Wall Street’s outlook for Five9 (FIVN) reflects a wide spectrum of sentiment, but at the bullish end, some analysts see major upside potential ahead.

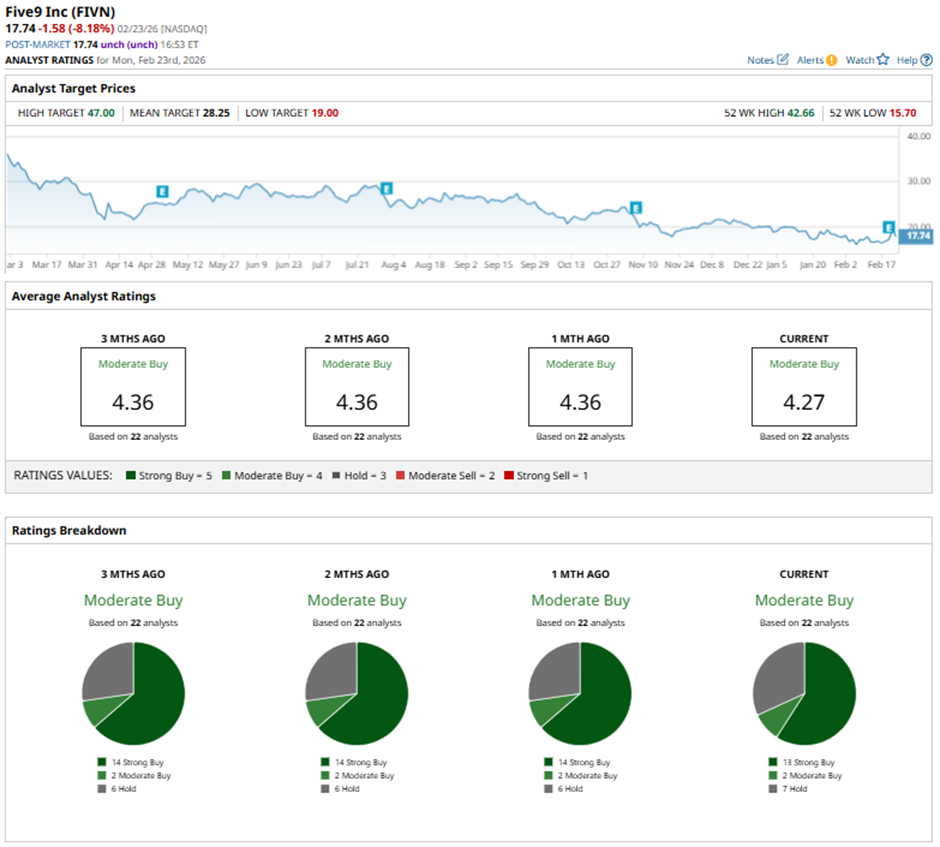

Among the latest forecasts, the Street-high price target set by Northland Capital Markets sits at about $47, markedly above the current trading range and signaling significant optimism about the cloud contact-center software provider’s growth prospects. This estimate reflects 164.9% upside from yesterday's closing price. Northland Capital has rated the stock a “Strong Buy.”

Shares of Five9 have shown momentum lately, climbing about 13.8% over the past five days. On Thursday, the company reported better-than-expected earnings and issued upbeat guidance, easing investor concerns that artificial intelligence (AI) could undermine its business model. Management said enterprise AI bookings more than doubled year-over-year, boosting backlog, while its AI portfolio reached $100 million in annual recurring revenue.

About Five9 Stock

Five9 is a provider of cloud-native contact center solutions that help businesses manage customer interactions across voice, chat, email and other digital channels. The company’s flagship Virtual Contact Center platform is designed to replace legacy on-premise systems with scalable, secure, and AI-enhanced software for customer service, sales, and support teams.

Headquartered in San Ramon, California, Five9 serves enterprises, mid-market, and small business customers worldwide with tools for omnichannel engagement, workforce optimization, and analytics. Five9’s market cap is currently about $1.4 billion.

Over the past year, Five9’s share price has endured significant volatility, reaching a 52-week high of $42.66 in February 2025 before tumbling 58.4% to close the last session at $17.74, reflecting substantial downward pressure amid sector weakness and shifting investor sentiment. The stock is down by 57.9% over the past year.

From a year-to-date standpoint, Five9 has also struggled, with returns still down about 11.5% as the shares attempt to rebound from deeper lows earlier in the year. The recent, modest uptick in price following positive earnings and guidance helped ease some selling pressure, but overall performance remains well below last year’s levels. Moreover, the momentum did not sustain in the subsequent session as the stock slumped 8.2% intraday on Feb. 23.

The stock is currently trading at 14.2x forward earnings, which is below the sector median.

Solid Quarterly Performance

Five9’s fourth-quarter and full-year 2025 financial results, released on Feb. 19, painted a picture of growth and improving profitability after years of transition. In Q4, the company reported record revenue of $300.3 million, up 8% year-over-year, with subscription revenue the bulk of its recurring business, growing 12% against the prior year. Enterprise AI revenue, a key strategic focus, expanded by about 50% year-over-year, with a healthy increase in backlog as bookings more than doubled compared with the prior period.

On profitability, Five9 delivered adjusted earnings per share of $0.80, which was above estimates, and up compared to $0.79 in the year-ago quarter. Notably, adjusted EBITDA margin widened year-over-year to 26%.

Full-year 2025 results showed a 10% increase in revenue to about $1.2 billion, while the company turned full-year net income positive at about $39.4 million after years of losses, marking a structural shift in profitability. Its non-GAAP earnings came in at $2.96, compared to $2.47 in the prior-year quarter.

Management’s guidance for fiscal 2026 calls for revenue in the range of $1.25 billion to $1.26 billion with non-GAAP EPS in the range of $3.15 to $3.21.

Analysts remain optimistic, forecasting EPS of roughly $1.22 for fiscal 2026, a 23.2% year-over-year jump, followed by a further 26.2% rise to $1.54 in 2027.

What Do Analysts Expect for Five9 Stock?

While FIVN has a robust Street-high price target, a number of analysts have trimmed their price targets recently. Nevertheless, the consensus rating on the stock remains largely favorable.

Five9 saw RBC Capital lower its price target to $25 from $35 while maintaining an “Outperform” rating, following solid fourth-quarter results. Despite the target cut and the stock’s sharp declines over the past year, RBC remains constructive, with analysts noting improving AI traction.

Also, Five9 saw its price target cut by Cantor Fitzgerald to $26 from $32, due to compressing multiples across the software sector, though the firm maintained an “Overweight” rating after the company delivered stronger-than-expected fourth-quarter 2025 results.

Overall, FIVN has a consensus “Moderate Buy” rating. Of the 22 analysts covering the stock, 13 advise a “Strong Buy,” two suggest a “Moderate Buy,” and the remaining seven analysts are on the sidelines, giving the stock a “Hold” rating.

FIVN’s average analyst price target of $28.25 suggests upside potential of 59.2%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart