Concerns about shareholder dilution also appear overstated. The company’s recent capital raises have strengthened its balance sheet by enabling it to pay down higher-cost debt, thereby reducing interest expense. At the same time, SoFi has been able to deploy excess capital into yield-generating assets, producing incremental interest income. When viewed in totality, this additional income can offset the impact of dilution and may even make the transactions accretive to EPS.

Finally, the recent pullback in SOFI's price has moderated valuation pressures. With its fundamentals continuing to improve and management projecting strong growth ahead, the decline presents an attractive buying opportunity.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart