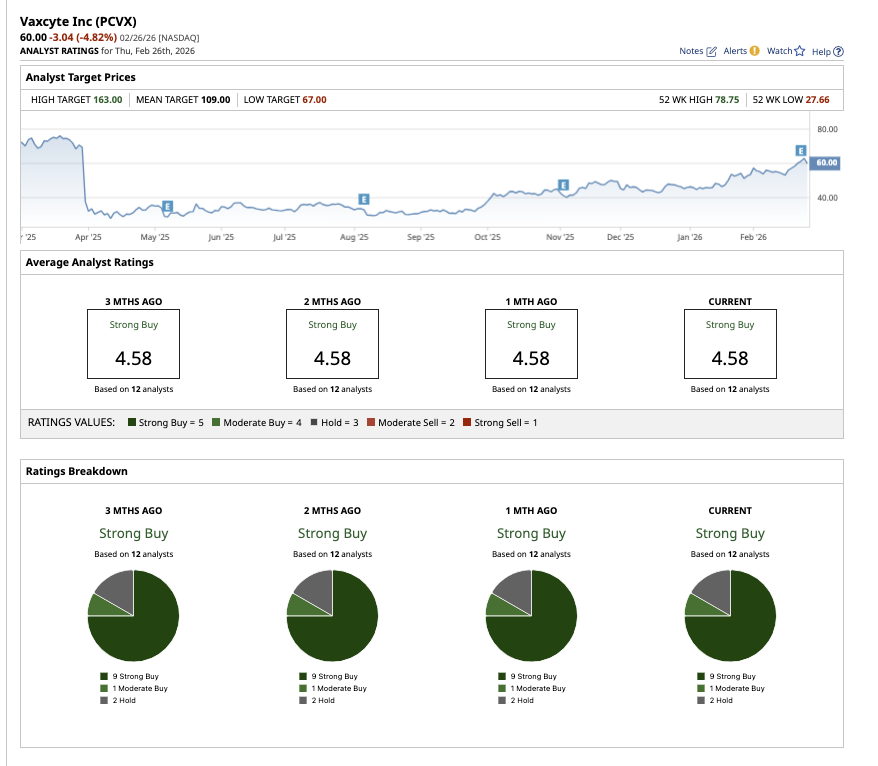

Vaxcyte (PCVX) is a clinical-stage vaccine innovation company focused on developing next-generation vaccines to protect people from serious bacterial infectious diseases. While Vaxcyte is still a clinical-stage company, Wall Street seems highly optimistic about PCVX stock, rating it as a consensus “Strong Buy” and forecasting potential upside of 76% from current levels based on the average price target of $109.

Vaxcyte is even attracting long-term growth investors' interest. This small-cap biotech is up 35% so far this year, outperforming many Big Tech names.

Let’s find out whether it is the right time to grab PCVX stock now.

What Is So Enticing About Vaxcyte?

Wall Street’s enthusiasm stems from a rare combination of late-stage momentum, differentiated science, and a stable balance sheet. Vaxcyte’s pneumococcal conjugate vaccine (PCV) portfolio — which includes VAX-31 and VAX-24 — is one of the main reasons for the bullish outlook.

Currently, VAX-31 — a 31-valent PCV candidate — is in three separate Phase 3 adult clinical programs and a Phase 2 infant program. The company expects data from one trial by the fourth quarter of 2026, with additional Phase 3 results in 2027. Compared to existing standard-of-care vaccines, this candidate is designed to prevent invasive pneumococcal disease (IPD) and pneumonia by targeting more serotypes. The U.S. Food and Drug Administration (FDA) has also designated the Breakthrough Therapy designation to VAX-31 to include prevention of pneumococcal pneumonia in addition to IPD. This broadens the vaccine's use significantly upon commercialization.

Meanwhile, the company’s other lead candidate has reported positive data from the Phase 2 infant trial in the recent Q4 print. It should be appealing to long-term investors that Vaxcyte isn’t betting on a single asset. In fact, it is building an entire franchise in one of the largest global vaccine markets.

A Massive Market Opportunity

Pneumococcal disease remains a global health concern. IPD is a highly contagious bacterial infection causing serious complications and death worldwide among older adults and infants. Vaxycte distinguishes itself from typical vaccine makers by using XpressCF, a cell-free protein synthesis technology licensed exclusively from Sutro Biopharma (STRO). The majority of vaccine makers cultivate their vaccine ingredients in live cells. However, in this method, portions of the vaccine are generated in a highly controlled lab facility.

This is useful since pneumococcal illness is caused by several evolving serotypes of the bacteria, which might change over time. If Vaxcyte succeeds, its vaccine will be more competitive and potentially more effective, giving it an advantage in the market. Vaxcyte's pipeline extends beyond the PCV franchise as well. In 2026, the company is planning a Phase 1 study for VAX-A1, a vaccine candidate targeting Group A Strep. It is also developing VAX-GI, which aims to prevent Shigella infections.

As a clinical-stage company with no revenue-generating products yet, Vaxcyte reported a net loss of $766.6 million for 2025. This is not unusual for a late-stage clinical biotech aggressively investing in development and manufacturing scale-up.

In fact, Vaxcyte appears confident in its vaccine development, having already completed the building of a specialized large-scale manufacturing facility with Lonza (LZAGY) and having begun a U.S. fill-finish buildout. Nonetheless, it has one of the most robust balance sheets among late-stage vaccine developers. The firm ended Q4 with $2.4 billion in cash, cash equivalents, and investments, excluding an additional $600 million in net proceeds from a February 2026 equity offering.

Biotech investors often fear stock dilution, which can happen when a company runs out of capital and has to raise money by issuing new stock. For now, it appears Vaxcyte is in a safe position. The company expects its cash balance to support the runway for Phase 3 trials, manufacturing buildout, and eventual commercialization activities without immediate funding constraints.

While the bull case is enticing, clinical-stage biotech stocks carry risk. The Phase 3 outcomes will determine Vaxcyte's future, which might go either way. PCVX stock can soar if things go right, but it could also fall sharply if they don’t. If you are someone who is craving a little risk and willing to handle it, you might want to grab this growth stock now. As the saying goes, “Fortune favors the bold.”

What Do Analysts Think of Vaxcyte Stock?

Analysts remain strongly bullish about Vaxcyte’s long-term prospects. Of the 12 analysts who cover the stock, nine recommend it as a “Strong Buy,” one calls it a “Moderate Buy,” and two rate the stock as a “Hold.” The average analyst target price for PCVX is $109, representing a 76% potential increase from current levels. Furthermore, Mizuho Securities analyst Salim Syed has set a high price target of $163, implying potential upside of 163% from current levels.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- As Billionaire David Tepper Takes Aim at Whirlpool Stock, Should You Buy, Sell, or Hold WHR Now?

- Are the Magnificent Seven Stocks Losing Steam? Should You Buy, Hold, or Sell?

- Why Oppenheimer Says Oracle Stock Can Gain 25% from Here

- Analysts Think LegalZoom Stock Can Double in 2026. Should You Buy It Here?