Michael Burry, the investor who famously foresaw the 2008 housing collapse, is back in the spotlight, and this time questioning the artificial intelligence (AI) spending spree by tech giants. He raised concerns over these players, including Alphabet (GOOG) (GOOGL) as to whether they can sustain massive investments in AI infrastructure without jeopardizing cash flow and earnings.

Burry’s worry is not abstract. Alphabet’s projected 2026 capital expenditures are set to nearly double last year’s levels to build data centers, procure AI chips, and scale its Gemini AI platform across Search and Cloud. He warns that such spending could collapse free cash flow (FCF), push companies into debt, and force complex accounting maneuvers to protect earnings. He questions when the end is in sight.

Despite Burry’s warnings, some market experts urge caution before reading too much into the timing of AI returns. The underlying question for investors is the balance between the promise of AI and the weight of its cost.

With Alphabet spending at record levels and GOOGL stock slipping, should investors stay invested and trust the long game, or step back and wait for clarity?

About Alphabet Stock

Alphabet hardly needs an introduction in global technology circles. Headquartered in California and valued at roughly $3.8 trillion by market cap, it stands as one of Silicon Valley’s most influential forces. Far beyond Search, Alphabet has expanded into AI, cloud infrastructure, autonomous mobility through Waymo, and advanced research led by DeepMind. Its Gemini models reflect an ambition not just to join the AI race, but to define it.

The market has taken note. Renewed confidence in Google’s AI execution and cloud momentum has supported a strong stock performance, securing Alphabet’s place comfortably within the world’s most valuable companies.

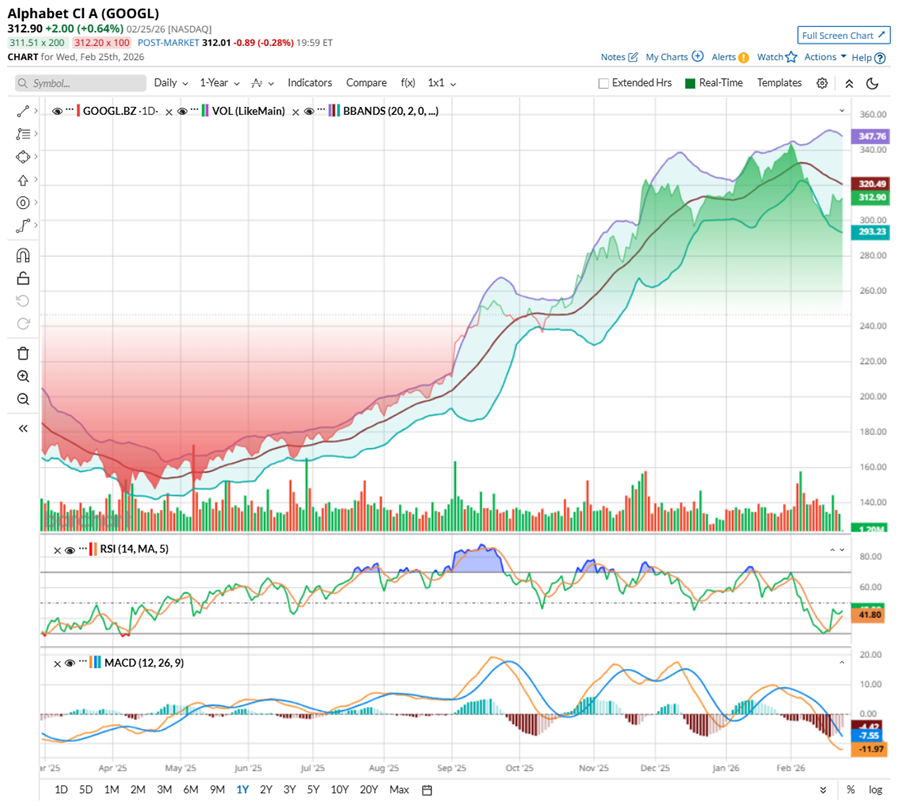

Alphabet has had quite a run. Not long ago, GOOGL tagged a 52-week high at $349, signaling that investor confidence in the tech giant, especially its AI ambitions, was alive and well. But markets rarely move in straight lines. Since that early February peak, the stock has pulled back about 13.5% and declined 7.8% over the past month as questions swirl around the pace and payoff of Alphabet’s aggressive AI spending.

Nevertheless, perspective matters. Even with the recent dip, shares remain up 77.95% over the past year and roughly 48.39% in just six months. In fact, the stock has gained 1.5% in just the last five days, hinting that buyers may be stepping back in. That’s not a broken chart, but a stock catching its breath.

The recent pullback, shaped in part by investor unease over heavy AI spending, is clearly visible on the technical chart. After an extended rally, GOOGL is taking a breather. Volume lacks strong accumulation on rebounds. The 14-day RSI has eased back to roughly 40, stepping away from levels of 70 it reached in early February, reflecting fading buying strength but not yet extreme pessimism. Plus, it resets conditions for a more sustainable move higher.

From a Bollinger Band perspective, the tone has shifted. After spending months pressing against the upper band during its strong advance, GOOGL has eased back toward the middle band, signaling that upside momentum has cooled. The bands remain relatively wide, reflecting elevated volatility. However, continued doubts around heavy AI capex may push the stock toward lower band support before confidence returns.

At the same time, the MACD oscillator shows the cooling momentum after a strong run. The MACD line slid below the signal line with negative histogram bars, confirming short-term bearish pressure.

After a strong run over the past year, GOOGL stock may look expensive at first glance, trading above its sector average and its on historical median. Priced at 26.84 times forward adjusted earnings, the valuation feels measured for a company delivering high-teen revenue growth and riding powerful momentum in Google Cloud. This is not a one-engine story either. Alphabet’s diversified business and fortress balance sheet add stability. It even pays a dividend now. With earnings poised to expand further, today’s multiple could quietly age well.

A Closer Look at Alphabet’s Stellar Q4 Report

The Google-parent closed 2025 on a strong note, delivering a fourth-quarter performance on Feb. 4 that underscored how deeply AI is now woven into its growth engine. For the quarter ended that ended on Dec. 31, revenue rose 18% year-over-year (YOY) to $113.8 billion, comfortably ahead of consensus. EPS came in at $2.82, up 31% annually and also beating expectations, as both Search and Cloud outperformed. For the full year, Alphabet’s revenue surpassed $400 billion for the first time in its history, with AI-led capabilities driving acceleration across core businesses.

Yet the shares slipped after the report, as investors quietly questioned whether GOOGL can truly turn its AI-loaded services into profits fast enough to justify that massive CapEx roadmap.

Google Services, the company’s largest segment spanning Search, YouTube, and subscriptions, generated $95.5 billion in revenue, up 14% YOY. Search and other advertising revenue climbed 17% to $63.1 billion, supported by stronger user engagement and improved monetization as AI-powered features enhanced results and ad relevance. YouTube advertising rose 9% to $11.4 billion, driven by solid direct-response demand despite tough comparisons.

The standout once again was Google Cloud. Revenue surged 48% to $17.7 billion, reflecting accelerating enterprise demand for AI infrastructure and solutions. Google Cloud Platform continued to gain traction with higher win rates, larger long-term commitments, and deeper spending from existing customers. Enterprise AI offerings are now generating billions in quarterly revenue. Backlog rose 55% sequentially and more than doubled annually to $240 billion, highlighting multi-year AI contracts across a diverse enterprise base.

Profitability remained healthy. Operating income jumped 31% to $31 billion, with margins at 31.6%. But beneath that strength, FCF margin eased to 21% YOY as quarterly capital spending surged to $27.9 billion. For the full year, CapEx reached $91.4 billion, largely funneled into technical infrastructure, with roughly 60% into servers and the remaining 40% into data centers and networking equipment.

And yet, Alphabet ended the year with more than $126 billion in cash, supporting continued buybacks and dividends. The company funded $5.5 billion in buybacks and $2.5 billion in dividends in Q4 alone.

Looking ahead, management guided 2026 capital expenditures to between $175 billion and 185 billion – nearly double 2025 levels – to expand AI and cloud capacity. While this heavier investment weighs on near-term FCF, leadership emphasized AI agents, Search upgrades, and enterprise momentum as key pillars for sustained growth into 2026 and beyond.

Wall Street analysts tracking Alphabet sees its earnings inching up steadily. For fiscal 2026, EPS is projected to rise about 7.1% YOY to $11.58, before growing by another 14.6% annually to $13.27 in fiscal 2027.

What Do Analysts Expect for Alphabet Stock?

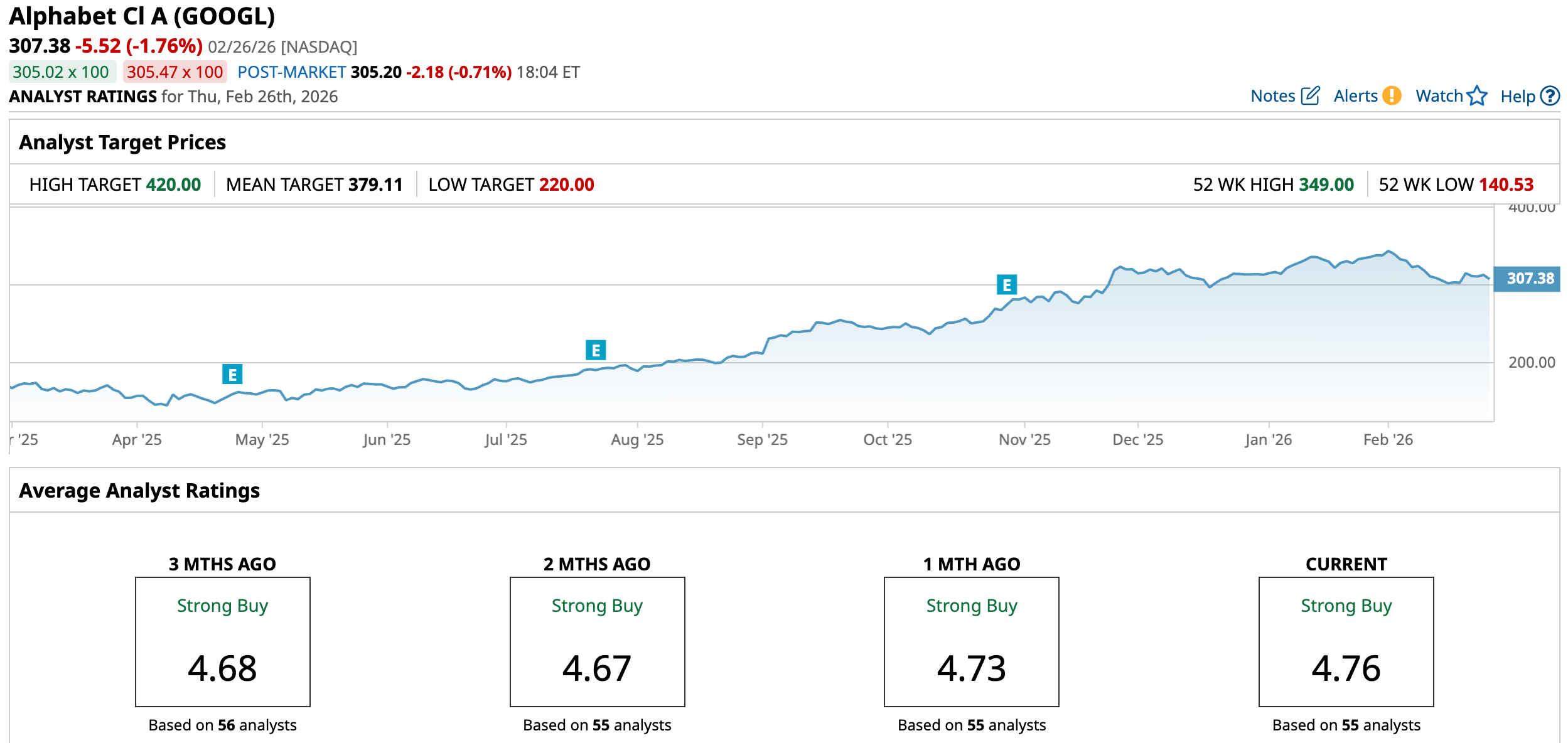

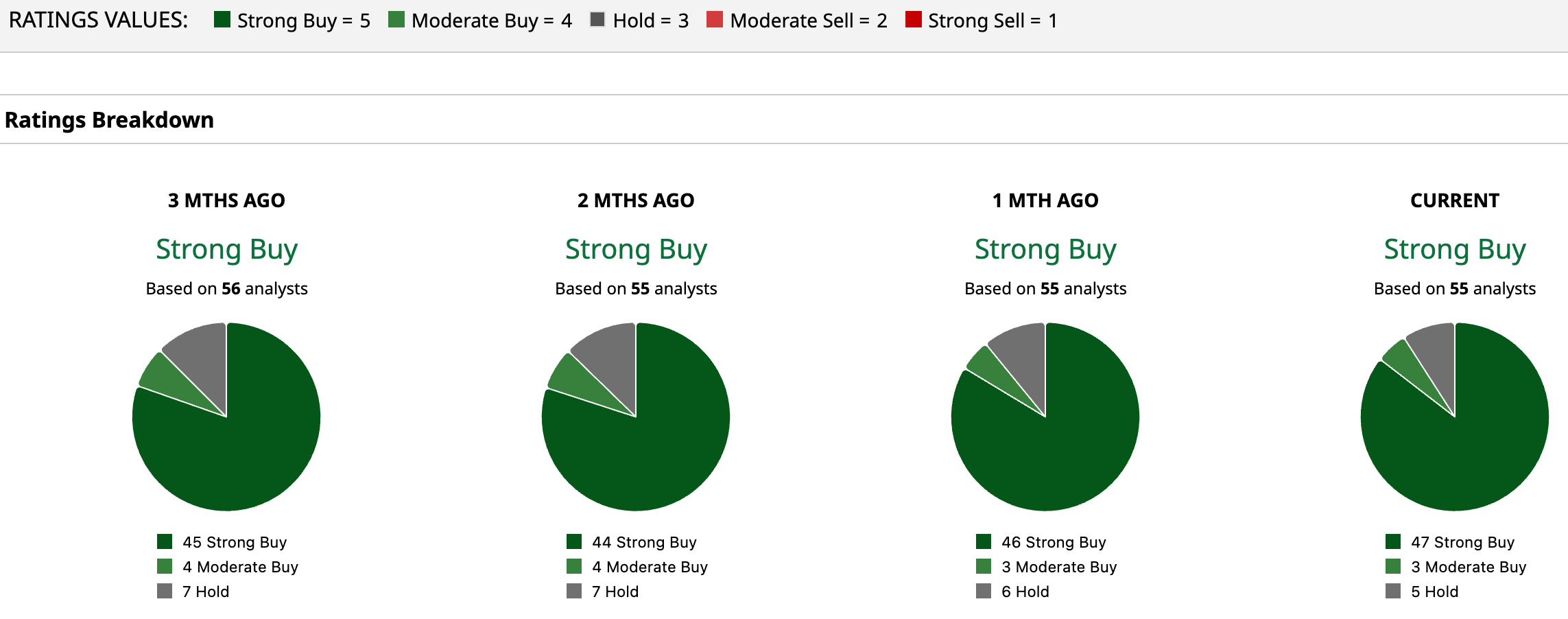

Analysts monitoring GOOGL are optimistic, with consensus of “Strong Buy” rating overall. Out of 55 analysts, 47 recommend a “Strong Buy,” three suggest a “Moderate Buy,” and five are playing it safe with a “Hold” rating.

The average price target of $379.11 suggests a 23.34% upside potential from here. Meanwhile, the Street-high target of $420 suggests GOOGL stock could rise 36.6%.

Final Thoughts on GOOGL

Michael Burry’s caution lingers in the background, reminding investors that spending at this scale inevitably raises the stock’s risk profile. Big bets can strain cash flow in the short run, forcing companies to borrow despite resilient balance sheet. Yet history shows Alphabet has typically allocated capital wisely, and if these AI investments pay off, the long-term reward could justify today’s discomfort.

Some experts also urge investors not to overreact to timing fears. Burry’s structural concerns on depreciation and CapEx are mathematically grounded. But markets don’t always move on logic alone, especially in transformative cycles like AI. Still, with billions pouring into infrastructure and competition intensifying, this is not a quick trade. It is a long game that may require unusual patience.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- As Uber Buys SpotHero, Should You Buy, Sell, or Hold UBER Stock?

- Sam Altman Casts Doubt on Space-Based Data Centers, But This 1 Hot Stock Is Determined to Make Them a Reality

- 1 Dividend Stock to Buy Now If You Are Still Betting on Data Center Demand

- With Bearish Overhangs in the Rearview Mirror, CrowdStrike (CRWD) Stock Looks Tempting