With a market cap of $80.4 billion, Cintas Corporation (CTAS) is a leading provider of corporate identity uniforms and related business services across the United States, Canada, and Latin America. The company operates through segments including Uniform Rental and Facility Services, First Aid and Safety Services, and All Other services.

Companies valued more than $10 billion are generally considered “large-cap” stocks, and Cintas fits this criterion perfectly. Cintas serves small businesses and major corporations by renting, servicing, and selling uniforms and facility products, as well as offering first aid, safety, and fire protection solutions through an extensive distribution and delivery network.

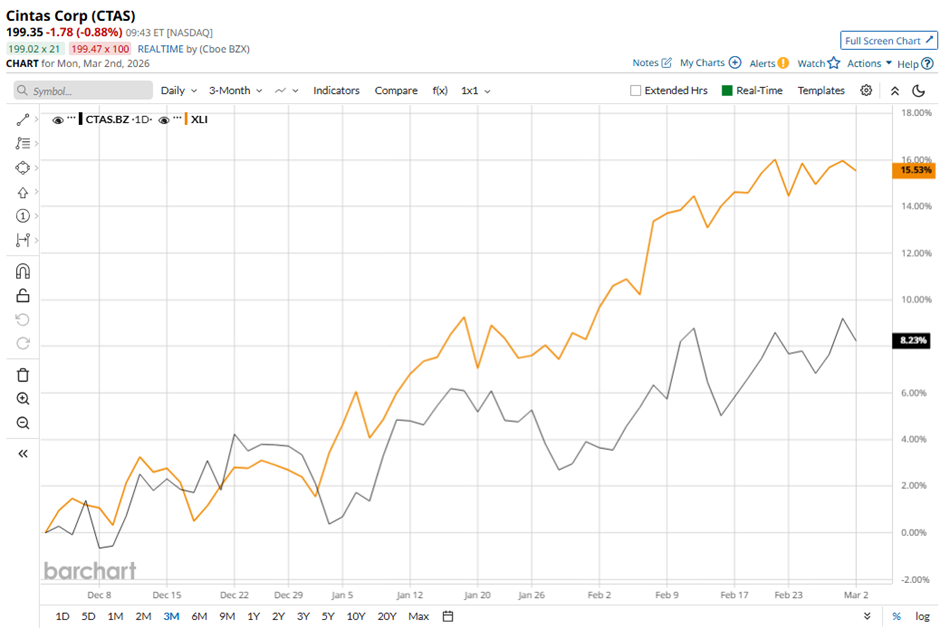

Shares of the Cincinnati, Ohio-based company have declined 13.2% from its 52-week high of $229.24. CTAS stock has risen 9.7% over the past three months, lagging behind the State Street Industrial Select Sector SPDR ETF’s (XLI) 15.9% increase over the same time frame.

CTAS stock is up 7.4% on a YTD basis, underperforming XLI’s 14.1% increase. In the longer term, shares of Cintas have dipped 2.7% over the past 52 weeks, compared to XLI’s 29.8% return over the same time frame.

The stock has fallen below its 200-day moving average since September 2025.

Shares of Cintas rose 1.3% on Dec. 18 after the company reported strong Q2 2026 results, highlighted by revenue of $2.8 billion, up 9.3% year-over-year. Investor sentiment was further boosted by improved profitability, as operating income increased 10.9% to $655.7 million, operating margin reached an all-time high of 23.4%, and EPS grew 11% to $1.21. The stock also benefited from management raising full-year fiscal 2026 guidance, increasing expected revenue to $11.15 billion - $11.22 billion and EPS to $4.81 - $4.88.

In comparison, CTAS stock has lagged behind its rival, Eaton Corporation plc (ETN). ETN stock has soared 18% on a YTD basis and 28.2% over the past 52 weeks.

Despite Cintas’ weak performance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of “Moderate Buy” from the 22 analysts covering the stock, and the mean price target of $218.50 is a premium of 9.5% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart