Valued at a market cap of $185 billion, The Walt Disney Company (DIS) is a diversified global entertainment conglomerate with leadership across filmed entertainment, television networks, streaming, theme parks, and consumer products. Founded in 1923 and headquartered in Burbank, California, Disney operates a vertically integrated ecosystem for the creation, distribution, and monetization of intellectual property.

Companies valued at $10 billion or more are generally considered “large-cap” stocks, and Walt Disney fits this criterion perfectly. Its market leadership stems from its unmatched portfolio of globally recognized intellectual property franchises (e.g., Disney classics, Marvel, Star Wars) and its ability to monetize that IP across a vertically integrated ecosystem, spanning films, streaming, television, theme parks, cruises, and consumer products. This cross-platform monetization flywheel amplifies brand engagement, drives recurring revenue, and creates durable pricing power, particularly in its high-margin parks-and-experiences segment.

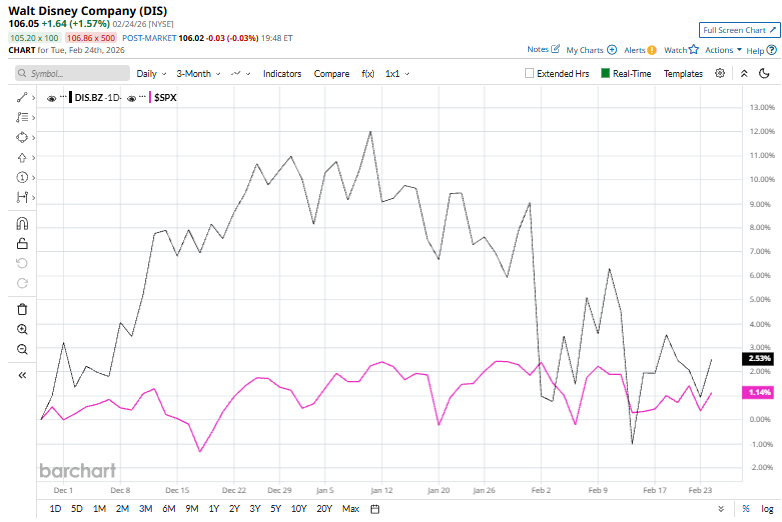

However, shares of the company have fallen 15% from its 52-week high of $124.69. Over the past three months, Walt Disney shares have soared 4%, lagging behind the S&P 500 Index’s ($SPX) 2.8% gains.

DIS stock has decreased 6.8% on a YTD basis, lagging behind $SPX’s marginal rise over the same period. Moreover, shares of Walt Disney have dropped 4.6% over the past 52 weeks, compared to SPX’s 15.2% gain.

The stock has slipped below its 50-day and 200-day moving averages since early this month.

On Feb. 2, Walt Disney released its FY2026 Q1 results, which disappointed investors, sending the stock down by over 7%. While revenue rose 5% year over year to $26 billion, adjusted EPS fell 7% to $1.63, reflecting margin pressure across key segments. Entertainment operating income dropped sharply due to elevated content and marketing costs, and Sports (ESPN) profits declined amid sports-rights inflation, subscriber erosion, and distribution disruptions. Although Parks & Experiences remained the primary profit driver with record revenue, its strength was insufficient to offset the weakness, resulting in overall operating income contraction.

Investor sentiment was further hurt by soft Q2 guidance, which pointed to continued earnings pressure and limited near-term margin recovery, reinforcing concerns about Disney’s costly streaming pivot and secular linear-TV headwinds.

In contrast, rival Netflix, Inc. (NFLX) has underperformed Walt Disney stock. Netflix shares have tanked 21.1% over the past 52 weeks and 16.8% on a YTD basis.

Despite DIS' underperformance over the past year, analysts remain highly optimistic about its prospects. Among the 30 analysts covering the stock, there is a consensus rating of “Strong Buy,” and the mean price target of $133.70 is a premium of 26.1% to current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart