Texas is on track to capture nearly 30% of the U.S. data center market share by 2028, as access to power increasingly decides where developers put their next sites. The state has turned into a focal point for new data center projects, with large tech companies racing to secure long-term energy deals. Just weeks ago, TotalEnergies (TTE) signed what it called its largest-ever U.S. renewable PPA for 1 GW of solar capacity over 15 years to support Google’s (GOOG) (GOOGL) data centers in Texas. And on Feb. 24, AES Corporation (AES) announced its own landmark deal with Google: 20-year Power Purchase Agreements for co-located power generation at a new data center campus in Wilbarger County, Texas. Under the agreement, AES will build and run the power assets and handle retail service, cost optimization, and energy management for Google’s facility.

BloombergNEF recently ranked AES as the top seller of clean energy to U.S. corporations, with Google as its largest corporate buyer in 2025. The company also stands out for income-focused investors, pairing a forward dividend yield of about 4.3% with a growing line-up of data center–linked power projects, which places it among the higher-yielding utilities.

So does this utility company still have room to run? Let’s find out.

The Numbers Behind the Narrative

AES Corporation is a global power company that develops, owns, and runs generation, storage, and energy infrastructure, with a growing focus on long-term clean energy contracts for large, well-known customers.

Over the past 52 weeks, the stock is up about 47%, and year to date (YTD) it has gained roughly 12%, showing how quickly investors are reevaluating its data center and renewables pipeline.

AES trades at 6.84x forward earnings versus about 19.37x for the utilities sector, which suggests the market still applies a clear discount to its earnings profile.

Income-focused investors are also getting a solid stream of cash. AES offers an annual dividend yield of about 4.33% on a $0.70 per-share payout, with the most recent quarterly dividend at $0.176 on Jan. 30, 2026. The forward payout ratio is a relatively low 33.60%, and the company has raised its dividend for 12 straight years, paying quarterly and topping the sector’s average 3.75% yield, which gives room to keep growing both the business and the payout.

Third-quarter 2025 results back up that story. GAAP net income came in at $517 million, up from $215 million a year earlier, with net income attributable to AES rising to $639 million from $504 million. Diluted EPS improved to $0.94 from $0.72, while adjusted EBITDA increased to $830 million from $698 million, and adjusted EBITDA, including tax attributes, reached $1.256 billion versus $1.174 billion. Adjusted EPS moved up to $0.75 from $0.71, showing that the growth investors are now pricing into the stock is already flowing through earnings and cash generation.

What’s Powering AES’s Next Leg of Growth

AES’s next leg of growth is already visible in its signed contracts. It has finished building Bellefield 1, a 1,000 MW solar-plus-storage project under a 15-year contract with Amazon (AMZN), the first half of a planned 2,000 MW complex that is set to be the largest solar-plus-storage facility in the United States when fully complete. With 500 MW of solar and 500 MW of four-hour battery storage in each phase, the project is built around the constant, around-the-clock power needs of large cloud and AI workloads.

At the same time, AES has secured long-term demand from another major data center customer, Meta (META). It has signed PPAs for 650 MW of solar capacity in the SPP market to support Meta’s data centers, with projects in Texas and Kansas that also create construction jobs and generate millions in long-term tax revenue for local communities. This is part of a broader buildout rather than a single push.

In its third-quarter 2025 update, AES said it is on track to bring 3.2 GW of new projects online in 2025, with 2.9 GW already finished, and has signed or been awarded 2.2 GW of new long-term renewable PPAs so far this year, including 1.6 GW tied directly to data centers. That pipeline is now feeding into headline projects such as the February 2026 “landmark agreements” with Google to place new clean generation alongside a large data center campus in Wilbarger County, Texas, under 20-year PPAs and an energy management agreement that keeps AES closely involved in the site’s operations over the long term.

What Wall Street Sees Ahead For AES Stock

Management is reaffirming 2025 adjusted EBITDA guidance of $2.65 billion to $2.85 billion, along with 2025 adjusted EPS of $2.10 to $2.26. The Street is expecting EPS of $0.62 for the December 2025 quarter, up from $0.54 a year earlier, and $0.30 for March 2026 versus $0.27 in the same quarter last year, which works out to year-over-year (YoY) growth of 14.81% and 11.11%.

Argus Research’s John Eade has taken a clearer stance on that setup. On Dec. 5, 2025, he upgraded AES from “Hold” to “Buy,” pointing to “accelerating renewables-driven earnings growth” and setting an $18 price target based on expected portfolio growth through 2027, including large data-center-linked projects like the new Google campus in Texas.

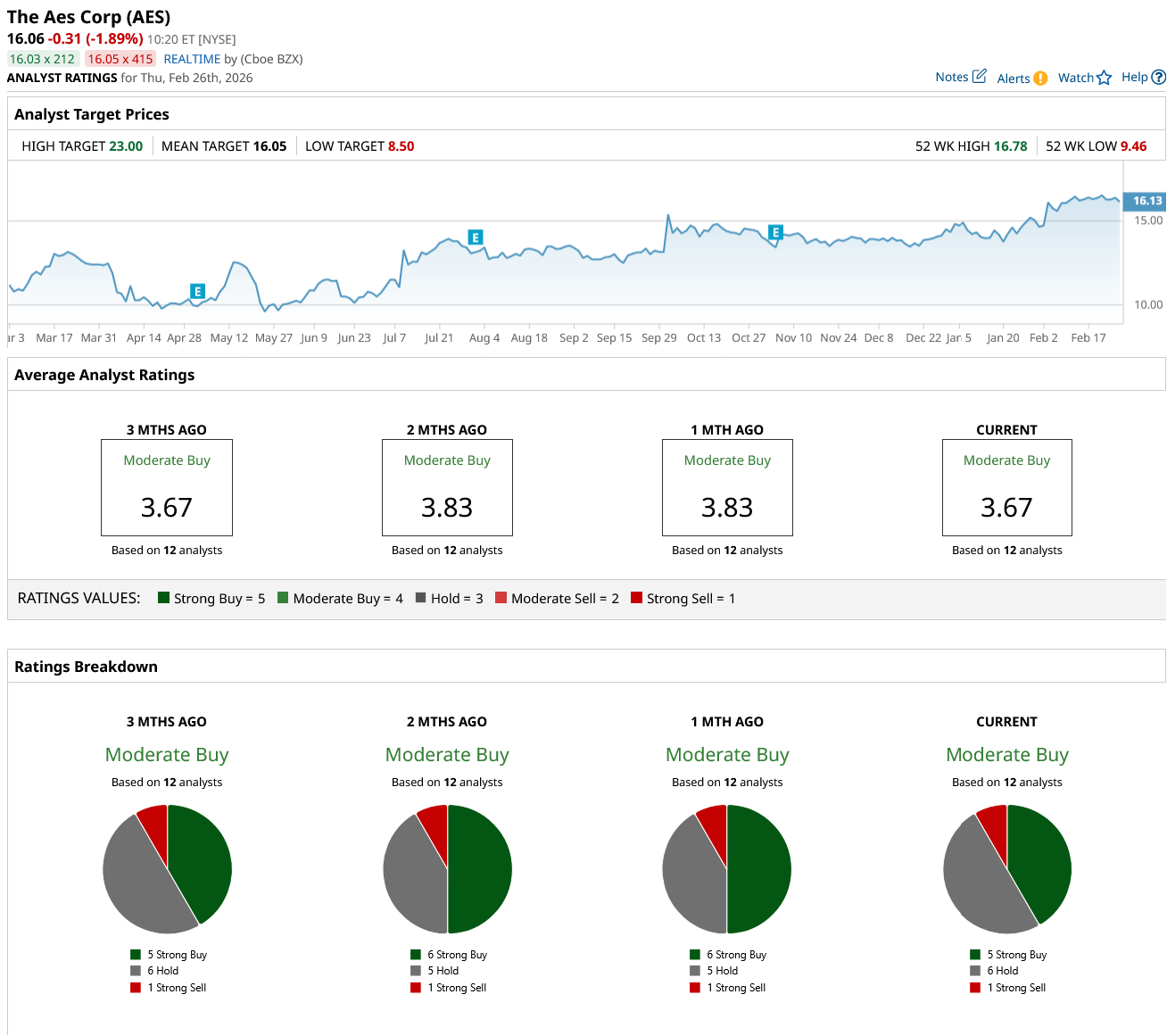

Looking across the full analyst group, all 12 covering the stock rate it a consensus “Moderate Buy,” with an average target of $16.05. With AES recently trading around $16.06, the shares sit almost exactly on par with that mean target, which suggests that Street estimates are lagging the pace at which the market is adjusting its view of AES as a high-yield, data-center-focused utility.

Conclusion

For dividend investors who want direct exposure to the data center buildout, AES looks like a legitimate contender rather than a hype play. You’re getting a near mid‑single‑digit yield, a long runway of contracted, hyperscaler-backed growth, and earnings that are already inflecting in the right direction. The valuation still prices in more caution than enthusiasm, which leaves room for total returns if management keeps hitting its numbers and converting its pipeline. In the near term, the stock probably grinds rather than spikes, but over the next few years, the bias most likely moves toward higher prices as the Google‑style deals show up in cash flow.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart