Meta (META) is not where it was supposed to be in the AI race. While Anthropic's Claude, Alphabet's (GOOG) (GOOGL) Gemini, and OpenAI's ChatGPT compete fiercely for the top position in the realm of AI chatbots, Meta AI is nowhere in the conversation. Damningly for Mark Zuckerberg, direct rival xAI's Grok model has also surged ahead of it.

This was not the case about a year ago, when, with the announcement of Superintelligence and after assembling a super team of AI veterans helmed by Scale AI's Alexander Wang, Meta was perceived to be the frontrunner in AI. Well, the stock is down more than 14% since then, and its market cap has corrected to $1.6 trillion from $1.7 trillion.

However, the social media giant remains convinced that its bet on AI will not be a dud like the metaverse. In fact, reports are emerging that, thanks to efficiency gains from AI, the company is mulling over culling 20% of its workforce. Notably, if this comes to fruition, this would be its biggest job cut since late 2022 and early 2023.

Also, the expected job cuts would help save costs for Meta's massive AI capex for 2026, which is forecasted to be in the range of $115 billion and $135 billion.

Nevertheless, it is the implication on the stock that market participants are interested in. How does META stack up as a stock now? Let's find out.

Robust Fundamentals

Meta's financials are as good as it gets, and after a rare earnings miss in the previous quarter (due to a one-time tax charge), the company is back on its familiar path of beating estimates.

Q4 2025 saw the company reporting revenues of $59.9 billion, up 24% from the prior year, as the average price per ad increased by 6% on a year-over-year (YoY) basis, supporting revenue growth. Earnings increased by 11% in the same period to $8.88 per share, surpassing the Street's expectations of an EPS of $8.21. Over the past nine quarters, Meta's earnings came in ahead of the consensus estimate on eight occasions.

The long-term track record is impressive as well, with Meta growing its revenue and earnings at a healthy CAGR of 27.34% and 32.27%, respectively.

Shifting back to Q4, the number of daily active people (DAP) across the company's family of apps rose by 7% from the prior year to $3.58 billion, as this led to the company reporting net cash from operating activities of $36.2 billion in the December 2025 quarter. Overall, the company closed the quarter with a cash balance of $81.6 billion, much higher than its short-term debt levels of $2.2 billion. The figure is even higher than its long-term debt levels of about $59 billion, implying that the company’s balance sheet remains robust.

Meanwhile, in Q1 2026, Meta expects revenue to be in the range of $53.5-56.5 billion, the midpoint of which would denote an annual growth rate of 30%.

However, the stock's muted share price performance was not enough to bring down its valuation to reasonable levels. Its forward P/E, P/S, and P/CF at 20.92, 6.32, and 11.78 are all above the sector medians of 12.98, 1.24, and 7.64, respectively. Yet, in terms of the forward PEG ratio, Meta seems to be undervalued at both the absolute and relative levels at 0.93, compared to the sector median of 1.18.

Meta Is Opting for Stealth in AI

In my last piece analyzing Meta, I had made a case as to why, despite its myriad set of concerns, Meta will continue to trudge on and remain relevant in the AI race. In a nutshell, it is too big to ignore, and its hegemony in the social media space is unparalleled (only TikTok looks like a serious competitor to me).

And it's not that it is not using AI to drive growth. It is doing exactly that at what it does best: driving ad spends from advertisers. Meta is integrating large language models into its advertising recommendation engines across the Family of Apps ecosystem. The two primary growth metrics for this segment, Family DAP and average price per ad, both accelerated in the second half of fiscal 2025, providing early evidence that the company's AI investments are translating into stronger monetization performance.

Meanwhile, although delayed, Meta's next-generation AI model, Avocado, remains a closely watched development. Designed with a focus on logical reasoning, coding capabilities, and agentic behavior, it represents a deliberate shift toward a closed, proprietary model architecture. Currently, Avocado appears to be lagging in certain areas. While internal benchmarks show efficiency gains over prior Llama models and superiority to Google's Gemini 2.5, leaked external evaluations indicate it trails behind leading frontier systems such as Gemini 3.0 and OpenAI's latest offerings. To generate returns on the massive $115-$135 billion in projected 2026 AI-related capital expenditures, Meta intends to commercialize Avocado through an enterprise SaaS-style subscription model and API access.

Finally, Meta has also accelerated its efforts in custom silicon development. On March 11, the company announced plans to roll out four new generations of its MTIA (Meta Training and Inference Accelerator) chips over the next two years. These chips target ranking and recommendation workloads as well as generative AI inference tasks. Each successive generation is expected to deliver substantial improvements in compute performance, memory bandwidth, and power efficiency, enabling Meta to migrate a larger portion of its inference workloads onto in-house hardware.

As MTIA chips gain the ability to support larger context windows with higher HBM bandwidth and greater compute density, Meta's reliance on third-party GPUs should gradually decrease. This transition from renting external compute resources to owning and optimizing its own silicon portfolio represents one of the most significant long-term margin-expansion opportunities for the company, and one that current market pricing has yet to fully reflect.

Analyst Opinion on META Stock

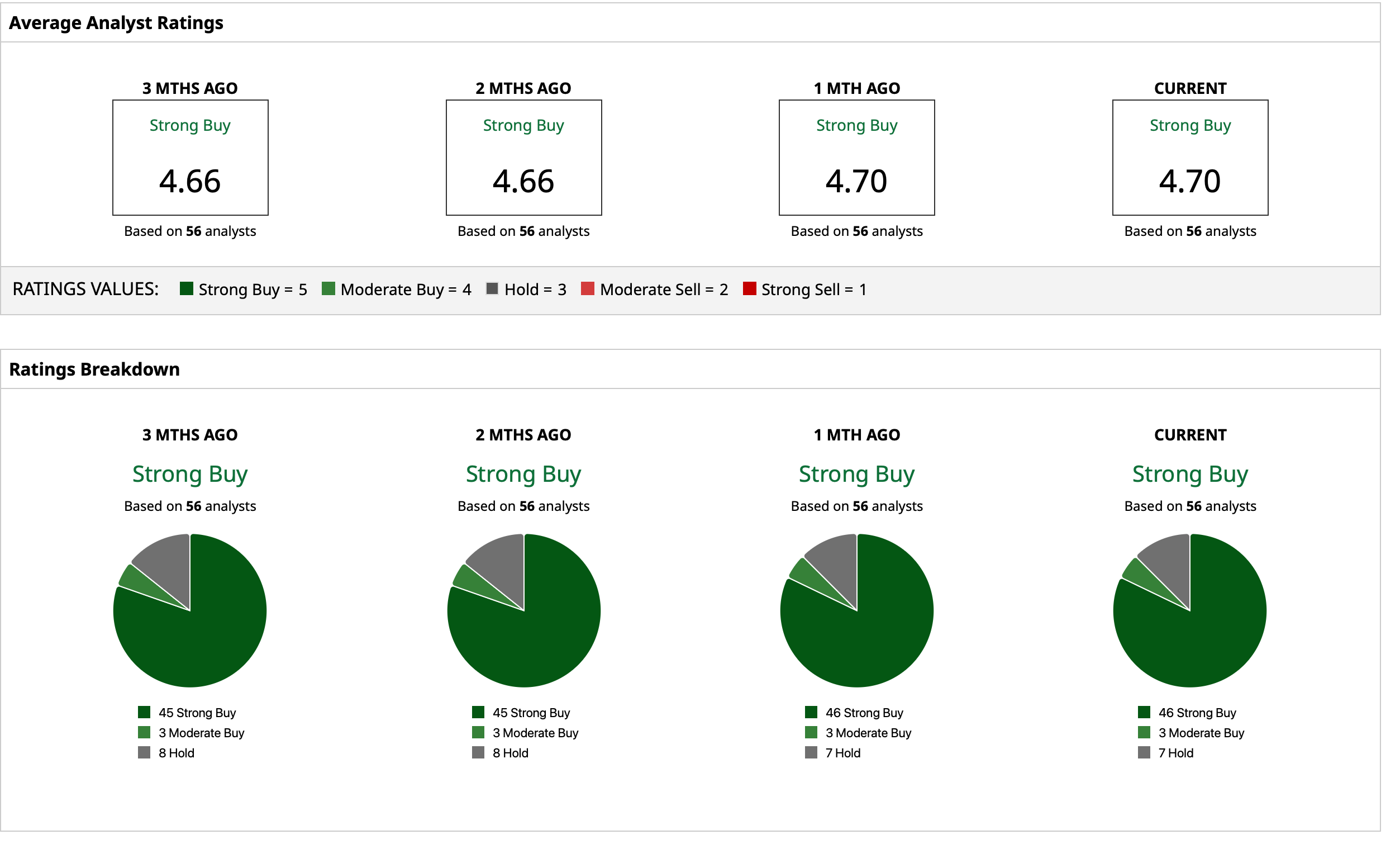

Thus, analysts have earmarked an overall rating of “Strong Buy” for the stock, with a mean target price of $864.04. This denotes an upside potential of about 39% from current levels. Out of 56 analysts covering the stock, 46 have a “Strong Buy” rating, three have a “Moderate Buy” rating, and seven have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Palantir Is Launching New AI OS Reference Architecture with Nvidia. Should You Buy PLTR Stock?

- As Tesla Gears Up to Launch Terafab, Is TSLA Stock a Buy?

- Add Global Exposure to Your Portfolio with This 1 Norwegian ETF

- Meta Could Cut 20% of Its Jobs as AI Costs Pile Up. Should You Buy, Sell, or Hold META Stock Before Layoffs?