Earnings season is in full swing, yet the market’s reaction has been anything but predictable. The companies that beat estimates often suffer sharp selloffs as investors punish weak guidance, margin misses, or looming cash needs rather than rewarding top-line beats. That risk-off haircut has been especially painful for capital-intensive clean-energy names, where execution and financing concerns overshadow encouraging results.

Against this backdrop, notably, Plug Power's (PLUG) upcoming March 2 report looms large. Plug sits at the crossroads of policy-driven demand and heavy capitalization, so the Q4 print will test whether recent contract wins, asset sales, and government backing are translating into sustainable revenue, shrinking losses, and a clearer path to profitability for the broader hydrogen and fuel-cell industry.

About PLUG Stock

Plug stands out as an early hydrogen pioneer. It has deployed over 72,000 fuel-cell systems and hundreds of fueling stations, serving giants like Amazon (AMZN) and Walmart (WMT). The company offers a one-stop green-hydrogen solution, from electrolyzers and liquid hydrogen to fuel cells, positioning itself as a leader in decarbonization infrastructure.

Hydrogen stocks haven’t offered investors a smooth ride lately. While long-term policy support for clean energy remains intact, concerns around funding needs and execution timelines have kept the group on edge. That’s been especially true for Plug Power even after it secured a $1.66 billion loan guarantee from the U.S. Department of Energy in January, a meaningful endorsement of its ambitious expansion plans.

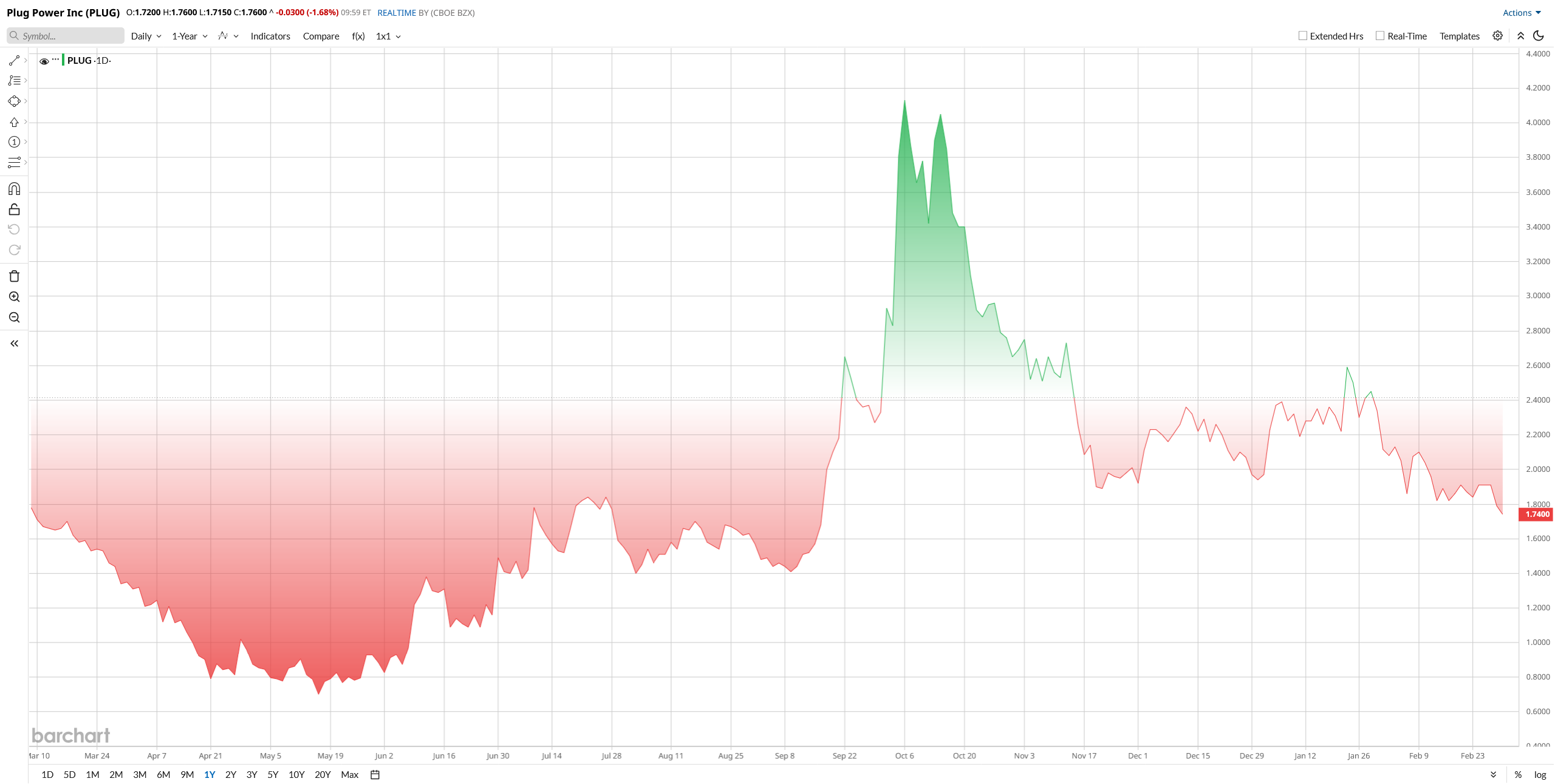

Over the past year, the stock has been up roughly 10%, but that modest gain trails the broader market. Each rally sparked by government backing or new supply agreements has been tempered by profit shortfalls and lingering dilution fears.

PLUG presents a mixed valuation scenario. Although its price/book ratio is 1.61, significantly lower than the sector median of 3.56, indicating some level of underpricing, its EV/sales of 5.67 is considerably higher than the sector median of 2.42, suggesting an expensive stock compared to its peers. In other words, Plug trades at a premium on sales and book value, reasonable only if its rapid growth and future profits materialize.

Plug Power Q4 Earnings Preview

Plug Power will report its Q4 2025 earnings after the market closes today, March 2. Wall Street expects a continued net loss but further narrowing. The consensus forecast is about -$0.10 EPS on roughly $217 million in sales. Notably, this is the first report under new CEO Jose Luis Crespo, who officially took the helm on March 1, making the earnings call his de facto debut to investors. Management has not changed its full-year targets, so it still aims for roughly $700 million in 2025 revenue and says cost-cutting (its “Project Quantum Leap”) is on track to push gross margins toward break-even by late 2025.

Technical models imply significant volatility that options traders price in around a 20% swing on the report. Investors will focus on Crespo’s strategy and any 2026 guidance. If Plug can beat expectations or outline a credible path to profitability, especially on the electrolyzer ramp-up, the stock could pop. Conversely, any shortfall or renewed financing concerns could prompt a sharp drop.

Recent News and Deals

Plug has been busy raising capital with recent actions. Last week, it agreed to sell part of its Project Gateway hydrogen site to Stream Data Centers for $132.5 million upfront, up to $142 million. This is the first step in a plan to generate about $275 million of liquidity via asset sales, restricted-cash releases, and other initiatives.

Moreover, Plug’s technology is also winning contracts. In November 2025, NASA tapped Plug to supply liquid hydrogen for its rocket centers, about 220 tonnes of fuel, as part of a $147 million program. Plug’s electrolyzer division is likewise expanding; for example, late 2025 saw new multi-megawatt electrolyzer orders in Europe and Africa. These partnerships highlight that major customers continue to embrace Plug’s solutions even as the company addresses its cash burn and execution challenges.

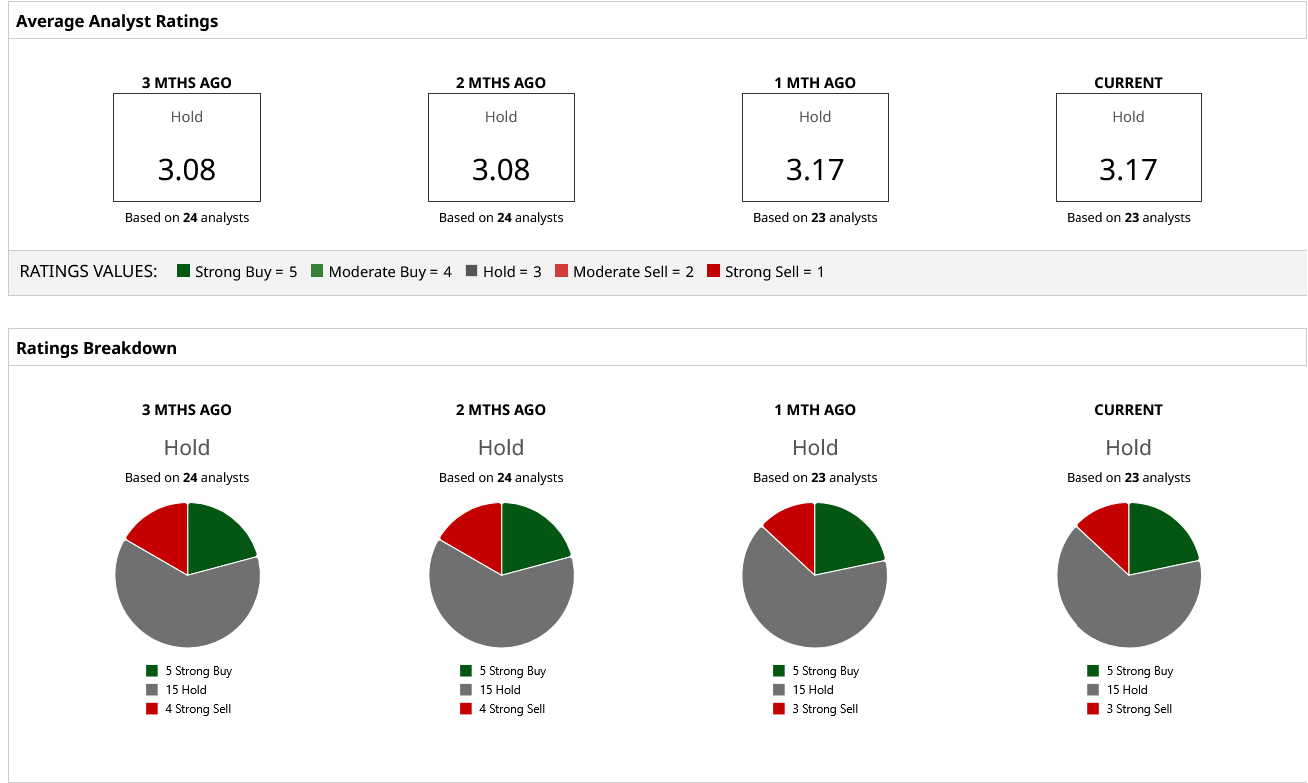

Analysts' Outlook on PLUG Stock

Wall Street analysts have taken a cautious stance on PLUG stock. Morgan Stanley maintains an “Underweight” stance with a $1.50 price target.

By contrast, more bullish firms like H.C. Wainwright and Canaccord have set $7 targets for late 2025.

J.P. Morgan’s analysts have noted that new tax-credit clarity from the so-called “One Big Beautiful Bill” should remove a major overhang for green-hydrogen projects, but they remain neutral on the stock.

Overall, the 30-analyst consensus target is roughly around $2.9, which implies an expected 70% upside potential over the current price.

In short, it looks like Wall Street is mostly on the sidelines. Any upgrades or updated guidance in today's call could therefore drive outsized moves in the share price.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart