The broad U.S. market has been driven by tech gains lately, while big-cap value plays like Berkshire Hathaway (BRK.A) (BRK.B) have remained relatively quiet. Investors in diversified outfits, insurers, industrials, and consumer conglomerates are watching cash-rich companies carefully.

Now, once again, all eyes are on Berkshire as the company is all set to report its 2025 annual report and earnings online on February 28. This means shareholders and analysts will get CEO Greg Abel’s first annual letter alongside the full-year results. In today’s environment of rising interest rates and cautious capital deployment, Abel’s comments could be a guide for how Berkshire aims to “move the needle” next.

Berkshire’s Diversified Empire and Cash Strength

Berkshire Hathaway, run by legendary investor Warren Buffett until year-end 2025, is a sprawling conglomerate. What makes Berkshire unique is Buffett’s decades-long value philosophy and the company’s humongous cash hoard of over $380 billion, giving it unmatched firepower to invest or buy back shares.

Besides the routine updates, Berkshire’s last few months have seen notable moves. In late 2025, it re-entered media by accumulating about 5.07 million shares of The New York Times around $352 million, its first newspaper bet in years, while quietly trimming stakes in Apple (AAPL) and Amazon (AMZN).

It also boosted positions in energy, adding Chevron (CVX), Chubb (CB), and paring some financial holdings. And in January 2026, Berkshire closed its acquisition of OxyChem (OXY), a leading chemicals maker, for nearly $9.7 billion. These moves show the new management’s selective approach, picking spots where Buffett saw value, but still holding huge cash as a buffer. Analysts say these deals have not dramatically swung the share price yet, but they hint at the strategic areas Abel may focus on.

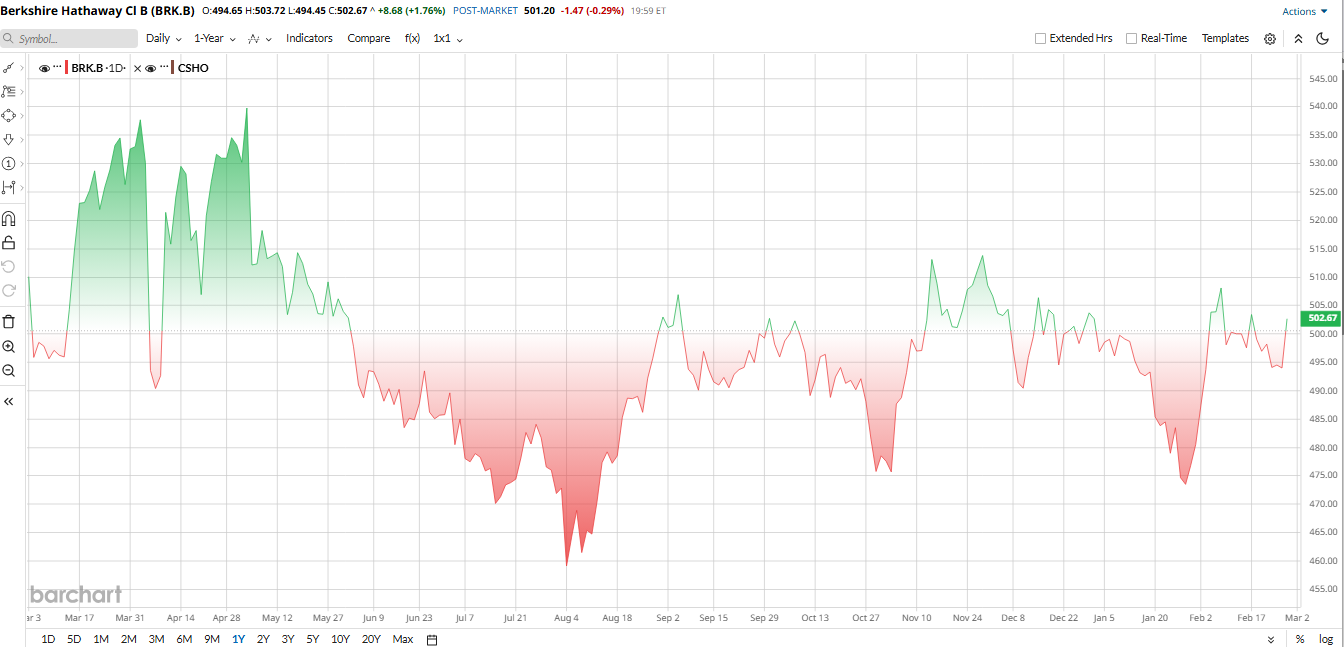

Berkshire’s stock isn't moving

Over the past 52 weeks, Berkshire’s stock rose modestly, roughly 2% underperforming the booming S&P 500 ($SPX) gain of 16%. Its businesses saw steady gains, but investors worry its $381.7 billion cash pile isn’t earning much and that Buffett’s successors have put a temporary pause on stock buybacks. Large equity stakes like Apple and Bank of America were trimmed in 2025, reflecting management’s cautious stance. Overall, earnings growth helped gains, but a “cash drag” and no major M&A kept performance muted.

On a valuation basis, Berkshire’s shares aren’t exactly cheap. The stock trades around 1.5× book value, compared to roughly 1× for a typical bank or insurer. Its trailing P/E is about 16× earnings, modestly above the 14× average in financials. In short, Berkshire sits a bit rich versus sector medians. This suggests the market expects solid stability, and keeps a close eye on whether that cash could be deployed more aggressively.

Mark Your Calendars for February 28

Berkshire Hathaway is set to release its full annual report and fourth-quarter earnings on Feb. 28 at around 8 a.m. ET, a closely watched update that will also feature Greg Abel’s first annual shareholder letter as CEO. Having officially taken the helm on Jan. 1, Abel is expected to outline his strategic priorities and provide insight into how Berkshire plans to deploy its roughly $381 billion cash position. Investors will be looking for signals on capital allocation, particularly whether share repurchases accelerate, acquisitions resume, or dividends enter the discussion. With the letter arriving alongside the final 2025 results, markets will directly weigh Abel’s commentary against operating performance, making this release an early benchmark for Berkshire’s leadership transition.

Analysts broadly expect Berkshire’s fourth-quarter results to cap another solid year. The company previously reported record annual operating profit of $47.44 billion, and consensus estimates suggest 2025 earnings could approach similar levels, implying quarterly operating profit in the $12 billion to $15 billion range. Insurance underwriting strength, stable railroad performance at BNSF, and consistent earnings from Berkshire Hathaway Energy are expected to remain key contributors. However, quarterly net income may fluctuate depending on investment gains or losses tied to market movements.

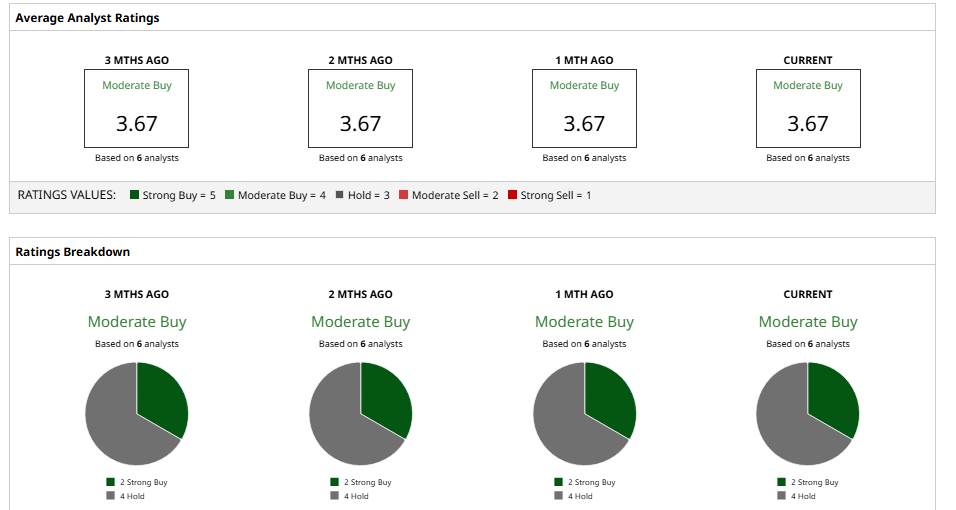

Wall Street Take on Berkshire Hathaway

Wall Street's opinion on Berkshire Hathaway Stock is moderately bullish. The group of 6 analysts tracked by Barchart has a consensus "Moderate Buy" rating with a split of 2 “Strong Buy” and 4 “Hold”. The average 12-month price target of $532 suggests the stock could surge nearly 6% from the current price.

In general, analysts praise Berkshire’s wide economic moat and cash buffer, but many note that without Buffett at the helm, management will need to prove it can maintain growth, a theme likely to come up in Abel’s letter.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart