High-profile managerial cuts draw notice when it is a high-profile manager, yet headline-sized trades do not necessarily correlate with broken companies. Even long-term names can feel vulnerable on the tape when portfolio rebalancing and changes in thematic conviction make even the names look vulnerable in a choppy growth market and tech-proximate market.

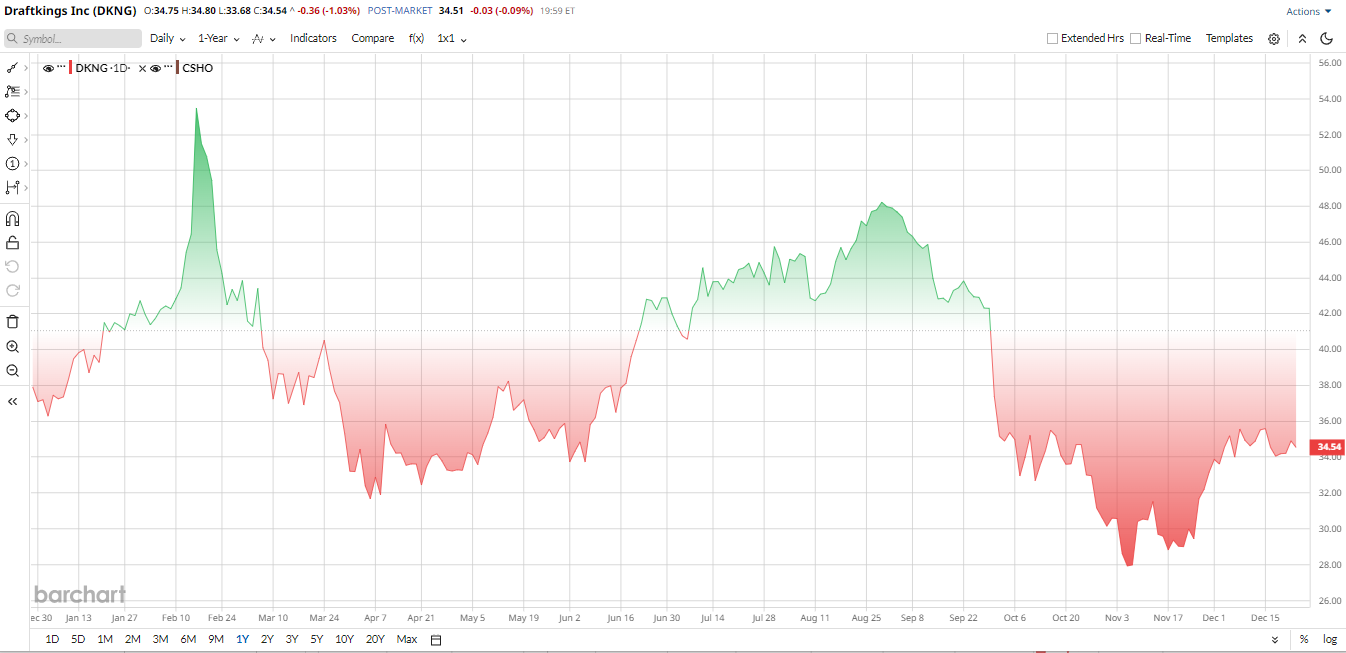

The same dynamic is being enacted with DraftKings (DKNG) following the sale by Cathie Wood’s ARK Invest last week. After holding DraftKings for a long time, ARK Invest has just sold over 300,000 shares, and that has investors wondering whether there is more to the decision or if this was just a normal rebalancing of their portfolios. The sale is at an uncertain time in the DKNG stock in 2025, but the company is still recording good revenue growth yet reports heavy losses.

As DraftKings continues to gain market presence and the management says that it is optimistic about its prospects, the main question that investors can ask is simple: Is the selling of Cathie Wood a red flag, or can it be an opportunity?

About DraftKings Stock

Based in Boston, DraftKings is a digital sports entertainment and gaming company. It offers online fantasy sports, sports betting, and iGaming across multiple states and regulated markets. DraftKings leverages technology to provide mobile wagering and also related digital media experiences to sports fans.

Valued at around $17 billion market cap, after strong gains in prior years, it has had a rougher stretch this year. Year-to-date (YTD), shares are down roughly 7%, reacting not just to broader tech swings but also to the unpredictability of sports outcomes that sometimes favor bettors over the house. Still, the long-term story remains intact. DraftKings continues to expand its footprint in U.S. sports betting, opening new markets like Missouri, which should drive growth for years to come.

However, on a valuation basis, it appears to be a challenge, as DKNG's multiples are extremely expensive relative to its peers. For instance, its price-to-book ratio is 23.18, significantly higher than the sector median of 2.14, suggesting that the stock is priced at a premium.

Ark Trade News and Market Reaction

Last week, ARK Invest disclosed it sold about 310,548 DKNG shares worth $10.7 million. This news briefly rattled the market, pushing DKNG slightly lower on the day. However, investors noted ARK’s history of frequent rebalancing in its ETFs, and DraftKings was only one of many trim targets.

Traders largely took the move in stride, focusing on fundamentals. In context, DraftKings had just reported solid results and raised guidance, so the sale was seen more as an ARK portfolio adjustment. In the minutes following the announcement, the stock impact was modest and short-lived.

Overall sentiment remained positive. Analysts pointed out DraftKings’ core business continues expanding, indicating Ark’s selloff is a tactical shift rather than a bearish signal for DKNG.

Revenue Growth Keeps Rolling While Losses Remain Intact

DKNG shares fell about 3% after the company reported mixed third-quarter results and lowered its full-year outlook.

While revenue rose 4% year-over-year (YoY) to $1.14 billion, it missed analyst expectations, reflecting a sharp contrast between strong iGaming growth, up nearly 25%, and a 9% decline in Sportsbook revenue as customer-friendly outcomes weighed on betting hold.

GAAP net losses remained significant at $257 million, though adjusted EPS of -$0.26 per share came in line with analysts' expectations, and adjusted EBITDA stayed negative at $127 million.

On the positive side, DraftKings strengthened its liquidity, ending the quarter with $1.23 billion in cash and generating positive free cash flow while expanding its $2 billion share repurchase plan.

CEO Jason Robins remains optimistic about long-term growth, pointing to new products and marketing initiatives.

However, DraftKings lowered its FY2025 revenue guidance from $5.9 to $6.1 billion, below the $6.2 billion expected, signaling near-term headwinds, particularly in Sportsbook performance.

Overall, while the long-term story of market expansion remains intact, the quarter highlights ongoing volatility that investors will need to navigate carefully.

Expands Product Footprint

DraftKings has been busy expanding its offerings. On Dec. 19, it launched DraftKings Predictions, a standalone prediction-market app. This moves DraftKings into new lines of wagering under CFTC oversight, potentially broadening its market.

Recently, DraftKings also rolled out a Spanish-language version of its sportsbook and casino to cater to that demographic. Partnerships have added momentum: the company announced a multi-year deal making it the official sportsbook of ESPN, and New York regulators reported record betting revenue, with DraftKings’ share of $89.1 million for the month. These initiatives, plus upcoming launches in states like Missouri, are largely considered positives by investors.

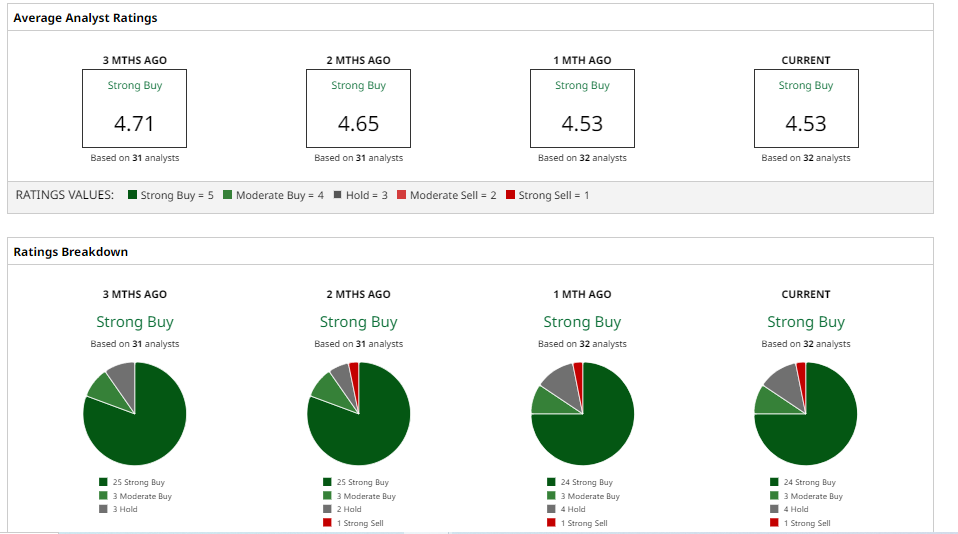

Analysts Opinions on DKNG Stock

Mostly analysts are showing confidence in DraftKings’ growth, while others are staying a little cautious.

Recently, Morgan Stanley kept an “Overweight” rating on DKNG stock with a $50 price target, pointing to the company’s new prediction markets platform as a potential long-term growth driver. Analysts there said the product could meaningfully expand DraftKings’ addressable market over time, though they also cautioned that early investment and marketing costs may limit near-term upside and keep the shares trading in a range.

Goldman Sachs also stayed constructive, maintaining a “Buy” rating while trimming its 12-month price target to $54 from $59 following the third-quarter report. The bank highlighted what it sees as underlying demand strength, including double-digit growth in NFL and NBA betting handle, while factoring in one-time headwinds from customer-friendly sports outcomes. Goldman said valuation still implies significant upside from current levels.

Susquehanna reiterated its “Buy” rating with a $59 target, and several other firms made more modest adjustments. Canaccord Genuity lowered its target to $54, while MoffettNathanson reduced its view to $48, both while keeping broadly positive stances on the longer-term story.

Overall, analyst sentiment remains supportive. DKNG stock carries a consensus “Strong Buy” rating, with most analysts setting a mean price target of $44.45, which suggests about 60% upside potential from the current price.

The Bottom Line

DraftKings’ long-term growth narrative remains intact, anchored by its expanding market presence and product innovation. However, investors should note that DraftKings is a high-risk stock due to sharply negative EPS revisions and extreme valuation multiples versus its consumer discretionary peers.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Super Micro Computer Stock Tumbles, But Investors are Piling into Its Call Options - Time to Buy SMCI?

- Chipotle Just Launched a New Protein-Packed Menu. Should You Buy CMG Stock for 2026?

- Cathie Wood Is Selling DraftKings Stock. Should You?

- Dan Ives Is Betting That Apple and Google Will Partner in 2026. Should You Buy AAPL Stock First?