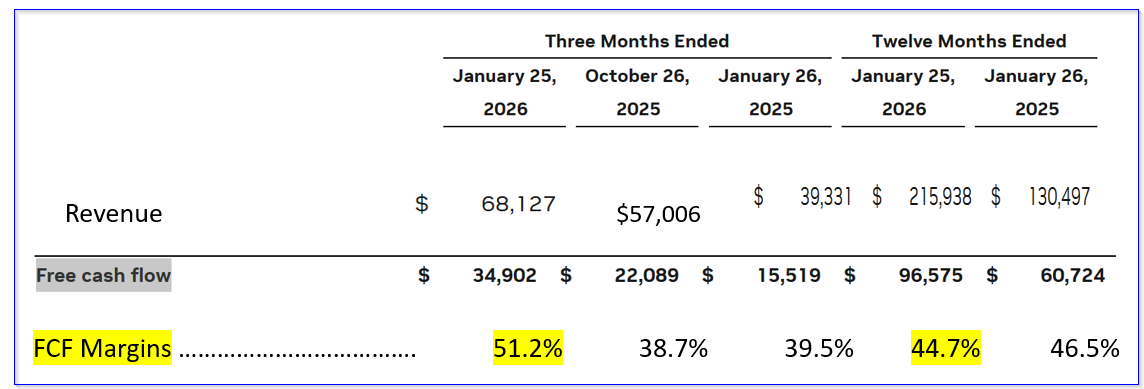

Nvidia, Inc. (NVDA) generated a massive 124% YoY growth in free cash flow (FCF) in Q4 and 59% in 2025. On Feb. 25, Nvidia's earnings release showed that its FCF margins were over 51% of sales in Q4 and 44.7% in 2025.

If that persists, NVDA stock could be worth at least 45% more at $263 per share. This article will show why and how analysts are valuing NVDA stock.

NVDA is at $181.67 in midday trading on Friday, Feb. 27. It's well below a pre-earnings release of $195.56 on Feb. 25, but up from a recent trough closing of $171.88 on Feb. 5. Its 6-month peak was $206.88 on Nov. 3, 2025.

It's very likely that once investors digest the strength of Nvidia's free cash flow (FCF) and its FCF margins, NVDA stock could rebound to well over that high. Here's why.

Nvidia's Strong FCF and FCF Margins

On Feb. 25, Nvidia, Inc. reported that its Q4 revenue rose 20% over Q3 and 73% YoY for the quarter ending Jan. 25, 2026.

More importantly, it reported that its free cash flow (FCF) was $34.9 billion, up 58% QoQ and +124.8% YoY. Its full-year 2026 FCF was up 59%.

In other words, FCF rose faster than revenue. That has huge implications for its FCF margins and operating leverage.

This can be seen in the table above, taken from the earnings release (my analysis of the FCF margins). It shows that in Q4, FCF represented over 51% of sales, up from 39% in Q3 and 40% a year ago.

The full-year FCF margin was slightly lower than in 2024, at 44.7%, but it remains very high. Given that its Q4 margins were higher, Nvidia may keep producing this 44.7% FCF margin over the next year.

Forecasting FCF

Analysts have significantly raised their revenue estimates for the year ending Jan. 2027 and the following year. Seeking Alpha's survey of 41 analysts shows $364.38 billion projected for this year and $449.22 billion for 2027 (ending Jan. 2028).

That implies that if Nvidia can keep making at least a 44% FCF margin this year, FCF could be over $160 billion:

$364.38 billion 2026 x 0.44 = $160.3 billion 2026 FCF estimate

That's 66% higher than the $96.6 billion in FCF generated in 2025. Moreover, over the next 12 months (NTM), assuming revenue averages $406.8 billion, it could rise over 85%:

$406.8b NTM revenue x 0.44 = $179 billion NTM FCF

This has huge implications for upside in NVDA's underlying value and its price targets.

Price Targets for NVDA Stock

If Nvidia were to pay out 100% of its $96.6 billion in FCF last year, the dividend yield would have been 2.19%. This is because its market cap today is $4.418 trillion, according to Yahoo! Finance:

$96.6b / $4,418b = 0.02186 = 2.19% FCF yield

We can use that metric to value its FCF going forward. Just to be conservative, let's make the FCF yield even higher at 2.50%:

$160.3b 2026 FCF est / 0.025 = $6,412 billion mkt cap

That is 45% higher than today's market capitalization of $4.418 trillion. In other words, NVDA could be worth 45% more:

$181.67 x 1.45 = $263.42 price target (PT)

It would be even higher using the NTM FCF estimate:

$179/0.025 = $7,160b

$7,160b / $4,418 = 1.62

1.62 x $181.67 = $294.30 PT

This means the FCF-based PTs range between $263 and $294 for the next year. Analysts tend to agree. For example, Yahoo! Finance's survey of 61 analysts is $262.51.

And AnaChart's survey of 37 analysts is $234.92 per share.

The bottom line here is that NVDA stock looks deeply depressed, assuming its FCF growth and FCF margins stay strong over the next year.

That implies that investors buying NVDA have a good probability of making money.

In a follow-up article, I will show that it makes sense to both short out-of-the-money (OTM) NVDA puts expiring in one month, as well as buy longer-dated in-the-money (ITM) NVDA call options.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- 52 Massive Vol/OI Spikes Expire March 20—Profit Plays on Top 3

- Uber Air Is Officially Here. Does That Make Uber Stock a Buy on Flying Car Dreams?

- ‘This is Not Business as Usual. This is Risk’: Michael Burry Warns Nvidia Looks Strikingly Similar to Cisco Just Prior to Dot Com Bubble Crash

- Warren Buffett Warns, ‘You Do Not Adequately Protect Yourself by Being Half Awake While Others Are Sleeping’