Tesla (TSLA) is the most polarizing company I have seen in my nearly two-decade investing career. On one hand are the skeptics who see the stock as highly overvalued, while the bulls believe that Tesla would eventually become the world’s biggest company.

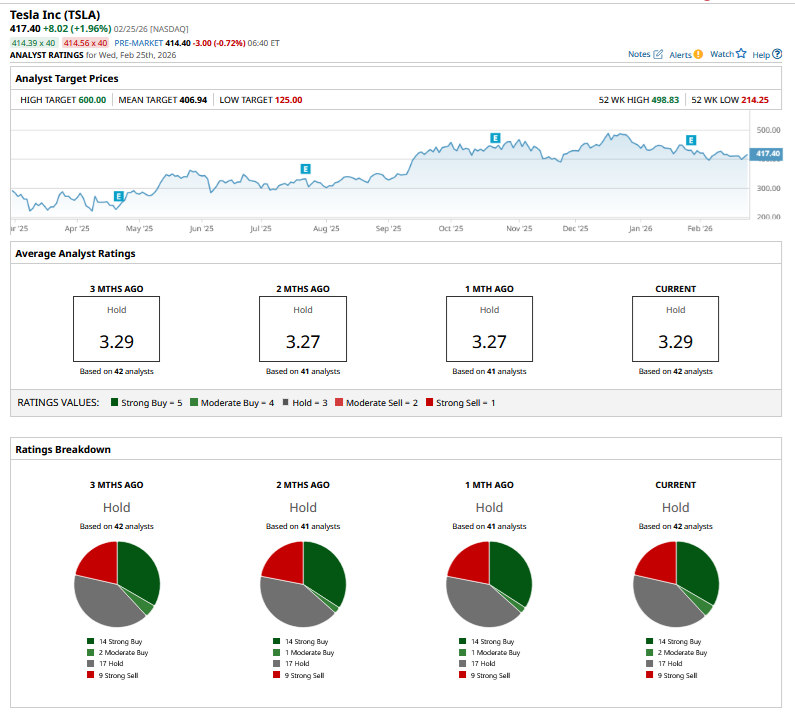

The divergence in Tesla’s target prices speaks for itself. GLJ Research analyst Gordon Johnson—the most vocal Tesla bear—values the stock at $25.28, which is by far the lowest among all sell-side analysts. On the other hand, Wedbush analyst Dan Ives has a Street-high target price of $600 on the Elon Musk-run company. The wide gulf between the most bullish and bearish voices on Wall Street cannot be starker and is big enough to easily fit Amazon (AMZN), a $2.3 trillion company and the world's biggest company by revenue, in between. We are not even talking about ARK Invest’s mid-range target price of $2600 on Tesla that the Cathie Wood-run company expects the stock to hit in three years.

To be sure, Tesla and Musk have proved skeptics wrong on more than one occasion, and the company leads the U.S. electric vehicle (EV) market by a big margin. There were concerns over it losing market share in the country, but thanks to multiple EV startups going out of business and legacy automakers pulling back on their once-ambitious EV targets, Tesla’s U.S. market share has increased to over 60%.

Tesla Is Notorious for Missing Deadlines

Meanwhile, there is also the other side of the argument, as I recall no other companies that have missed deadlines and forecasts as frequently as Tesla. The company formally withdrew the forecast of 20 million annual deliveries by 2030 and has virtually given up on the 50% annual delivery growth guidance. From projecting a million robotaxis by 2020 and perpetual promises of full autonomy “by the end of the year,” Tesla hasn’t been a shining example of meeting projections and has actually been a case of “overpromising and underdelivering.” While Musk is known to make bold projections, some of the projections looked unrealistic, and I had previously noted the questionable 20 million annual delivery forecast.

Tesla Has Pivoted to Physical AI

Meanwhile, Tesla's story is now more about artificial intelligence (AI)—specifically, Optimus humanoid, autonomous driving, and, by extension, robotaxis. While one may differ on the quantum, these two account for the bulk of Tesla’s current valuation.

Musk indeed has big expectations from the robotaxi fleet as well as Optimus, and so do those who are bullish on the company. However, there are many ifs and buts here. Firstly, both robotaxis and humanoids are in their infancy, and while there are bullish projections, such forecasts are often a bit too optimistic. We don’t need to go much further, and the current state of the U.S. EV industry is testimony to the fact that projections can be way off the mark, as the U.S. EV adoption rates should have been much higher, going by even the bearish forecasts.

The second is, of course, the execution part. To Tesla's and Musk’s credit, the company has executed quite well, and its prowess in car manufacturing is a case study in itself that even legacy automakers praise—if not in public, then in private.

The Biggest Threat to Tesla Comes from Chinese Companies

However, China remains an elephant in the room when it comes to AI products like humanoids and autonomous driving.

The question of Chinese companies entering the humanoid space did pop up during Tesla’s Q4 2025 earnings call last month. Responding to the question, Musk admitted that “by far the biggest competition for humanoid robots will be from China.” However, in his typical way, he boasted, “We believe Optimus will be much more capable than any robot that we are aware of under development in China.”

Given China’s backing of new-age companies in the EV and robotics industries and the strides Chinese companies are making in advanced manufacturing, we can be quite sure that some Chinese companies will give Tesla a run for its money in physical AI.

Is TSLA Stock a Buy?

While I believe that Tesla is one of the most consequential companies of this era, I am not too bullish on the stock’s outlook given its rich valuations. At a $1.8 trillion market cap, I don’t find enough margin of safety in Tesla shares. While I do hold a small stake in the company, I would refrain from adding more shares, as the risk-reward ratio does not look too favorable at these prices.

While I am not a perma bear on Tesla, as Gordon Johnson and I don't see the stock dropping to the levels he projects, I don’t see it rising to $600 this year, as I believe much of the physical AI story is largely priced into the stock. That said, if I were to bet on one of these outcomes, I would bet on Tesla hitting $600 rather than $25, given how vociferously the stock can react to any bullish commentary from Musk.

On the date of publication, Mohit Oberoi had a position in: TSLA , AMZN . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart