Instacart (CART), which goes by the legal name Maplebear, has evolved into a dominant digital grocery marketplace in North America. It connects customers with supermarkets, warehouse clubs, specialty retailers, and even restaurants for same-day delivery or pickup. Today, however, the company is more than just a delivery marketplace. It is now a multi-layered grocery technology platform that has even integrated artificial intelligence (AI) into the shopping experience.

While Instacart is turning into a more diversified and increasingly profitable business model, is the stock a buy, hold, or sell now?

A Business With Renewed Momentum

Instacart's online marketplace connects customers to more than 2,200 retail banners across approximately 100,000 locations. Its enterprise platform is equally strong. With its Storefront Pro offering, Instacart now supports more than 380 grocery e-commerce sites. In the fourth quarter, Instacart experienced its fastest Gross Transaction Value (GTV) growth in three years. GTV, which measures the total dollar value of all orders placed on a platform during a given period, increased 14% year-on-year (YoY) to $9.8 billion. This increase was driven by 89.5 million orders, which rose 16% YoY.

Management expects GTV to be between $10.12 billion and $10.27 billion in the first quarter of 2026, indicating an 11% to 13% YoY increase. Given the ongoing concerns about Amazon (AMZN), DoorDash (DASH), and Uber (UBER) expanding in grocery, this is impressive growth. Customer engagement trends are also showing impressive results, with more than 26 million customers having used Instacart during the year. While frequency among existing users continued to rise, there were new additions as well. This indicates that online grocery is still a relatively untapped industry, and Instacart is profiting from long-term behavioral shifts.

The company's advertising division is another high-margin growth engine. In Q4, advertising and other revenue increased 10% YoY. During the quarter, more than 9,000 brands advertised on Instacart, an increase from 7,000 during the same period last year. Instacart is also working with Meta Platforms (META), Alphabet (GOOG) (GOOGL), and The Trade Desk (TTD) to provide off-platform access to its first-party grocery data. These tech companies target high-intent consumers and measure conversion back to actual grocery purchases.

Adjusted EBITDA for the full year climbed 23% year on year to $1.08 billion, showing that operational leverage is translating into higher profitability even as the company invests in growth initiatives. However, GAAP net income fell year over year due to a one-time, nonrecurring $60 million FTC settlement.

In 2025, the company repurchased $1.4 billion in shares, with $671 million remaining in buyback authorization. It ended the quarter with $1 billion in cash and similar assets.

Analysts who cover Instacart estimate 10.6% revenue growth to $4.14 billion in 2026, followed by earnings growth of 48.5%. Revenue and earnings are expected to grow by 9% and 15.8%, respectively, in 2027. CART stock is trading at a discount of 15 times forward earnings, given the earnings growth expected.

Buy, Hold, or Sell?

Instacart is not the pandemic-era hypergrowth story anymore. It is evolving into a more balanced, multi-engine platform combining marketplace scale, enterprise SaaS integration, retail media monetization, and AI-driven efficiency. Long-term investors with a good risk appetite who can wait for the company to reach its full potential may want to accumulate shares at the dip now. Conservative investors may wish to hold on to the stock.

What Does Wall Street Say About CART Stock?

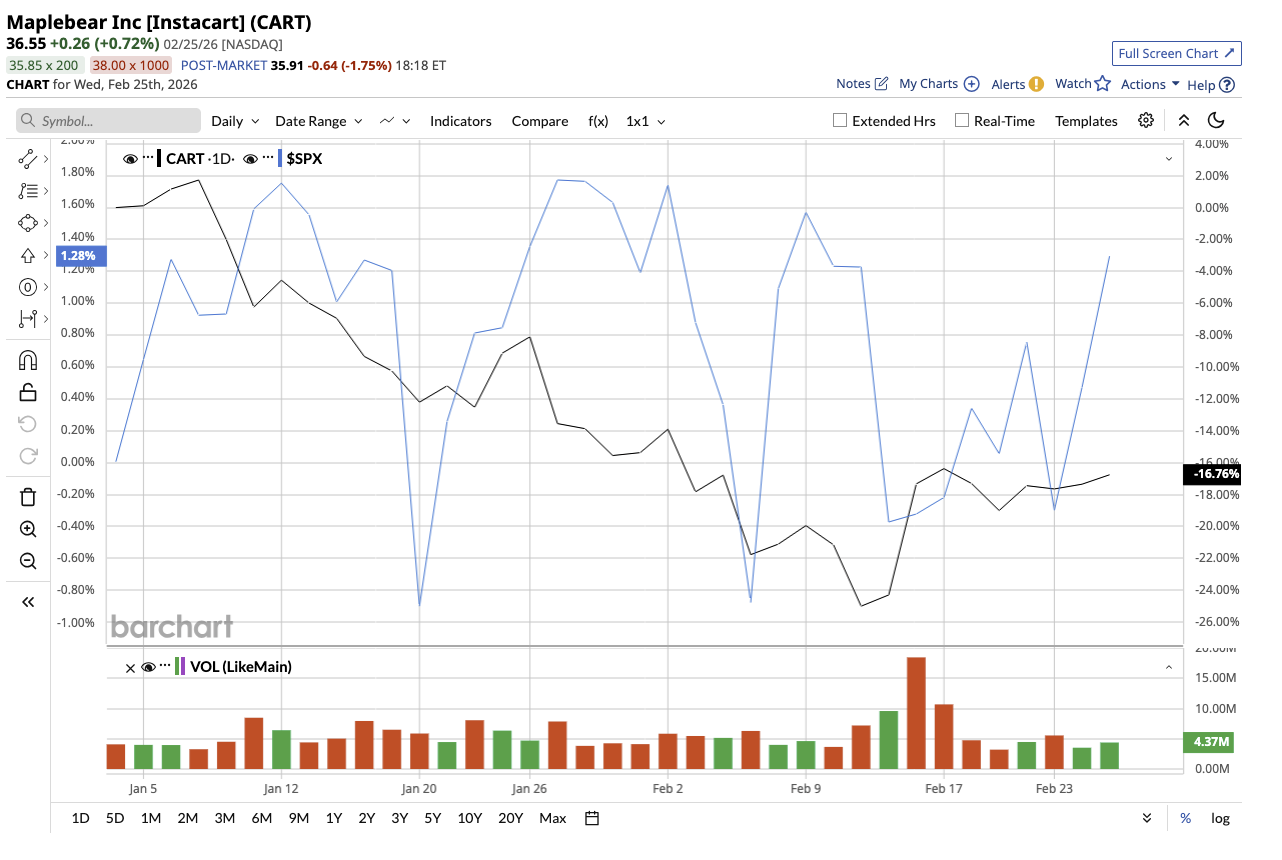

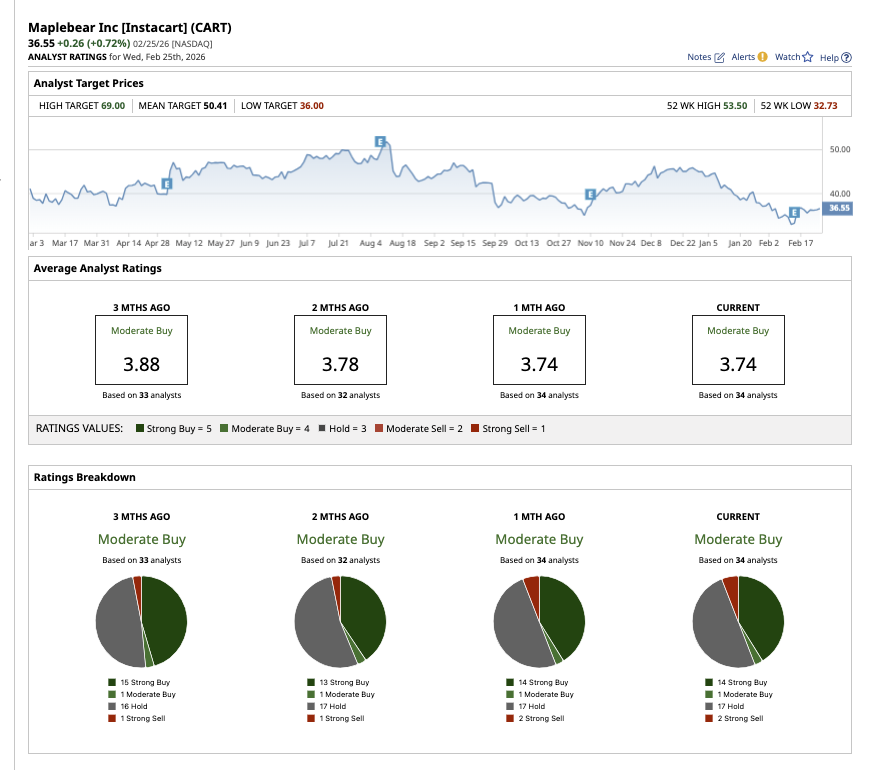

CART stock is down 16% year-to-date (YTD). Nonetheless, analysts believe the stock can go up by 38% based on the average target price of $50.41. Furthermore, the high price estimate of $69 suggests a potential upside of 89% over the next 12 months. Overall, Wall Street rates CART stock as a “Moderate Buy.” Of the 34 analysts covering the stock, 14 rate it a “Strong Buy,” one says it is a “Moderate Buy,” 17 rate it a “Hold,” and two say it is a “Strong Sell.”

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart