American Express Company (AXP), headquartered in New York, operates as an integrated payments company. With a market cap of $220 billion, the company’s principal products and services are charge and credit payment card products and travel-related services offered to consumers and businesses around the world.

Companies worth $200 billion or more are generally described as “mega-cap stocks,” and AXP definitely fits that description, with its market cap exceeding this threshold, reflecting its substantial size, influence, and dominance in the credit services industry. AXP's strength lies in its integrated payments platform, allowing for direct relationships with customers and merchants. This unique position enables the company to gather valuable transaction data for personalized services and tailored marketing efforts. With a reputation for premium quality and customer service, AXP attracts high-spending clients and maintains a loyal customer base. Its focus on innovation and customer experience is reflected in its digital services and customer care, appealing to Millennials and Gen Z.

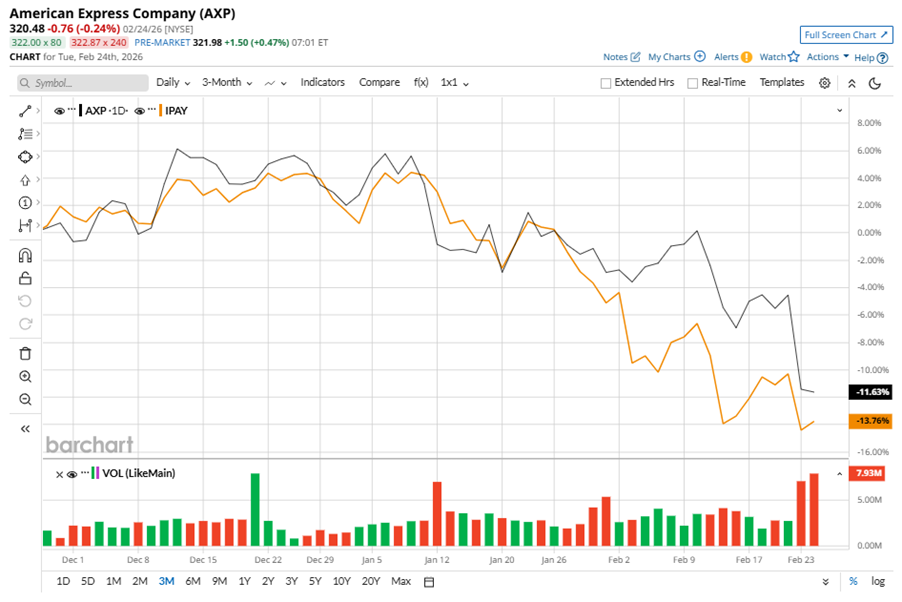

Despite its notable strength, AXP slipped 17.3% from its 52-week high of $387.49, achieved on Dec. 12, 2025. Over the past three months, AXP stock declined 10%, outperforming the Amplify Digital Payments ETF’s (IPAY) 12.5% dip during the same time frame.

Shares of AXP fell 13.4% on a YTD basis but climbed 8.4% over the past 52 weeks, outperforming IPAY’s 15.1% dip on a YTD basis and 23.4% losses over the last year.

To confirm the bearish trend, AXP is trading below its 50-day moving average since early January. The stock has been trading below its 200-day moving average recently.

AXP is crushing it due to a shift to premium products like the U.S. platinum card, driving card fee growth and customer engagement. CEO Stephen Squeri notes high demand and excellent credit quality. AXP expects continued growth from premium strategy, tech investments, and younger cardholders. Its key drivers include U.S. platinum card refresh, international growth, and digital expansion. Millennials and Gen Z are driving spending growth, with strong international results and tech upgrades boosting efficiency.

On Jan. 30, AXP shares closed down by 1.8% after reporting its Q4 results. Its EPS of $3.53 did not meet Wall Street expectations of $3.54. The company’s revenue was $19 billion, surpassing Wall Street forecasts of $18.8 billion. AXP expects full-year EPS to be $17.30 to $17.90.

In the competitive arena of credit services, Visa Inc. (V) has taken the lead over AXP, with a 12.4% downtick on a YTD basis but lagged behind the stock with a 12.2% loss over the past 52 weeks.

Wall Street analysts are reasonably bullish on AXP’s prospects. The stock has a consensus “Moderate Buy” rating from the 30 analysts covering it, and the mean price target of $378.89 suggests a potential upside of 18.2% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart