Software stocks have not had it easy this year. The application software space, once the market’s steady compounder, has taken a sharp hit. Many of these names are down 30% to 55% year-to-date (YTD) – a steeper slide than the broader software pack, with the iShares Expanded Tech-Software Sector ETF (IGV) off around 27.2%. Clearly, investors are reassessing what growth really looks like in an artificial intelligence (AI)-first world.

That shift in mood prompted Jefferies analysts led by Brent Thill to take a step back and reassess the space. The team applied a new AI Risk Matrix, examining factors such as customer mix, competitive positioning, proprietary data advantages, and pricing models. Their conclusion was cautious: the market faces “further risk of AI disruption,” and selectivity is now critical. Several stocks were moved to “Hold” as risks and sentiment pressures linger.

Still, Jefferies believes software as a category remains fundamentally resilient. Business processes are deeply embedded in these platforms. And in this reset, some names stand out, including Intuit (INTU), the business and tax software maker.

Jefferies named Intuit its “top large-cap pick” in application software. The brokerage firm highlighted how Intuit uses around 80 AI model variations built on over 40 years of data from nearly 100 million customers. That deep data pool and massive user base create a strong competitive moat, giving analysts confidence in its ability to adapt and grow through the AI shift.

Let’s take a closer look at Intuit.

About Intuit Stock

California-based Intuit, founded in 1983, is a global financial technology platform serving nearly 100 million users. The company builds tools that help consumers file taxes, track spending, build credit, and grow wealth, while empowering small businesses to manage accounting, payroll, payments, and marketing.

Its ecosystem spans QuickBooks for business management, TurboTax for tax preparation, Credit Karma for personal finance, and professional tax solutions for accountants. Increasingly, Intuit is layering AI and expert support across these products, aiming to simplify complex financial tasks and create a connected, end-to-end money management experience. Its market cap stands at around $100.05 billion.

Intuit started 2025 with strong momentum. Solid tax-season numbers and growing confidence in its AI push helped the stock climb steadily. But as the broader tech sector cooled, the rally lost steam.

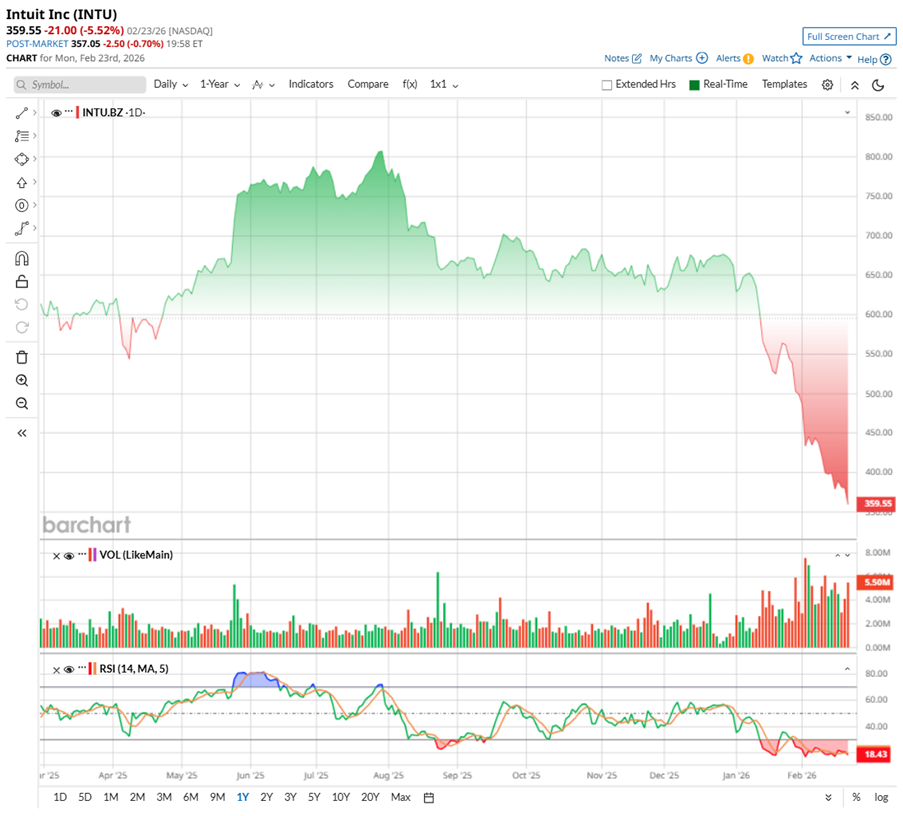

Fast forward to early 2026, and the mood has clearly changed. The stock is down about 44.5% YTD and recently touched a low of $349, a level not seen in nearly three years. From its July high of $813.70, that’s a drop of nearly 56%. The selloff reflects a wider reset in software valuations, as investors worry about AI disruption and compress multiples across the sector.

From a technical standpoint, volume has picked up noticeably during the recent selloff, with several high red bars signaling heavy distribution and strong selling pressure. At the same time, the 14-day RSI has dropped deep into oversold territory, near the low-20s, suggesting momentum is stretched and the stock may be nearing short-term exhaustion. This combination hints at intense pressure now, but also raises the possibility of a technical bounce if sentiment begins to stabilize.

After the recent pullback, Intuit is trading at more reasonable levels. The stock is priced at around 15.5 times forward adjusted earnings, with a forward PEG ratio sitting at 1.1x – below both sector averages and its own historical norms. For a company delivering steady double-digit earnings growth, backed by diversified platforms and growing AI integration, the current valuation appears attractive and arguably undervalued.

Beyond its appealing valuation, Intuit rewards shareholders with steady dividends. The company has paid and increased its dividend for 14 consecutive years. In January, it distributed $1.20 per share for the quarter, which translates to an annualized forward payout of $4.80 per share. With a forward yield of about 1.34% and a payout ratio near 20%, the dividend looks sustainable, leaving ample room for future increases.

Intuit Tops Q1 2026 Numbers

When Intuit reported its fiscal first-quarter 2026 results on Nov. 20, the numbers beat Wall Street’s projections, signaling business is still growing rapidly. For the quarter ended Oct. 31, 2025, revenue came in at about $3.9 billion, up roughly 18% year-over-year (YOY). Non-GAAP EPS rose to around $3.34, well above last year’s $2.50. The engine behind that growth was subscription revenue, supported by healthy demand across its ecosystem.

TurboTax delivered another solid performance, with TurboTax Live seeing particularly strong engagement as more users opted for expert-assisted services. The Global Business Solutions segment, home to QuickBooks, continued to post steady gains as small and mid-sized businesses leaned further into digital tools. Credit Karma also contributed with double-digit growth, adding momentum to the consumer platform. With scale improving and costs well managed, adjusted earnings climbed more than 20%, reflecting strong operating leverage.

At the center of it all is Intuit’s AI-driven expert platform strategy. The company is building what it calls a “system of intelligence,” combining decades of data, AI, and human expertise. New “done-for-you” innovations are helping businesses move smoothly from lead generation to getting paid, while consumers can manage everything from credit building to long-term wealth creation within one connected platform.

Financially, the balance sheet remains solid. Intuit ended the quarter with about $3.7 billion in cash and investments against $6.1 billion in debt. Over the past year, free cash flow amounted to $6 billion, giving the company flexibility to reinvest in innovation while returning capital to shareholders. During the quarter, it repurchased $851 million worth of stock, with $4.4 billion still available under its authorization.

Looking at the guidance, management expects fiscal 2026 revenue between $20.997 billion and $21.186 billion, implying growth of roughly 12% to 13%. Non-GAAP EPS is expected in the range of $22.98 to $23.18, marking projected growth of about 14% to 15%.

The company is gearing up for its Q2 earnings report on Thursday, Feb. 26, after the market closes. Management expects the momentum to continue. For Q2, revenue is projected to grow in the mid-teens, alongside higher earnings.

Meanwhile, analysts tracking Intuit anticipate Q2 revenue to grow to $4.5 billion, with the bottom line rising 7.7% YOY to $2.23 per share. Looking further ahead to fiscal 2026, the company’s EPS is anticipated to grow 12.1% annually to $17.23 before jumping by another 14.2% YoY to $19.68 in the next fiscal year.

What Do Analysts Expect for Intuit Stock?

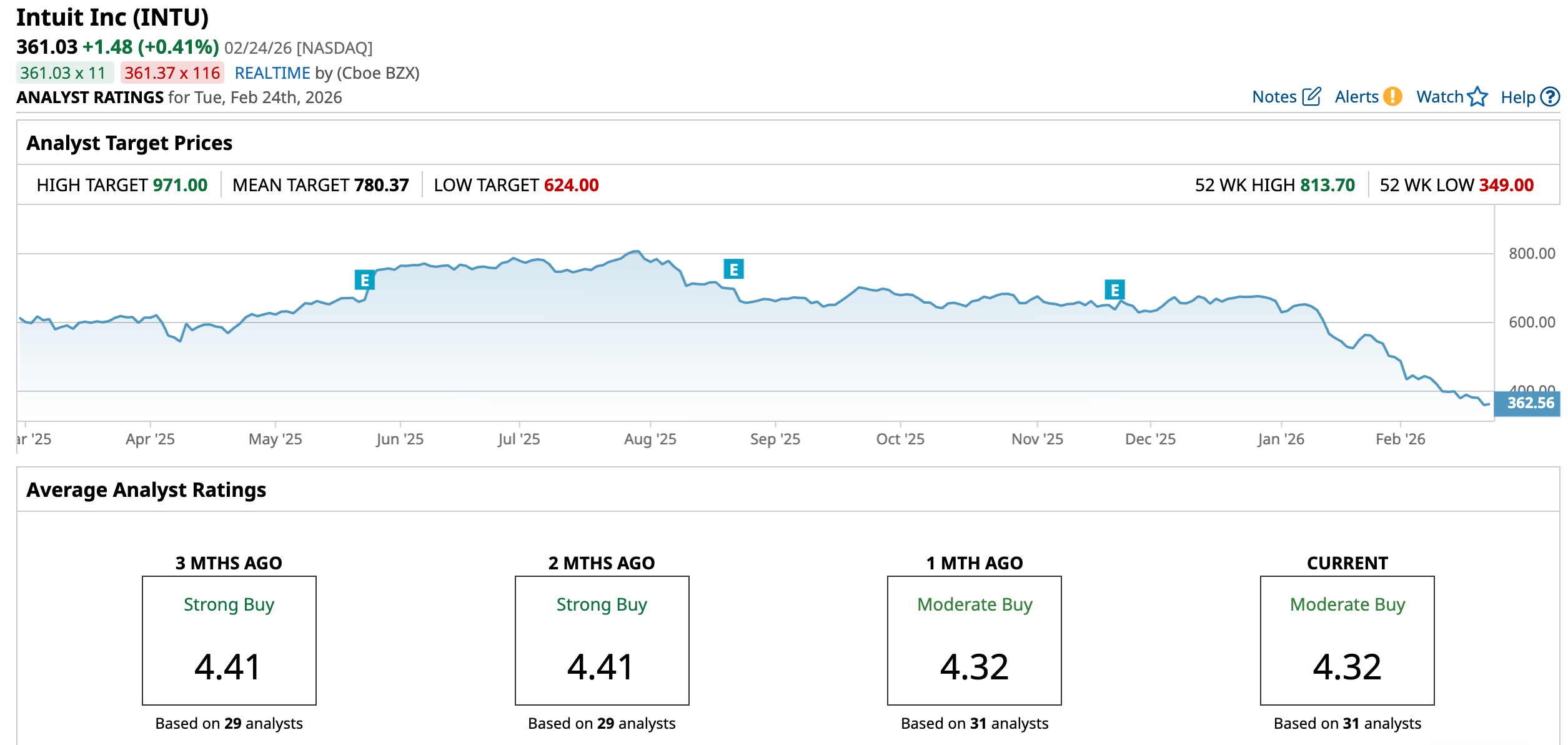

Jefferies recently trimmed its price target on Intuit to $650 from $850, but it still has a “Buy” rating on INTU. The brokerage firm expects solid fiscal Q2 results, even though it is a seasonally quieter period with limited tax e-filing days. Also, Jefferies sees potential upside from Credit Karma, supported by improving momentum among credit card issuers.

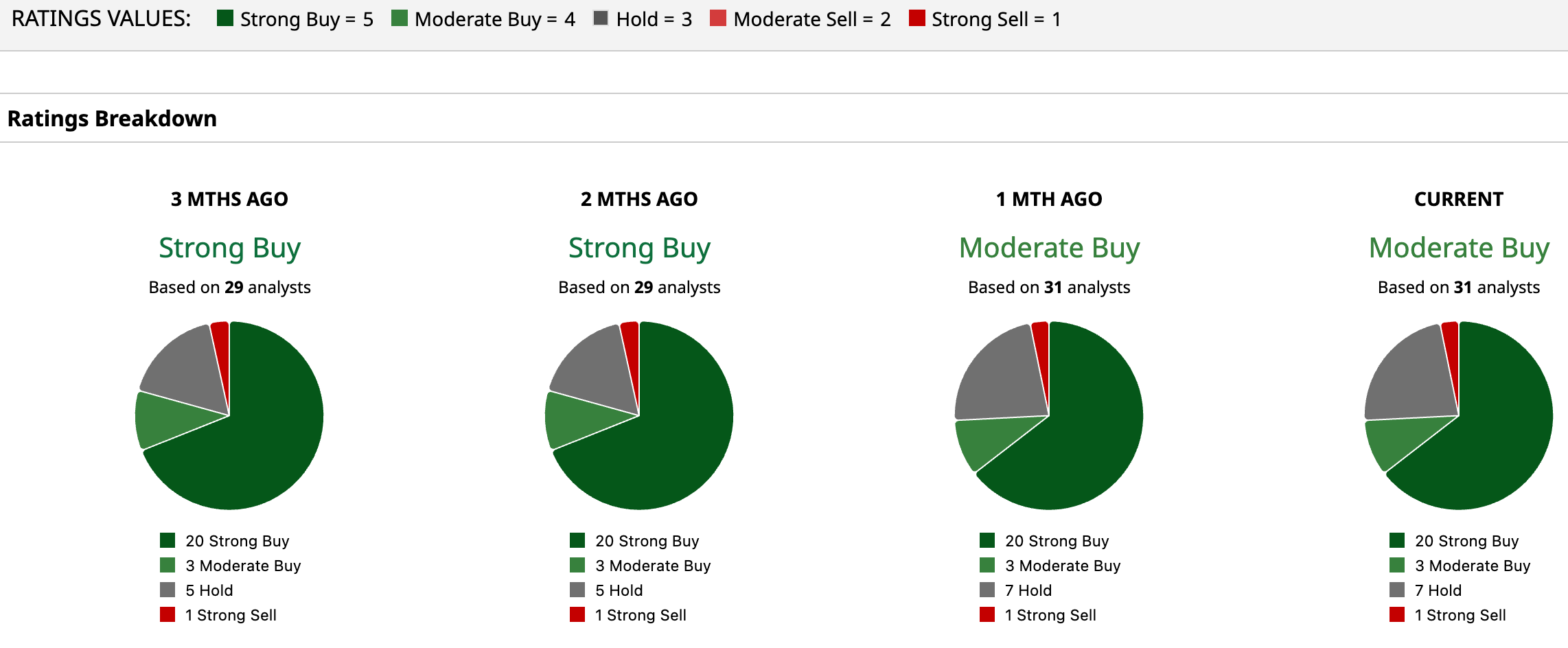

Overall, analysts have revised INTU to a “Moderate Buy,” down from a “Strong Buy” rating two months ago, reflecting a more cautious tone in investor confidence. Out of the 31 analysts in coverage, 20 recommend a “Strong Buy,” three suggest a “Moderate Buy,” seven analysts are playing it safe with a “Hold” rating, and the remaining one is skeptical, having a “Strong Sell” rating.

Meanwhile, INTU’s mean price target of $780.37 suggests rebound potential of 116% from the current price levels. On an optimistic note, the Street-high of $971 the software application stock could rally as much as 169%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart